“TMI”: Diverse G7 Domestic Economic Tributaries Converge Into The Global Macklem Doctrine Rubicon

“TMI”: Diverse G7 Domestic Economic Tributaries Converge Into The Global Macklem Doctrine Rubicon

“To Muddle, or to Macklem? That is the question.” (Unattributed)

Summary:

· Whilst united, on Ukraine, at the global level, G7 nations and their central bankers are diverse at the national level.

· The internally conflicted Eurozone will become a managed command economy for the duration of its structural transformation towards a Federal Republic.

· The UK will become an austere economy with an ungovernable polity.

· The US will have a barnstorming attempt at a soft economic landing.

· Macklem Doctrine now has rules of engagement for G7 members to converge economic performance on.

Hitherto, G7 had been successfully opining the thesis of its winning strategy to reclaim economic prosperity for democracies. The release of the indiscriminate Global Regime Change virus, by G7, and the domestic responses to it may change this narrative somewhat.

The recently released Global Regime Change virus is highly contagious and wildly indiscriminate.

(Source: the Author)

G7 may stand united, at the global level, on Ukraine, but its members’ domestic economic policies are not as well coordinated as its Russian sanctions. Ironically, this economic decoupling may take the sting out of both the inflationary, and recessionary, forces that have been unleashed by the conflict. It may also exacerbate them, though.

It’s the (Global) Economy, Stupid (sic) ….

Sadly, multi-polar indigestion, for all involved in the digestion of Ukraine, will come from a global recession, rather than unilaterally for Russia through sanctions per se. Justice will then be served on the political grandstanders, as they are turfed out of office because of the recession. Justice may never be served on President Putin if he retains his grip on power during the recession and beyond it.

Amusingly, the central bankers will survive, as they always do during and after global crises. Indeed, they may be greeted as saviors when they start the massive monetary policy stimulus, again, to counter the recession that they had a hand in creating. Politicians come and go, but central bankers live eternally, or at least their expanded balance sheets do.

(Source: the Author)

This decoupling, and muddling along, is more driven by the domestic political survival instincts, of the G7 leaders, than any deliberate strategy. These domestic survival instincts, and skills, have been sharpened by the Global Regime Change virus that they have, recently, released at the global level. The default posture of muddling along, under the current circumstances, does not appear to be a deliberate choice; but it may turn out to be the optimal one, in hindsight.

Whilst they muddle, domestically, G7 policymakers must accept the consequence, of slower economic growth, globally. Muddling may, thus, buy time for the central bankers, to get their inflation-fighting acts together, just in time for the next combined (and globally coordinated!) fiscal and monetary policy expansion.

Fortunately, for G7 muddlers, there exists a guide for the perplexed muddler. This guide has been written by the Bank for International Settlements (BIS). In addition, to writing the guide, the BIS also has promoted the man who will coordinate it to the starring role.

Many Rivers to Cross, but they can’t seem to find their way ….

The problem, for those who exclusively derive their signals from price action, is that they lack context. In times, like this, context is very meaningful.

One never steps in the same river twice; and this river may be structurally changing course, rather than mean reverting back to its previous one.

Mind the (Missile) Gap: Crossing the Rubicon, by way of the Atlantic and Pacific Oceans ….

The Anglo-Saxon-ANZAC cadre, within G7, give it a name, AUKUS, is starting at the global level and sailing upstream from there.

Presumably, in response to the successful testing of hypersonic missiles, by China, and their recent use by Russia, in Ukraine, AUKUS members will, henceforth, expand their military fiscal deficits on hypersonic missiles spending. Meanwhile, nominally, pacifist Japan is rapidly de-pacifying in order to spell JAUKUS.

The EU is bringing up the NATO rear, as usual, to make it JAUKEUUS, or is it J’AKEUUUS? Josep Borrell, the EU’s de facto Foreign Minister, and de facto nuncio to the court of the de facto Chinese Emperor, recently had some very undiplomatic things to say about Sino-EU relations. Said relations have, demonstrably, just reached a new low point, diplomatically classified as a “deaf dialogue”, on the subject of Ukraine.

