History Is Kindest To Those Who Sanitize It

History Is Kindest To Those Who Sanitize It

“Therefore, having judged that to be happy means to be free, and to be free means to be brave, do not shy away from the risks of war.” (Pericles)

Summary:

· History is being kind to the sanitizers of the Ukraine War thesis.

· Sanitization efforts are turning towards China, even before Russia has been sanitized.

· “Cold Amazon” Vice Chair Brainard reminds that Fed monetary policymaking will always put patriotism before the dual mandate.

· The Villeroy and The Bosch model of the Eurozone Project applies consolidation to achieve energy security.

· Amazon signals that supply has caught up with demand, not in a good way, but, in a Schumpeterian way.

· Raphael Bostic confirms that demand has caught up with constrained supply, but not in a good way.

· Bostic also confirms that the FOMC is primarily fighting inflation, with the risky mismatched tool of financial stability policy, since supply-side inflation is beyond the Fed’s monetary policymaking reach.

· The balance sheet discussion in the latest FOMC minutes was the Soft-Landing signal.

· The UK economy is finding out which layer of the global economy cake will be served at Jubilee street parties.

As IMF Managing Director Kristalina Georgieva warned of the risks of global economic fragmentation, as a consequence of the Ukraine war, the global economy continued to fragment. As the global economy fragmented, the Davos World Economic Forum coalesced, in person, to try to hold it together.

· China has switched its global economic strategy from working through G20 to working through the BRICs.

(Source: the Author)

The last report observed China’s concentration of its global economic center of gravity around the locus of the BRICs. The Asia-Pacific Economic Cooperation (APEC) group has become the latest casualty, of walkouts, in the war of economic attrition between the competing economic interests in the region. The unavoidable conclusion is that some, of the multipoles, in the emerging New Multipolar World Order (NMWO), repel each other.

In all of this global repulsion, or perhaps in view of it, a compelling narrative is being promoted by those currently holding the initiative.

We’ve been expecting you, Mr. Putin ….

History, allegedly, is kind to those who write it. Applying this maxim, a recent Russian attempt to rewrite history, therefore, appears to be failing because its war in Ukraine is failing.

History also appears to be kindest to those who sanitize it.

If only the Fed and the Federal Government could find someone else to blame for the global supply chain woes and inflation. If blaming this someone also required disinflationary, deficit financed, supply-side investment then both could stop blaming each other, and get on with the financing.

Which brings both to the war in Ukraine.

As President Putin’s offensive and health appear to dissipate, writers who have seized the initiative are being unkind. In a recent draft version, of the historiography of the Ukraine conflict, it is written that Putin’s fate was sealed, back in 2013, by oil and gas analyst Daniel Yergin, when the latter asked the Russian President for his take on the threat from American Shale. At this point, as the story goes, it is alleged that energy (officially) became weaponized; and that the US and Russia were, then, headed on a collision course. They both recently collided in Ukraine.

As a result, of the collision, it is reported that President Putin is commanding at the rank of a colonel/brigadier-general. It is also reported that war crimes are being committed in the ranks from colonel down.

(Source: internationalcriminalcourtofjustice)

Evidently, the chain of command, from colonel/brigadier-general upwards may not necessarily be implicated in said war crimes; since these officers are not the ones technically giving the orders anymore. The officers from major general, up to field marshal, thus, don’t even have to use the standard we were only following orders plea made popular at a previous infamous war crimes trial. The same may not be said for the unique rank, of one, at President-Colonel/Brigadier-General in Chief level in the chain of command.

There is, however, a way for the uniquely unfortunate President-Colonel/Brigadier-General in Chief to avoid the Hague, if he is deemed to be too ill to stand trial. Incarceration, and ostracism, in a sanatorium, would be the sentence; thereby leaving the exonerated chain of command upwards to negotiate peace with honor. Strangely enough, this sentencing is already taking place in the criminal court of the public domain.

If any of this collision dialectic fiction is true, then what is happening, in Ukraine, today, is no surprise. It is, then, also highly likely that there is a plan that has been in place, for some time, since Yergin’s drawing of first blood, to deal with the collision. Providence, or something masquerading as such, it may seem, has chosen to have the collision happen now.

