An Awkward Time To Admit That Inflation Is Everywhere A Monetary Policy Phenomenon

An Awkward Time To Admit That Inflation Is Everywhere A Monetary Policy Phenomenon

“Nothing vast enters the lives of mortals without a curse.” (Sophocles)

Summary:

· Ukraine is a diversion via which China’s Belt and Road runs into direct conflict with G7.

· Inflation is being primarily fought with financial stability policy tightening rather than monetary policy tightening.

· Inflation dynamics may have become structurally unhinged from their historically benign trend in October 2021.

· Thomas Barkin gets a credibility downgrade.

· Neel “Ex Culpa” Kashkari has lost his credibility.

Starting global conflict on the back foot, behind the curve ….

Just when the Fed should be aligning itself, and its balance sheet, with the US Commander in Chief’s global imperative, the US central bank is discovering some awkward home truths.

The FOMC may eventually come to the rescue, late, because it responded first with zeal, to the COVID-19 imperative and never stopped giving, until it was too late. Having paid the price for the FOMC’s indiscretions, with inflation, the US economy looks set to pay again through an economic slowdown.

America’s allies may also pay the price, as economic support is late arriving for them in dealing with the menace to the East.

The Eurozone, inside the Natozone, wrapped in the G7-Zone ….

Summary:

· G7 has canceled the 1970s narrative.

· G7 has canceled G20 and all multipolar initiatives associated with it.

· Regime change by Cancel Culture could be on the G7 agenda.

(Source: the Author)

The previous report discussed the G7 response, to the Ukraine situation, and the wider threat presented by the Sino-Russian takeover of G20. The military part of the G7 response has involved the re-affirmation of the NATO global fighting brand.

Il est ne le divin enfant (sic) ….

If the French are correct, in saying that revenge is a dish best served cold, President Macron has already overcooked President Putin’s Pastila.

(Source: the Author)

Prior to the NATO re-affirmation, it was noted that President Macron, egged-on by Angela Merkel, had been pursuing a dilution of NATO powers, within the Eurozone, to promote a closer alliance with Russia. Seemingly, after the Russian invasion of Ukraine, Macron and his failed initiative are now orphans.

With Merkel gone, Germany has renewed its commitment and military spending threshold to the full NATO membership level. Furthermore, this membership renewal will involve the purchase of American F-35s. Germany has, thus, fully re-aligned itself with NATO and G7, at the expense of the EU.

With all bets on Macron’s initiative off, Russia is swiftly diversifying its strategic military and economic options. The options in the West are no longer attractive.

Go East Young Oligarch ….

The Russian invasion of Ukraine is swiftly becoming the support act for the main event. This main event would appear to be an economic confrontation between the G7 and China. Capital flight and flows, in relation to the Ukraine crisis, are the medium of economic transmission of the main event.

Despite Chinese protestation that it is not overtly helping sanctioned Russians, slip the global dragnet, the latest FDI numbers suggest otherwise. If G7 sanction enforcers follow the money, they will ultimately find themselves in China. China’s Belt and Road initiative has a new notch and new diversion via Russia. Sadly, for China, these new developments will run directly into G7 obstacles. The remainder of China’s global Belt and Road infrastructure will, hence, suffer from the contagion from this Russian diversion. As the USA follows the money, President Biden is taking the view that China is aiding Russia and has threatened reciprocal economic sanctions.

China may, soon, be forced to choose between continued support for Russia or pursuit of its greater global ambition. Whilst it is deciding, global supply chains will ossify and inflation will be nudged higher. This latest nudge is, however, a clear global economic headwind of ominous proportions. Developed central banks, who are embarking on monetary policy tightening, should take note and tread cautiously.

#Price discovery by @CancelCulture (epilogue) ….

The last report discussed how G7 policymakers, and their regulators, were “canceling” commodity speculators, and the normal market price discovery process, which together were spoiling the prospects for the developed economy central banks to create the illusion of soft economic landings.