Allegedly, there is a missile gap that needs filling. By inference, there is also a missile shield that needs building. So, in total, that’s double the fiscal spending. Or is it fiscal spending squared?

The last time that the old missile gap ruse was used, to boost fiscal spending, it turned out to be a false premise. By the time the falsehood had been discovered, the twin US fiscal and trade deficits had destroyed the Gold Standard. To be fair, though, the Soviet Union was also economically prostrate, but the West didn’t know (or wish to acknowledge) it at the time. This time around, enforced Russian prostration has just kicked off. This time around, also, China’s pockets are deep and its economy is integrated into global supply chains so the impact will not be localized.

Crossing the Rubicon, by way of the Dnieper ….

· The war in Ukraine is the catalyst for irreversible structural changes in the global economy.

(Source: the Author)

The last report discussed the irreversible structural change which has been catalyzed by the war in Ukraine. Germany was noted to be in the vanguard of this movement within the Eurozone. This German driver of transformation is also evident at the Executive Board level of the ECB. This is critical since the Executive Board provides the context and framework, and hence the devolved credible commitment, from the political executive, which allows the Governing Council to execute independent monetary policy decisions. This critical governance feature of the ECB is important, in such times as this, when inflation says that the ECB should be tightening monetary policy but the geopolitical situation says that monetary policy accommodation should persist.

With the current context in which the Governing Council operates conflicted, it was appropriate that the Executive Board should provide some guidance and structure. This was, recently, and elegantly provided by Executive Board member Isabel Schnabel.

Schnabel’s latest guidance, effectively, instructed Christine Lagarde, and her team, on how they should resolve their internal conflicts, in line with the imperative of the EU’s political executive, whilst adhering to the principle of central bank independence. It is okay to be independent, but devolved legitimacy trumps this independence, especially in times of crisis. This trump card, thus, obliges the ECB to work with, not against, the political executive. This card, hence, sets some clearly defined red lines on the limits of ECB independence.

Schnabel’s guide, for the perplexed Governing Council members, was a clear explanation of where the political executive is taking the Eurozone. It was thus a guide on where devolved legitimacy, and independence, oblige the Governing Council to follow.

In Schnabel’s words, the Eurozone is heading in the direction of a structural change that will make it more energy-efficient and independent. Confluent, with this structural transformation, is a disengagement with the current political executive in Russia and also potentially China. This transformation is inherently, inflationary in nature. This inherent inflation will also destroy aggregate demand as the mix of economic inputs changes. Consequently, once again, the ECB must work with the political executive to enable the transition, as it did in the response to COVID-19.

Essentially, as Schnabel sees, and therefore the Governing Council must also see it, this is an issue of “Managing Structural Trade-Offs”. The application of the word structural clearly speaks to the irreversible transformation underway in the Eurozone economy.

The transformation of the Eurozone is, thus, a given that will trade higher inflation for independence. The ECB Governing Council will engage with the political executive in trying to make the cost of structural transformation, in inflation and interest rate terms, as minimal as is politically acceptable as possible. The market will not be allowed to decide on what the price terms of this trade-off will be. The market will be forced into acceptance of this fait accompli by the combined strength of the ECB and political executive.

Currently, this trade-off obliges the Governing Council to withdraw monetary policy stimulus. This can only mean that a counter-balancing fiscal stimulus is coming. This also means that greater intervention, in the operation of Eurozone markets, to allocate resources in line with the transformation imperative, is to be expected. Financial speculators in commodities beware.

Essentially, the Eurozone is going to be a managed, command economy, for the duration of the structural transformation envisaged by Schnabel. This command economy will run significant transformative fiscal deficits.

Schnabel’s Executive Board colleague, and Chief Economist Philip Lane, has, also, metaphorically underlined the Eurozone’s transformational crossing of the Rubicon, with his characterization of the current phase in economic history as a “watershed”.