This author would hazard a guess that, if it exists, this collision plan was first conceived when President Obama was gracefully accepting defeat, whilst NSA Susan Rice was simultaneously explaining that Russian influence had been, mainly, responsible for the said defeat. Shortly after Shale was weaponized, in 2013, Advisor Rice laid down her marker in 2014. The rest, as they say, is history. President Zelensky recently reminded his allies of the timeline, when he rebuked them for their failure to act, in 2014, when Rice initially laid down her warning tracer.

Strategists also know the maxim “that it is pardonable to be defeated, but never to be surprised”. President Biden is looking neither surprised, nor defeated. In fact, POTUS predicted the Ukraine invasion days before it happened. Unfortunately, he did not make a prediction when he was Vice President and NSA Rice issued the original threat alert. The maxim that one should never interrupt an enemy that is making a mistake also now comes to mind.

Waving a carrot, or perhaps an olive branch, POTUS has appeared anxious that the President-Colonel/Brigadier-General-Chief should be given a way out before he hits the red button that begins the end of civilization. Almost as swiftly, as this anxiety was aired, the sanitorium door was metaphorically unlocked. Waving a stick, POTUS then indirectly charged Putin, of being a war criminal, in a genocide speech which accused the Russian president of authoring the policy of extermination of Ukrainian culture. This ethnic cleansing stick is ubiquitous since it can easily be transformed to beat President Xi Jinping for his policy toward the Uighurs.

The rats are also, allegedly, leaving the sinking Battleship Potemkin, suggesting that it’s game over, in any case. The mutiny has been led by the Pied Piper of the recently resigned Russian Ambassador in Geneva. The sentiments of the Resignator are admirable, but his timing is questionable. Why is he only leaving now that the ship is sinking? Where was his moral outrage, months ago, when the invasion began? A rat is still a rat, it would seem, even if, at least, it is now our rat.

It may not be over until the fat matron at the sanatorium sings, but this has not stopped plans for a New World Order from being made, in the meantime, whilst the appended clinical admission formalities remain pending.

· As President Putin’s offensive, and his health, dissipate the G7 “Friend-Shoring-Driver” casus belli is pivoting from Russia to China’s “COVID-Zero” policy.

(Source: the Author)

Prematurely, or presciently, depending on one’s perspective, attention is already being shifted, away from Ukraine, towards the threat from China. Henry Kissinger is most anxious that this focal pivot is both fast and concluded, with compromise, rather than with further hostility. According to the Kissinger worldview, Russian economic integrity and autonomy should be preserved so that it does not become a Chinese satellite. Furthermore, China should be understood rather than antagonized. The great strategist seems to have forgotten that when what he is suggesting now was previously pursued, as Western foreign policy, Russia and China took liberties and tried to undermine the cornerstones of democracies. When most favored nations turn on those who have favored them, the risk of being fooled twice is not edifying.

Readers should note that the sanatorium exit door in China has also been unlocked this month.

A genocide speech in relation to the Uighurs should now be expected. The ground has already been prepared, with leaked information about the detention and abuse of Uighurs in concentration camps.

· China’s “COVID-Zero” strategy may now be to mitigate bank runs rather than COVID-19 per se.

(Source: the Author)

The schism between the Chinese President and Premier is widely known and widely reported. Clearly, this schism provides political context for the true understanding of how and why the “COVID-Zero” strategy is playing out the way it is. If it is true that the Chinese leader is incapacitated, in some way, then the reasoning behind the “COVID-Zero” strategy, at the expense of the economy, also, needs closer scrutiny. Resistance to the “COVID-Zero” policy is growing. Enforcement is already crumbling in the face of militant youth. It is not clear if the resistance is to the harsh conditions or it is just because those under lockdown do not believe the story of their current incarceration.