Since then, Mr. Market has understood that he is under attack from policymakers, regulators, and central bankers, and is liquidating as fast as he can before the next hiked-margin call. When the LME Nickel ring recently re-opened, prices immediately moved 5% lower, on thin volume, and trading was halted again. It was the inflation spiking speculative longs turn to get squeezed.

Those riveted to spiking oil and commodity futures prices, on their screens, should remember that the complete opposite occurs in the real world in times of crisis.

(Source: the Author)

So keen was Mr. Market to unwind, his global economic positioning/hedging, that he caused a complete dislocation in the VIX curve, whereby, the cost of unwinding option positions was higher than the cost of constructing the underlying index unwinding trades themselves. The price to unwind the option trades, hence, became larger than their constituent parts indicating, thereby, suggesting counterparty risk, and collateral and margin calls driving the price action. This chaos was exemplified by the price action in the Barclays iPath Series B S&P 500 VIX Short-Term Futures ETN (ticker VXX), a structured product that is supposed to mimic underlying equity market volatility. Barclays has canceled further issuance of the note and trading was halted as volume, and volatility, in the note itself was over 50% higher than its underlying constituents.

· Meaningless high spot commodity prices on screens are the reference point for meaningful discounts in the “constrained” physical markets.

(Source: the Author)

The contagion is spreading from the metals complex to the oil complex, with aggressive disinflationary intent.

With credit spreads blowing out, to recession levels, even before the FOMC had started tightening, the motive and propensity to cancel trades in the capital markets were also growing.

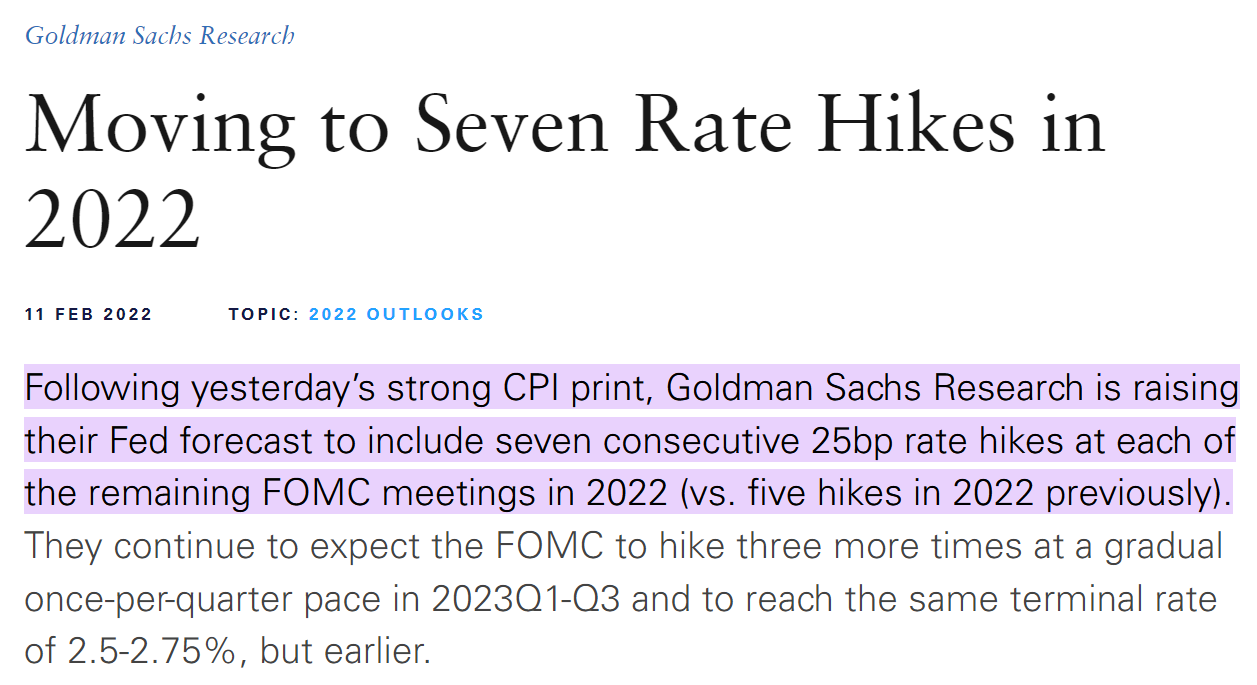

Some firms, like Goldman, are exploiting the chaos in what this author has called the “Big Long” moment.