As it happens, Germany is also in the lead when it comes to transformative fiscal deficit running.

Crossing the Rubicon, by way of the Rhine ….

Germany recently announced that fiscal “Black Zero” has become the latest casualty of structural economic regime change. German wages adjusted for inflation, through the social security system, in order to compensate workers for the higher cost of living, will not be allowed to creep into higher tax brackets. Thus, German workers will have a real boost to their disposable incomes that the Federal government cannot claw back through the income tax system. It can, and probably, will be clawed back through inflation-driven sales taxes if the German workers are lured into spending their windfall.

Perversely, therefore, this form of fiscal stimulus may lead to continued/expanded consumption that will exacerbate price inflation. Structural inflation may, hence, get baked into the German economy as an unintended consequence of the political imperative, to buy political capital, with a policy of strength through fiscal joy. No wonder Bund yields are ascending.

The rise in Bund yields is nothing in comparison with that in BTPs.

Crossing the Rubicon, by way of the Tiber ….

Italian Prime Minister Mario Draghi has resorted to the kind of noble lies that he used to tell when he was ECB President. Back in the day, at the ECB, Draghi used to print money whilst promising to stop printing in the future when the specific economic crisis was over. As the Eurozone lurched from one crisis to the next, Draghi just kept printing.

Draghi’s same modus operandi is now evident in Italy, but this time, in relation to fiscal policy. Draghi confidently expects to expand fiscal policy, under the premise that he will balance the budget over a three-year time horizon when growth returns. Clearly, if Italy lurches from one crisis to the next the original premise is false.

The ECB’s own professional economic forecasts, certainly, question Draghi’s premise.

If the ECB’s economic forecasts are correct, there will not be sufficient GDP in the bloc to pay down any extra debt incurred over this three-year budget-balancing period. In the absence of growth, the ECB will then be provoked into compressing Italian yield spreads that are responding to Draghi welching on his promise to pay.

Draghi’s prescription is, hence, a good model of how the Eurozone’s fiscal profile will evolve over the next three years; and what the ECB will do about it.

Crossing the Rubicon, by way of the Eider ….

The winds of war, and fiscal change, originating in Russia, are also blowing across the Baltic into Germany’s Teutonic neighbours on the Northern bank of the river Eider. The fiscally prudent Danes have recently removed their structural fiscal deficit cap of 0.5% of GDP because of the Russian threat. Countercyclical fiscal stimulus and structural defence spending stimulus will now burst through this original ceiling, thereby, dragging bond yields with them.

Crossing the Rubicon, by way of the Svir ….

On the other side of the Baltic littoral, on the Karelian peninsula, the Finns are following their EU partners’ responses to the Russian economic and military headwinds.

Finland is now sweating an expanded fiscal, and military budget, in peacetime so that it does not have to bleed heavily in wartime. Finnish bond yields are rising accordingly, adding to the rising bond milieux in the Eurozone and EU.

“Project SPQE”: Crossing the Rubicon, by way of the Main ….

Ironically, it is the ECB that is portraying the economic future of the Eurozone rather than the political executive. The ECB has taken the dangerous stance of nudging national governments to break fiscal debt limits. This nudge is part of the bigger nudge towards deeper economic integration outlined by Isabel Schnabel. COVID-19, and the Ukraine war, are the new drivers of this manifest destiny.

The ECB’s Executive Board has effectively sanctioned this next phase of the Eurozone Project, according to the latest commentary by board member Fabio Panetta.

Panetta has set the precedent for this next stage, by laying out the crises, that have driven this imperative, from as far back as its genesis in the Roman Empire. He is, also, quick to note that the burden will be shared, between fiscal and monetary policy, so that the burden is not felt painfully by the people of the Newest Rome. This is code for deficit monetization, and price controls, to make inflation appear to disappear.

ECB Vice President Luis de Guindos has set the scene for the imminent next chapter. This scene involves the coordination of fiscal and monetary policy, to create a European Superstate, first amongst global equals, with a scaled-up economy that will withstand future global crises.