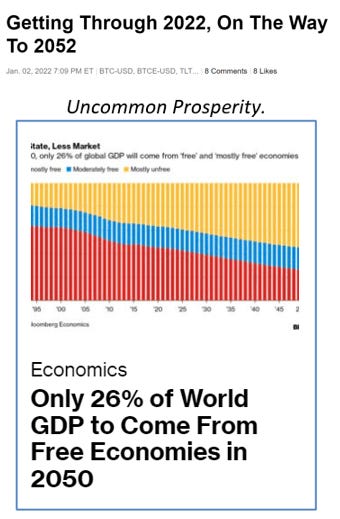

Some economists estimate that, by 2050, only 26% of global GDP will come from democracies. Conveniently absent, from this alarming headline, is a statistic that explains how the accumulated wealth, between now and 2050, will be distributed. “The 1%” appears to have found a way to hide, within “The 26%”; and militate the latter into confronting “The 74%” on their behalf.

(Source: the Author)

Before doing any thesis testing, it may also help the reader to revisit the global macro outlook for 2022 from this author.

It may also help the reader to peruse the recent commencement remarks of Fed Vice Chair Lael Brainard to the graduating class of the School for Spies and Wonks (SSAW) aka SAIS.

New Multipolar World Order (NMWO) (II): “I love workin’ for Uncle Sam ….”

Despite coming across as a bit of a broadly inclusive Woke Luvvy, Fed Vice Chair Lael Brainard is a Cold Warrior. In fact, based on her commencement remarks, she is more of a Cold Amazon. In a beguiling, yet inspiring, speech Brainard made the case for a bipartisan, broadly diverse, coalition of willing graduates to get out there and do it for the Gipper. The Gipper on this occasion, being President Biden. This appears to be what she did as a graduate and what she continues to do as a Fed Vice-Chair.

Brainard is an American first, and second the Fed Vice Chair, after recently being sworn in. In this context, her interpretation of the Fed’s dual mandate is, therefore, subjective and, hence, subject to her patriotism. In these times of uncertainty, where America is threatened, it is, therefore, logical to expect that her monetary policy action will fall into line with the patriotic cadence first, and foremost.

· The Macklem Doctrine of America’s global imperative may make bigger fools out of the FOMC than the incoming inflation data.

(Source: the Author)

In short, expect big a big fiscal deficit and a big Fed balance sheet. Also expect an inflation narrative, from the Fed, which complies with the patriotic narrative. The Soft-Landing would be the patriotic narrative of choice. Then, trade and invest accordingly.

· The ultimate New World Order, enabled by Macklem Doctrine, will have its own specific financial bubble in addition to “intransient” structural inflation.

(Source: the Author)

Do not believe the patriotic inflation narrative, however. Even if inflation stops compounding at the same rate, that it did in 2021, the inflation that has been baked in is permanent, and, will never be expunged by outright price depression.

Patriotism in the Eurozone is being expanded beyond national borders within the bloc.

New Multipolar World Order (NMWO) (I): Energised by Villeroy and the Bosch ….

· Villeroy’s New Multipolar World Order (NMWO) seeks to share Liberty, Equality, Fraternity, and the American Exorbitant Privilege to finance fiscal irresponsibility.

(Source: the Author)

The last report discussed the bicameral Franco-German plan, for the unified Eurozone tripole, within the New Multipolar World Order (NMWO) under current construction. The author envisaged this Eurozone tripole as fiscally unsustainable yet sustained by the sharing of the exorbitant privilege, of global reserve currency status, pari passu, with the US Dollar. Further evidence to support this thesis is coming in rapidly.

The EU has disguised its fiscal style drift, deeper into the red, via the extension of the suspended fiscal deficit limits. The EU’s justifying tautology alleges that extending the period of fiscal limit suspension will enable a gradual transition away from fiscal stimulus towards fiscal neutral positions. With a slowing Eurozone economy, this is nonsense. Deficits will widen for two reasons. First, as economies slow, the tax receipts will slow. Second, a counter-cyclical fiscal stimulus, in each nation, will be rolled out to address the economic slowdown.

Eurozone common energy policy, and thereby mitigation of Germany’s energy-poor status, will be attained through consolidation. First up, in the consolidation process is the swallowing of the Spanish energy giant Gamesa into Siemens Energy. Germany, thereby, seeks to avoid having to nationalize key sectors, of its energy supply chain, by promoting the survival of its acquisitive national champions. Brazenly, flaunting an anti-competitive credo, which belies the strategy, Siemens is swallowing the last 33% of Gamesa which it does not already own. Presumably, the European Commission will tightly regulate the output prices of Siemens Energy, across the Eurozone, to prevent inflation and public resistance from undermining the consolidated manifest destiny envisaged.