Whilst talking up the prospect of at least seven rate hikes, this year, from the FOMC, Goldman simultaneously opines the risk to the global economy from Ukraine. The two commentaries are inconsistent on the first inspection. A closer inspection reveals consistency with an ulterior motive.

Never interrupt your opponent when he is making a mistake (sic) ….

Goldman is not the only one talking and positioning. Goldman is, however, positioning itself against the bearish crowd. This is a corollary Big Long move being undertaken by Goldman.

(Source: the Author)

Assets and commodities can be cherry-picked in fire-sales, which seems to be the object of the equivocal commentary exercise. Goldman, already, appears to be doing some cherry-picking in the physical Nickel space.

Inflation can also be manhandled lower in said fire-sales and appropriations. Talking the markets down, ostensibly, sounds and looks like Goldman applying the FOMC’s extended forward guidance with brio.

In the current disorderly market purge, the cheap (and apparently risky) debt of underlying commodity positions can be acquired for less than the intrinsic value of the commodities themselves. This is how Russian Oligarchs did it back in the day. Today this process is legitimized by the oversight of central banks and market regulators, with inflation axes to grind.

The situation in the markets is, potentially, larcenous and, potentially, a case of insider market manipulation, but it is impossible to prove so convincingly. This thesis is, however, an elevated probability rather than a paranoid suspicion.

Within firms, like Goldman, the compliance Chinese walls, which are supposed to separate conflicted business units, appear to be very porous in the current circumstances. Some firms, like Goldman, are adept at resolving these conflicts and compliance with Chinese wall issues in the interests of shareholders; often at the expense of some of the firms’ customers.

The winners and losers, in this great wealth transfer, seem to have been identified by the G7 policymakers and their central bankers. Firms, like Goldman, are simply aligning the markets, and their price discovery, with this natural selection process; whilst, simultaneously, aligning their trading P&Ls and creating shareholder value in the process.

· The Fed is encouraging Mr. Market to create and then converge higher spot volatility basis lower forward volatility.

(Source: the Author)

This author has previously suggested that the Fed wanted an inverted volatility curve term structure. The Fed has got what it desires, now, and should handle the fallout, carefully, to avoid a full-blown economic headwind from the capital markets. For this headwind to be avoided, spot volatility must converge lower basis the forward. The commodity markets, therefore, need to continue their collapse in price to deliver the lower inflation in the forward curve that the Fed desires. The current spike in spot volatility and the unwinding sell-off in spot commodity positions will do this, as long as it is not allowed to create an economic slowdown in its wake.

The economic headwind implied in the conditions created, by this volatility convergence trade, will then act as the call, and the catalyst, for the massive economic stimulus that ensues. Said economic stimulus has already been flagged, and named, North of the border in Canada.

Build Back a Better Macklem Doctrine And Disinflationary Growth Will Come (reprise) ….

(Source: the Author)

Whilst the FOMC wrestles with Mr. Market, and regulators assist by canceling the obstacles to a soft-economic landing picture, the US central bank is falling further behind the global growth curve. By default, the FOMC is, also, falling behind the global solution to the growth problem. The author has labeled this solution Macklem Doctrine in honor of its first adopter Bank of Canada Governor Tiff Macklem. Adherents to the doctrine believe that a fiscal stimulus, to the supply side, will engineer disinflationary growth by unblocking and expanding supply chains.

· The Fed may embrace Macklem Doctrine when it sees the unrealized losses on its balance sheet from the recent spike in yields.