The visions, of both of these central bankers, infer an expanded ECB balance sheet to enable the process with ubiquitous, and infamous, “favourable financing conditions”. SPQR requires SPQE. Hints about SPQE are already circulating, even before the current expected monetary policy normalization has occurred. The next SPQE will, allegedly, be deployed to compress diverging sovereign yield spreads that have already become a growth sapping headwind.

The ECB, in fact, is deliberately ambiguous about its plans. On the one hand, Governing Council member Yannis Stournaras says that the ECB will do “whatever it takes” to fight inflation. But, on the other hand, De Guindos and Panetta say that it will do whatever it takes for an economic union. Clearly, Eurozone policymakers intend to conflate the two, potentially, conflicting directives. Egregious rule and market bending are portended by such ambiguity. This ambiguity is just like some Eurozone countries taking Russian gas and others sanctioning it, yet all remaining under the Eurozone umbrella.

This ambiguity does not so much imply that the ECB doesn’t have any plans, but rather that it will just make things up as it goes along, from one crisis to the next. It also implies that the central bank will deliberately circumvent, to the point of breaking, the traditional price discovery process and operation of capital markets.

France is the first mover, in the next phase of Eurozone integration. Taking advantage of the dip in asset prices, caused by the Ukraine invasion, French banking giant Credit Agricole has bought into the rich Italian region of Lombardy, with a 9.2% stake in Italy’s third-largest lender Banco BPM.

Neither De Guindos nor Panetta, have thanked President Putin for injecting momentum into the process that they described.

A breakaway former province, of the Newest Republic, has different dreams of empire.

Crossing the Styx, by way of the Thames: He came, He saw, He Fracked …. He was Nuked!

The Perfidious Albion, as its name implies, is following the time-honoured tradition of playing the balance of power game, through Brexit-aligned assonance rather than dissonance. UK policy is, therefore, ideologically out of sync with its European neighbours. It is also rhyming and not repeating with its own past.

Dodging the bullet, of Partygate, in the hail of bullets from Ukraine, UK Prime Minister Johnson has used the smokescreen, from the conflict, to disguise his party’s dogmatic pursuit of Sir Keith Joseph’s inflation solution; which was previously sold, to the populist Sun-reading masses, by Rupert Murdoch, as a humble shopkeeper’s daughter from Grantham’s diary.

A shrunken public sector, and commensurately shrunken fiscal deficit, are assumed, by the Green Card-carrying Monetarist Chancellor Sunak, to be the keys to fighting inflation and rising interest rates. The Chancellor also hopes that his dogmatic adherence to Joseph Doctrine will allow him, and his Non-Dom wife, to ascend the greasy pole that is currently wobbling, perilously, as the former Gauleiter of Londongrad disports himself at its summit. Greasy pole dancing has never been so challenging for disciples of the New Generation.

The first time, when Joseph Doctrine was christened, the Union was less fissile, though just as divided, and had more abundant North Sea Oil and Gas to see it through the economic crisis. Today, however, the North Sea is less bountiful and may fall into secessionist Scottish hands. In addition, the Nimbys, who live on top of abundant shale hydrocarbon deposits, are being less than cooperative; because they value the price of their houses higher than the cost of heating them. A similar Nimby fate awaits the revisiting nuclear initiative.

The Tories have never been big on alternative energy, in any case, because it was suspiciously assumed to be a Euro-Trojan Horse, from which to capture the nation’s sovereignty. Consequently, the UK economy has an energy gap, in its economic policy mix, which may swallow the whole mixture.

The UK economy will, henceforth, feel painful austerity. This may feel like something that would have seemed like a sunny day, at the beach, for those who have lived through the rainy days of Thatcherism.

The Bank of England’s Doves are already anticipating the carnage and the real economic damage ahead. Sir Jon Cunliffe now estimates that the impact of the Ukraine situation, on the UK economy, is most likely to be disinflationary. This is a twist, indeed, since most other reputable economists assume that it will be inflationary.