· Christine Lagarde has anticipated the bicameral Villeroy and the Bosch Eurozone integration strategy with a tweak to the monetary policy framework at the ECB.

(Source: the Author)

The last report also discussed the prescience, of ECB President Christine Lagarde, in tweaking the central bank’s monetary policymaking process to comply with the greater devolution of fiscal powers to nations, whilst also, accommodating the Hawkish bias of her Northern European colleagues.

Lagarde has recently blogged about what she believes the new monetary policymaking parameters are and the context in which they exist. They exist in the context in which inflation is a consumption tax that benefits global trade partners at the expense of the Eurozone economy. Lagarde intends to keep monetary policy normalization settings gradual, and flexible, in order to support the “Friend-Shoring” process through which the consumption tax of inflation remains, within the Eurozone, to be recycled in the furtherance of the European Project. Bank of France Governor Francois Villeroy de Galhau agrees with her, thereby, challenging the assumption that the ECB will tighten by 50-basis points at its next Governing Council meeting. Lagarde believes that the Eurozone “Friend-Shoring” process will be a supply-side investment strategy that ultimately delivers lower inflation in the long term.

Some of Lagarde’s colleagues have grumbled, but they have all been told to get into line by their national elected leaders from whom they devolve their power and their franchise. The EU has devolved more fiscal power to national governments in consideration for these governments agreeing to economically, and politically, move closer together. Subsidiarity is, thus, in name only, since all are pulling together simultaneously. Since the national central banks devolve their legitimacy from their national leaders, who are closing ranks, there is little that they can do to obstruct the process with tighter monetary policy conditions that create fragmentation risk.

The US version of the New Multipolar World Order (NMWO) is, currently, being held up by rampant inflation. Conventional wisdom now attributes the main cause of inflation to extended and constrained supply chains. The supply chain blockage is, however, just about to be overshadowed by a more powerful force of economic contraction.

US supply catches up with demand, but not in a good way ….

Fool me thrice, still call me a “Neel”, Jan.

(Source: the Author)

Much has been made of the story of how US logistics supply chain capacity has failed. Minneapolis Fed president Neel “Ex Culpa” Kashkari has connected the tight supply chain dot, to the alleged healthy consumer balance sheet dot, in a dot plot of robust aggregate demand. This author has never connected these dots in that order. Neither, would it seem, has Jeff Bezos.

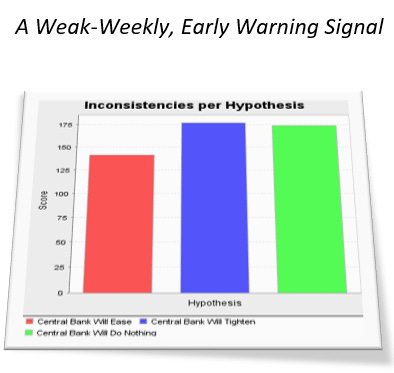

· A Key Signals proprietary indicator signals that the FOMC is, once again, totally off with its timing, this time, on monetary policy tightening.

(Source and caption by Keysignals)

Amazon has recently announced that it has overcapacity, in warehousing, relative to consumer demand, which it intends to cannibalize through attrition and sub-leasing. The author would note that this, form of Schumpeterian Creative Destruction, is a significant context for his own proprietary indicator that began calling for the Fed to ease in the first week of May. The business cycle is turning swiftly into a down wave, lagging the already contracting credit cycle by a couple of quarters.

· The US will have a barnstorming attempt at a soft economic landing.

(Source: the Author)

The release of the latest FOMC meeting minutes was an opportunity to see how the committee was factoring in the US economy’s sudden loss of altitude into its attempted soft-landing.

The Softly-Softly approach to R* ….

· Inflation is being primarily fought with financial stability policy tightening rather than monetary policy tightening.

(Source: the Author)

The latest FOMC meeting minutes showed a clear understanding that the Fed continues to primarily tighten monetary policy with financial stability policy tools. There was a strong consensus to follow up on the pre-committed two 50-basis points rate hikes, with the view that the chaos created, in the capital markets, would exert a significant drag on the real economy. The inference is, that disinflationary perceptions would be inculcated into disinflationary expectations.