(Source: the Author)

This author has, also, suggested that the FOMC may be prompted to accelerate its catch-up with the Macklem Doctrine curve by the appearance of unrealized capital losses, on its balance sheet, from the current spike in yields. Such unrealized losses create the specter of Fed insolvency. The insolvent Fed would potentially need bailing out. This would be ironic when it is assumed that the Fed was actually bailing out the US economy by providing its balance sheet on demand to the US Treasury. This chicken and egg insolvency debate is not something to be taking into an economic slowdown. The FOMC has a real pecuniary incentive to swiftly get back to expanding monetary policy.

The awkward moment of the realization, of the Fed’s solvency conundrum, has now been conjectured by JP Morgan. It is a little more than coincidence, that whilst Morgan is conjecturing, on the matter, the very actions of Mr. Market that are doing the questioning, through price discovery, are being manipulated and canceled in some cases.

“Supply-Side Keynesian” Yellen wishes to Build Back Better America’s disinflationary supply chain with a larger fiscal deficit.

(Source: the Author)

Morgan hastily concludes that the Fed’s losses will not be realized, in practice, but in fact, the much larger loss of credible commitment will. Presumably, this means that the US central bank will be exposed as the fiscal agency of the Federal Government, that it has become, rather than an independent monetary authority that it is Congressionally mandated to be.

Don’t bite the hand that feeds you, just smack it gently but firmly. (reprise)

The Fed’s predicament represents a much larger predicament for those whom this author calls the Masters of the Asset Class Universe. These alleged, Masters have been observed gently reminding the Fed of their mutualized symbiosis.

In previous reports, this author has chronicled how monetary policymaking has been sub-contracted out, to these private institutions, by the Fed has awarding reserve balance asset management mandates. Those who have argued that Quantitative Easing is a temporary provision of liquidity have ignored the fact that the subcontracting of reserve asset management, to the private sector, is a more permanent manifestation of it. This also represents a privatization of monetary policymaking by stealth.

The imputed private monetary policy managers receive huge fee income in line with their reserve asset management mandates. This income stream is now being threatened by the Fed’s alleged intention to scale back its balance sheet. Furthermore, the rise in yields that the threat of interest rate hikes has created also delivers unrealized capital losses to the private reserve asset managers. They are in crisis. But for them, every financial crisis ultimately has a silver lining since it begets a larger Fed balance sheet and lower interest rates.

One could cynically argue that Macklem Doctrine, and the huge fiscal stimulus it brings, which needs deficit-funding, is the next big earner for the Masters of the Asset Class Universe.

One could, further, cynically, argue that the Fed and the Masters are, hence, incentivized to get with the Macklem Doctrine thesis as soon as possible. Manipulating markets and canceling trades is, therefore, in both their interests; since it gets them to Macklem Doctrine sooner by way of falling inflation and slowing economic growth.

With the tension rising, it was time for the FOMC to show and tell its intentions and capabilities to deal with the competing demands on its policymaking decisions and balance sheet.

Some FOMC members acknowledge Macklem Doctrine, others don’t ….

· The FOMC wishes to be seen and heard as a tough inflation fighter.

· The FOMC may be felt as a tough inflation fighter only in March.

(Source: the Author)

Previously, this author had suggested that the March FOMC meeting would be the FOMC’s last chance to appear like a tough inflation fighter. The meeting lived up to this billing

Ostensibly, with its decision, the FOMC showed concern about inflation; but not enough concern to hike 50 basis points. The latest Summary of Economic Projections still depicts inflation as being transient, even though higher than the last projections. Economic growth projections are dismal, and unemployment hits a brick wall, and then gets worse in 2024.

Despite being “acutely aware” of the need to deal with price inflation, Chairman Powell did not lose sight of his growth mandate. Apparently, the FOMC is committed to avoiding a recession as it tackles inflation. It sounds like a soft-landing meme is under development.

Hitherto, it had been assumed that St. Louis Fed president James Bullard’s accelerated monetary policy tightening would be sequentially rolled out over the course of the next FOMC meetings. Chairman Powell’s commitment, to avoiding recession, effectively dilutes Bullard and his prescription.