Unfortunately, for the Doves, the Hawks have also stirred, thereby, setting up the prospect of intense infighting. This infighting may then lead to a loss of consensus policy execution that, further, undermines the Bank’s credibility.

Monetary policy thought leader, and Monetarist zealot, Bank of England Chief Economist Huw Pill has casually pulled the pin out of the grenade in the great debate. Pill believes that central banks have got away with QE, until now, because they have been “lucky”. This luck has prevailed in the form of disinflationary forces, for long enough, to convince the lucky central bankers that a new paradigm exists. Suddenly, all bets, on said paradigm, are off. Consequently, QE may be taken out of the toolbox never to be used again.

Crossing the Rubicon, by way of the St. Lawrence ….

Things should be great if you are the Canadian Prime Minister. The substitution of democratic Canadian hydrocarbons, for undemocratic Russian hydrocarbons, should be the icing on the cake for an economy that is leveraging off the fiscal and monetary excesses of its Southern neighbour. So how has it all gone so sadly wrong for Justin Trudeau?

In answer, to why read inflation.

Now what?

In answer, to now what, also read inflation.

Prime Minister Trudeau intends to splash a further fiscal stimulus on acquiring political, that is to say populist, capital through subsidies and price controls. If Trudeau is a Liberal, then this political handle obviously has a different meaning in Francophone Canada. It certainly does not mean laissez-faire. This does, however, mean liberal spending behaviour, which heralds more fire on the economic flames that will raise inflation, bond yields and interest rates, not necessarily in that order.

Not Crossing the Delaware, by way of the Potomac ….

The consensual, popular, fiscal policymaking mixes, in Germany, Denmark, and Finland are things that will make President Biden green-eyed with envy. Currently, he faces a partisan political backdrop and a central bank that is leaving him, and the economy, high and dry, in the pursuit of fighting inflation.

Biden and the US economy must watch, with open mouths, as the Fed attempts a soft economic landing, to briefly refuel, in order to take off with a large monetary stimulus payload. This attempted soft landing is becoming a bit of a barnstorming show.

Not Crossing the Rubicon, by way of the Missouri ….

St. Louis Fed president Jim Bullard is the most likely to crash land, rather than soft land, the US economy. In his view, the FOMC is “behind the curve” and must now raise interest rates another 3% this year. Ukraine, and/or other global issues do not concern him.

Bullard did, however, shine a light at the end of the tightening tunnel. The Fed, apparently, has not lost its credible commitment because Mr. Market, via the forward curve, believes that it will successfully tighten monetary policy. Notwithstanding, this vote of confidence, the FOMC must now be seen to deliver at least 3% of rate hikes as consideration.

One of Bullard’s colleagues, even, imagines that the tightening, implied in the forward curve bargaining, is over already.

Just Cross the Rubicon Already, by way of the Hudson ….

New York Fed president John Williams has adopted an outcomes-based approach to his guidance, which, presumably will also be his approach to FOMC voting.

Williams starts with the premise (and assumption) of a soft-landing, that has not yet happened, and works back from there. Consequently, he can be more flexible in responding to the incoming growth and inflation data. Consequently, since this incoming data is strong on both counts he can swing with the 50 basis points hikes crew. The important thing, however, is not the 50 basis points but, rather, the flexibility that Williams has to change his mind, and his guidance, going forward. He has, also, and wisely, not set a time frame on when this, assumed, soft landing will be achieved, thereby, giving him even more wiggle room.

Manifesting desirable, outcomes-based, forward guidance seems to be, the current stock in trade, of FOMC members who have an affiliation with the San Francisco Fed. Evidently, this is some form of behavioural finance, perceptions framing, technique in which they profess to excel.

Already Across the Rubicon, by way of the Golden Gate bridge ….

San Francisco Fed president Mary Day is, already, fondly imaging herself on the other side of monetary policy tightening river crossing. Apparently, there is no recession to be seen on this side and inflation has been subdued. This is more like wishful thinking than outcomes-based forward guidance. In the meantime, the US economy will just have to get wet with monetary policy tightening and hope that it does not drown.