The recent guidance, from Fed speakers, is largely consonant with the consensus in the minutes.

The Bostic Put essayed: ‘Even firetrucks’ with sirens blaring slow at intersections ….

· The “Bostic Put” joins the “Waller Put” on the list of “Fed Puts” being extensively forward-procrastinated.

(Source: the Author)

With a growing market consensus, anticipating a recession, the various forms of “Fed Put” which have been provided, in extended forward guidance, have begun to be articulated with greater clarity. The objective behind the various Puts was to avoid a recession created by monetary policy tightening. This message has been lost, amid the market panic, so some clarity is required.

Atlanta Fed president Raphael Bostic has tried to provide clarity by stating that, data-dependent ceteris paribus, there is a good case to be made for pausing, to assess the economic damage, after a further two 50-basis points rate hikes.

In search of clarity, Bostic has taken a leaf out of Richmond Fed president Thomas Barkin’s book and turned essayist. The message from Bostic’s recent essay is that the inflation problem is more of a supply-side problem. It will become even more of a supply-side problem if the FOMC recklessly tightens monetary policy and destroys aggregate demand. This supply-side problem is beyond the scope of monetary policy. It is in the fiscal realm of elected policymakers. Bostic is hinting that “Build Back Better” should be directed at supply-side expansion and reform.

As Bostic allegorizes ‘even firetrucks’ with sirens blaring slow at intersections. By inference, the US economy is at a tipping point where aggregate demand may suddenly fall below constrained supply. Tightening monetary policy at this point is counterproductive.

· The FOMC may be sacrificing its credibility, in order, to lower price inflation with higher market volatility.

(Source: the Author)

Bostic has confirmed that the real monetary policy tightening tool, currently being applied, is a financial stability policy tool. Since he also confirms that inflation is everywhere a supply-side phenomenon, out of the reach of monetary policy, it is perhaps unsurprising that the FOMC is experimenting with financial stability policy to fight inflation. This mismatch of policy tools is a big risk. Evidently, based on the various “Fed Puts” that are doing the guidance rounds, and the recent FOMC minutes, the Fed is very uneasy about this experiment.

We’re all in this together ….

Kansas City Fed president Esther George can always be relied upon to say it the way it is, like it or not. In her latest speech, she made it clear that the Fed, and the Federal Government first counter-cyclically, and then pro-cyclically, created the demand side of today’s inflation problem. This was not helped by supply chain disruptions and a tight, skill-mismatched labor force. The Ukraine war has just doubled up on the inflation and growth risk.

With inflation so high, George does not feel that the FOMC has the luxury of waving various Puts around until the Fed Funds rate is around 2%. Getting to 2% will incur economic weakness. It is what it is.

San Francisco Fed president Mary Daly has just decided to guide with platitudes, sans dates, and estimates of when, and by how much, the FOMC will tighten, at this point. Consequently, she provides a rosy Soft-Landing scenario in which the FOMC “get the interest rate up...price stability restored and still leave Americans with jobs aplentiful and with growth expanding as we expect it to.”

Further soft-landing signals are desperately being thrown off by the New York Fed.

The “Fed Put”: A Hyperbolic act of self-preservation ….

The recent FOMC meeting minutes also highlighted the Fed’s approach to its balance sheet reduction process. This is where the soft-landing signaling occurred.

· The Fed may embrace Macklem Doctrine when it sees the unrealized losses on its balance sheet from the recent spike in yields.

(Source: the Author)

In the last report, New York Fed president John Williams confirmed that there is no appetite for the central bank to realize losses through outright security sales. This loss aversion is specifically strong in the case of mortgage-backed securities (MBS) holdings. In the case of MBS, there is a double whammy or convexity in the trading vernacular. The first whammy is that MBS prices fall by nature of the higher discount factor. The double whammy is that the underlying collateral, house values, also fall contributing to the fall in the MBS price. Evidently, Williams does not want the balance sheet to go there and add a triple whammy by selling MBS into a falling MBS market and a falling house price market.