Powell’s commitment, to avoid recession, is an acknowledgment of Macklem Doctrine. It is also an acknowledgment that he has some catching up to do with it. Bullard, however, remains unrepentant and will not acknowledge the imminence of Macklem Doctrine at the Fed. He, therefore, dissented, at the latest meeting, and then melodramatically gave his own reasoning for his actions.

Nailing his colors to the mast, of his leaking ship, Bullard has stated that he called for a 3% Fed Funds rate last year. He should have called louder, and he should have called back in March rather than late in the day in 2021 after the inflation horse was six months out of the stable.

Evidently, Bullard wanted 50 basis points, instead of 25, at the latest FOMC meeting, and is a bit miffed that he and his tightening plans are being quietly side-lined. Thus piqued, he gave his own explanation of dissent for the record. This explanation now sees him in favor of five 50 basis points rate hikes in five of the next scheduled six FOMC meetings this year. He will now stand, or fall, by what happens to growth and inflation going forward.

Bullard’s position will be supported by Fed Governor Christopher Waller. Waller has admitted that, had it not been for the outbreak of hostilities in Ukraine, he would have voted to hike rates 50 basis points at the latest FOMC meeting. Going forward, he fully expects to vote for 50 basis points hikes in several of the remaining FOMC meetings this year.

Bullard may have the last empiric laugh and the pyrrhic victory that goes with the levity.

If it is broke, you’d better fix it, quickly ….

Long live King Thomas, or at least until the March FOMC meeting!

Famous last words: “If you can keep your head, and say Holy Cow, when all of those around you are losing theirs, and shouting Katie bar the door, you should be the Fed Chairman my son!”

(Source: the Author)

This author has enjoyed the agnostic approach, taken by Richmond Fed president Thomas Barkin, to studying the current inflation problem. Thus far, Barkin had not drawn any meaningful conclusions that could radically change monetary policy settings. This has now changed.

One of Barkin’s staffers has come to two frightening conclusions about what has happened to US inflation since October 2021.

Firstly, it has been found that now inflation is pervasive in all prices of goods and services, rather than being concentrated in a handful of drivers.

Secondly, it has been found that the relationship between inflation and the distribution of price changes has recently broken down from its predictable behavior since 1995.

Frighteningly, in response to these two findings, it has been concluded that monetary policy itself has been the greatest dis-locator and disruptor of the traditional behavior of prices. This can only mean that the monetary policy response to COVID-19 is the culprit. The study infers that monetary policy must be swiftly tightened if the traditional behavior of inflation is to return.

Going forward, it will be interesting to observe if, and how, Thomas Barkin incorporates his staff research on inflation into his own guidance and FOMC decision making.

The arrival of Macklem Doctrine will be challenged by the Richmond Fed staff inflation study. Only the threat of imminent recession will militate in its favor, and prevent the FOMC from continuing to tighten monetary policy, in order, to return to the established inflation behavior from 1995 to date.

Barkin’s initial response has been to toe the FOMC line, thereby diverging from his own staffers. In the previous article, Barkin had been observed to want to get back to neutral as soon as possible, from where to (more safely) observe the behavior of inflation. His latest, collegiate, guidance shows him to be in less of a hurry, to get back to the neutral vantage point, despite threatening that he could hike 50 basis points at any time.

Clearly, if Barkin was in sync with his staffers, he would have voted for 50 basis points immediately. Evidently, he wishes to avoid the FOMC losing further credible commitment by appearing to panic and/or show internal division. Consequently, he toes the 25 basis point party line and proselytizes recession avoiding, and 70s repeat episode that goes with a more radical tightening of monetary policy.

Observing Barkin’s latest guidance, this author laments his loss of independent thought and the integrity that goes with it. Barkin must now be placed on the credibility watchlist, with his first downgrade, and the potential for a full loss of credibility.