Not Crossing the Rubicon, by way of the Delaware ….

Philadelphia Patrick T. Harker, at least, has the integrity, not shared by all his FOMC colleagues, to admit that the Fed is partially to blame for the current inflation spike. The other culprits are fiscal policy and supply chains.

Harker, therefore, intends to make amends, for the FOMC’s part in the inflation debacle, by “methodically” tightening monetary policy. In doing so, he does not intend to compound the Fed’s infamy by triggering a recession.

Not Crossing the Rubicon, by way of the Chattahoochee ….

Atlanta Fed president Raphael Bostic, like Harker, is methodical. In his method, he hopes that monetary policy will not need to be tightened beyond the neutral rate, without saying exactly what this neutral rate level is.

Not crossing the Rubicon, by way of the Chicago River ….

Chicago Fed president Charles Evans is in the same boat as Raphael Bostic. He also hopes that the arrival point, for monetary policy tightening, will be the neutral rate.

Not Crossing the Rubicon, by way of the James, the York, the Rappanock and the Potomac ….

Famous essayist and Richmond Fed president Thomas Barkin is, literally, all over the place. His travels are taking him to the grassroots communities, within his district. From these vantage points, he can understand how his regional economy is performing. He has found plenty of Federal stimulus, but little bandwidth and capacity to productively put it to work. Neither has he found obvious local sources of capital, so it is Hobson’s Choice with Federal funding.

Barkin is, thus, by default, a student of the supply-side. His studies, of the supply-side, and the recent Ukraine shock, have prompted him to scale back his zeal for getting back to the neutral rate asap. A misfiring grassroots economy, plus an exogenous growth shock, are growing headwinds. Consequently, he is less likely to vote for 50 basis point interest rate hikes going forwards.

Inflation/Job Security Conflation ….

· The Fed is diverging from the White House and may even, officially, blame the Federal Government, for the current inflation spike, under oath.

(Source: the Author)

The last report discussed the growing potential threat of a legal challenge to the Fed’s execution of its dual mandates, by nature of the fact that the central bank has ignored its inflation mandate, for too long, at the behest of the White House.

A growing list of FOMC members, including Pro Tempore Chairman Powell (“PTC”), have been observed to be preparing their written depositions, in the form of extended forward guidance, for their day on the stand. A point has been reached at which some FOMC members are insinuating that fiscal policy, and not them, is to blame for the current inflation spike.

This tale has taken a special twist in the specific case of Fed Governor, and nominee Vice-Chair, Lael Brainard.

Know your meme (sic).

It should be remembered that Brainard was giddily chasing inflation target overshooting and broad inclusion, when the FOMC should have been withdrawing monetary policy stimulus, in March 2021, as the committee officially acknowledged that the economic rebound was way beyond its expectations.

Federal Reserve Governor Lael Brainard also signaled that the Fed is refining an old tool in order for it to become a sharper tool, to focus its inclusivity agenda, under the general heading of pandemic response. Brainard’s emphasis on the Community Reinvestment Act (CRA), in a recent webinar on post-pandemic reconstruction, hinted strongly that it will become a significant tool in the Fed’s toolbox going forward from here.

This sharpening of the CRA, also, infers that a new Inclusivity Mandate is being assumed by the Fed de facto rather than mandated by Congress de jure.

(Source: the Author)

It should, also, be remembered that Brainard was the key person in the Fed’s broad inclusion movement. This role involved her repositioning the Community Reinvestment Act (CRA) as the monetary policy tool with which the Fed would pursue its, not Congressionally approved, subjective broad inclusion mandate, as a sub-heading of its employment mandate.

Today’s inflation spike, and Brainard’s Vice-Chair nomination, are the compromised unintended consequences of her previous Dovish zeal. Brainard has much to answer for. In response, she is emphasizing how she will deal with the consequences of her previous actions.