The last report observed Cleveland Fed president Loretta Mester delicately opening the subject of unrealized losses, in mortgaged back securities, on the Fed’s balance sheet. Said losses could, potentially, be realized, through sales, as the balance sheet is wound down. The author didn’t perceive much appetite to take the losses in view of the associated greater loss of credible commitment incurred. Consequently, the author perceived an appetite from the Fed to support the bond market. This appetite has subsequently become voracious in the form of rhetoric and guidance.

(Source: the Author)

The New York Fed has taken the step of broadcasting its loss aversion through the inference that there will be a corollary soft landing for the economy. This broadcast was made in the New York Fed’s annual report on open market operations. The balance sheet is broadcast to be wound down over a period of three years, through the maturing of holdings rather than sales. The balance sheet will, hence, decline by roughly $ 2.5 trillion to circa $ 6 Trillion. The shrinkage of the balance sheet by a third, over three years, whilst large is also well spread out over time. The tightening impact of balance sheet shrinkage is, thus, diluted; one might even say muted. The legacy circa $ 6 Trillion balance sheet is a financial cushion, of significant size, especially in view of the fact that the Fed is already making noises about ending the rate hike cycle.

The New York Fed would like to frame the balance sheet issue as a Soft-Landing signal.

The UK Prime Minister would do anything for a Soft-Landing right now.

Stands the Church Clock at ten-to-three and is there Layer Cake still for tea?

UK Prime Minister Boris Johnson’s strategic misalignment with the New Multipolar World Order (NMWO) under construction, is finally getting the kind of editorial attention that can only mean one thing. This thing is regime change.

The UK Prime Minister will not go, it seems, without a fight. This will be bad for the New Multipolar World Order (NMWO) and worse for Britain.

Speaker Pelosi has already signaled that Britain will not be allowed to spoil EU-US trade relations and their bicameral vision of the NMWO. There simply is no place for Britain, and no exorbitant privilege either, as an equal of the two. The British PM would be well advised to take care. Instead of taking care, he gambles and plays the balance of power game, seemingly, to make Britain and/or himself seem more relevant than they actually are.

(Source: the Author)

The UK PM recently had his Eddie Temple Facts of Life moment at the hands of Speaker Pelosi. Madame Speaker politely informed the PM of which layer of the New Multipolar World Order (NMWO) layer cake he and Britain are in. It’s not near the top. Also, it’s a far cry from the far pavilions that the PM fondly imagines still exist in some corner of a foreign field that is forever England.

Britain has been relegated to the State level, of the Trans-Atlantic layer cake. Brexit, and the Irish Border question, have, effectively, severed relations between the British Government and the US Federal Government. The embarrassing situation, for all involved, means that the British Government must now re-establish political and commercial links with the US States in order to maintain ties with the nation as a whole. The first re-established contact was recently achieved in a new trade deal with the Indiana Senate.

· Britain conflates the Commonwealth regime with the concurrent G7 global governance best practice regime.

(Source: the Author)

Knowing the dubious proclivity, of the PM, for destruction, it is highly likely that Britain will soon cement diplomatic, and trade, relations with the old slave-owning Confederacy, from where the bandwagon and march towards Civil War, and four more years of President Trump, will begin. The blowback for Britain, and Johnson, will cement the UK’s emerging pariah status and a more desperate embrace of the Commonwealth.

The Special Relationship is over. Prime Minister Boris Johnson is at the bottom of the cake facing being forcibly removed altogether.

Johnson’s demise will have been hastened by the latest Partygate revelations and lurid photographs. His ousters, clearly, know how and when to play their cards. To regain the initiative, the Chancellor was forced to levy a windfall tax on energy companies. The knee-jerk move comes too late and is unlikely to fool voters. Further political capital, and exchequer revenue, are expected to be extorted from the shakedown of the private equity industry which now owns most of UK Ltd. This move will also alienate the PM’s traditional support base in the private sector and the City. In another knee-jerk response, the former Mayor of Londongrad now wishes to rain down more missiles on his former reptilian Russian benefactors.

With all this Robbin Hooding going on, there are bound to be sellers of Sterling and Sterling priced assets. Sensing a trap door opening up, underneath Sterling and UK assets (especially in the energy sector!), the government has strengthened its powers to intervene in acquisitions.