Whilst waiting for Barkin, to lose his credibility, the recent rapid change in guidance from Minnesota Fed president Neel Kashkari may serve as a drum-roll. The drum roll may then be followed by a quick clash of the symbols to celebrate Kashkari’s theatrical loss of credibility.

Like Barkin, Kashkari is an essayist. Unlike Barkin, Kashkari has used his most recent essay to procrastinate rather than to apologize for getting his inflation call totally wrong. For those unwilling to plow through Kashkari’s bloviate mea culpa, suffice it to say that it’s actually an ex culpa.

In ex culpa, Kashkari doesn’t admit to being wrong. He, allegedly, remains right about inflation being transient. The problem is that it is not as transient as he first assumed. Apparently, this is not his fault but is, in fact, the collective fault of all the economic agents in the US economy.

Despite this extended transience, Kashkari has hiked up his economic projections for rate hikes by more than 100 basis points. He now sees the need to move to the tighter side of the neutral rate, in order, to observe the extended transience; just in case it is permanent. Watching Kashkari try to pull off his written gymnastics, in a public speaking engagement, will be painful for all, but the most sadistic, to endure.

Simply watching and reading Kashkari, it is hard not to think of the Richmond Fed staffer’s conclusion that monetary policy has created a dislocation in the benign wake of the inflation continuum. Kashkari is not swiftly trying to put the singularity genie back into the bottle.

Summary

· The Fed is behind the domestic economic curve but up to date with America’s global agenda.

· Mr. Market’s risk-on positioning will require tighter financial stability policy rules, and their unintended consequences, rather than net-tighter monetary policy conditions.

· The Fed has finally, and appropriately, decided to Qualitatively Normalize whilst continuing to Quantitatively Ease at a slower pace.

· The Fed has chosen to frame inflation risk in terms of conventional interest rates and not the size of its balance sheet.

· Perhaps, because he has been bullied by the Fed, and lost money, Mr. Market has, so far, been happy to dissociate inflation from the size of the Fed’s balance sheet.

(Source: the Author)

Clearly, market regulators have assumed that the inflation genie is out of the bottle. Rather than wait for the FOMC, to tighten monetary policy, these regulators are physically tightening liquidity, and financial stability policy settings, in order to trigger a slide in commodities and the inflation linked to them.

Back in November 2021, just as the Richmond Fed staffers allege that inflation was becoming unhinged, this author observed that the Fed was contemporaneous, with its global obligations, yet behind the domestic inflation curve. The extended levels of risk asset prices, observed at the time, suggested to the author that financial stability policy would be tightened. It was also assumed that the FOMC would Qualitatively Normalize whilst continuing to Quantitatively Ease.

Revisiting this November 2021 thesis today, with inflation spiking higher, one can see that the tightening of financial stability policy is being increased and that Quantitative Easing is being rapidly clawed back. Regulators and FOMC members are panicking. In addition, they are under pressure to get the job done, quickly, because America is falling behind its global economic obligations.

If you can’t serve yourself, who can you serve?

Individuals and FOMC members have got in the way of effective monetary policymaking. In some cases their reasoning and motivations are dubious.

Neel Kashkari’s disingenuity may run closer to treason. This author has noted Kashkari’s embrace of balance sheet expansion and the subcontracting of monetary policy, from the Fed, to systemically important asset managers i.e. Master of the Asset Class Universe in the past.

Alleged Fed insider dealing is a distracting minor misdemeanor from the related murkier business of the privatization of US monetary policymaking.

(Source: the Author)

It was also noted that Kashkari, along with the disgraced (and retired) Vice-Chair Clarida, were alumni of the same systemically important asset manager. To give Kashkari the benefit of the doubt, with the benefit of hindsight, one could say that he was misguided and has, since then, realized the error of his ways. The cost of this epiphany, in terms of inflation and lost economic growth, falls, asymmetrically, and un-equitably on those US economic agents whom he blames for messing up his inflation call. Karma, Kashkari style, would appear to be larcenous also.

Perhaps central bankers need to have the same kind of liabilities for their actions as company executives. Haven’t they been getting away with it for too long?