Fast forwarding, to today, Brainard’s application to become Fed Vice-Chair is compromised by her broadly inclusive, inflation overshooting, track record. Consequently, Brainard has rewritten her resume, and re-invented herself, even citing Paul Volcker as her inspiration, as a credibly committed inflation fighter. There is, however, no evidence of this credibility from her previous behaviour and guidance, quite the contrary, as it happens.

In her latest guidance, Brainard has, therefore, played the role of the committed inflation fighter to the best of her abilities. This cosplay has involved the complete reworking of her broadly inclusive character.

Ostensibly, through the disguise, of investigating the impact of inflation, across different income groups, Brainard has been able to spin a new narrative that reinvents her Dovish broad inclusivity in a Hawk costume. Allegedly, since inflation falls hardest on those in need of broad inclusion, Brainard will broadly include them in an economic slowdown, through monetary policy tightening, that will deliver their salvation through lower prices for goods and services which they consume.

Basically, it’s tough love from Brainard these days. Apparently, this tough love is what Congress needs to hear, in order, in the beauty pageant of the Vice-Chair nomination process. The tough love meme reminds this author of the recent Kim Kardashian faux pas, in which those in need of broad inclusion were told how to comply with Kim’s interpretation of the employment mandate. This author can’t wait to hear Brainard’s tough love, less than, broadly inclusive views on the Great Resignation; especially when monetary policy tightening starts to reduce employment opportunities.

Keep Calm and Muddle Your Way Across the Rubicon, by way of the Missouri ….

Through all the theatrics and ass-covering, currently underway at the Fed, the demeanour and guidance of Kansas City Fed president Esther George have been exemplary. When her colleagues were overshooting and broadly inclusive, George was suspicious. Now that they are aggressively Hawkish, she is cautious. She does not dissent, from their view, she simply wishes it to be executed in the way that does the least harm to the US economy.

In do least harm mode, George has recently reprised the need to include balance sheet size, and reduction, into the equation with rate hikes. She has recently repeated this opinion, in the light of incoming inflation and growth data which has shown an acceleration in both.

Doing the least harm would seem to be the acme of skill, not only for career-minded central bankers but, also, for political leaders, elected and/or otherwise.

Muddling through is, however, not what is being proscribed by G7 policymakers and their central bankers. They have a plan to cook an omelette and serve some cold revenge dishes for dessert. But, to make an omelette, someone’s eggs need to be broken. To serve a cold desert there, also, has to be a loser or losers. Fortunately, for G7 members cooking instructions exist to distinguish the winners from the losers.

Ready, Steady, Cook ….

· The war in Ukraine is the catalyst for irreversible structural changes in the global economy.

· Some G7 central banks are self-isolating, from the regime change virus, to save themselves by fighting inflation.

(Source: the Author)

The last report suggested that the global economy is entering a period of irreversible structural change.

· Macklem Doctrine (GHOS Protocol) will roll out in global venues soon and run for three years if successful.

(Source: the Author)

The last report also suggested that the global central banking response would be coordinated, with supply-side policies, by the Bank for International Settlements (BIS). This coordinated response would come under the broad heading of Macklem Doctrine.

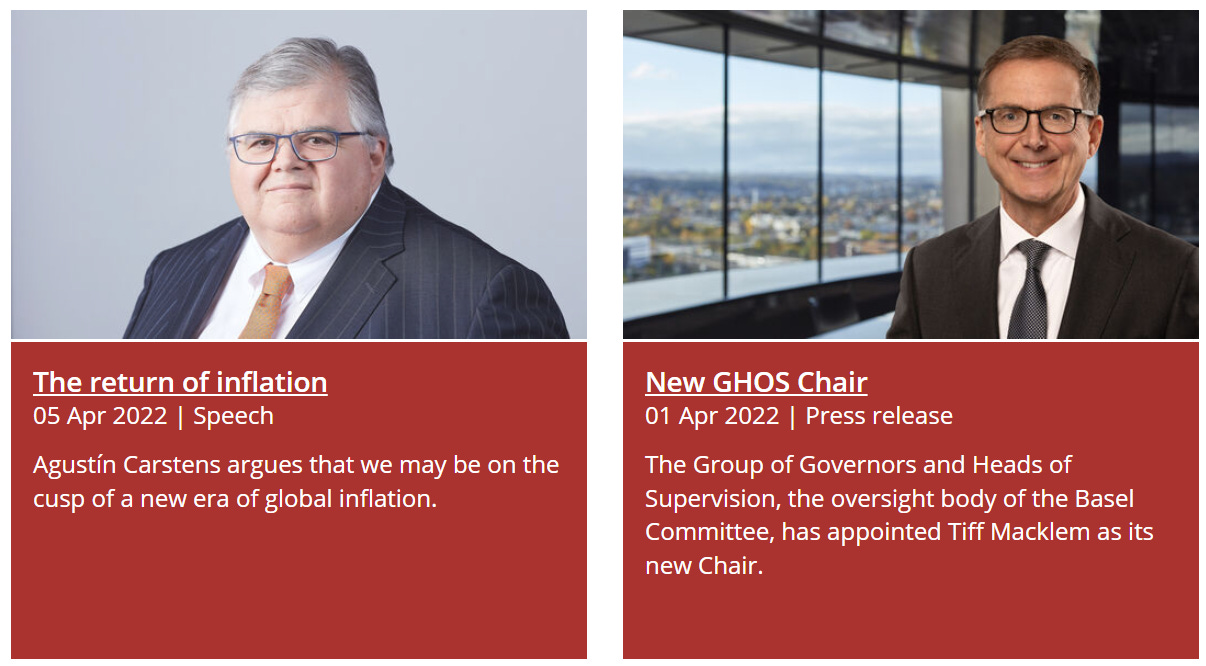

As a precursor to Macklem Doctrine being rolled out, over an envisaged three-year time horizon, its namesake author Bank of Canada Governor Tiff Macklem had recently been installed in a coordinating position at the BIS.

Since then, the BIS has advanced to contact with the global structural change, and its enemy/enemies. BIS General Manager Augustin Carstens has recently set out the rules of engagement for all the central bankers involved.

In essence, the rules were articulated by Carstens, thus: “After more than a decade of struggling to bring inflation up to target, central banks now face the opposite problem. Inflation is back. The rise in inflation reflects the rapid and goods-intensive economic recovery from the Covid-19-induced recession – bolstered by highly accommodative fiscal and monetary policy – which supply has been unable to fully meet. We should not expect inflationary pressures to ease soon as many of the forces behind high inflation remain in place and new ones are emerging. There are already signs of increased price spillovers across sectors and between prices and wages, as is common in a high-inflation environment. Moreover, the structural factors keeping inflation low in recent decades may wane as globalisation retreats. The inflationary paradigm may be changing. Central banks need to adjust to this new environment, not least by raising policy rates to more appropriate levels. The world economy must learn to rely less on expansionary monetary policies.”(Author’s emphasis)

Carstens has spoken to the irreversible structural change, suggested by this author, and its inherent inflationary nature. Central bankers have been told that they must tighten monetary policy, beyond the neutral rate, for a brief period of time. The political executive has been warned that fiscal stimulus must be narrowly aimed at genuine supply-side targets, rather than populist subsidies. The case for military spending thus needs embellishing, in some detail, by AUKUS, but no doubt its members can extemporize with alacrity. Globalization, via non-core G7 initiatives, is now in the retreat.

Maybe, from beyond the grave, Sir Keith Joseph has ghost-written the script of Macklem Doctrine (GHOS Protocol). Chancellor Sunak, evidently, seems to think (and hope) so.

The global rules of the game, for the G7 team playing Macklem Doctrine, have, thus, been delivered; and its eponymous coordinator has been given a three-year contract. As one would, logically, expect the seeds of Macklem Doctrine would initially germinate into green shoots close to home. Thus, it is no surprise to find that a Canadian banking CEO has been quick to jump on board the bandwagon.

Canadian Imperial Bank of Commerce (CIBC) Chief Executive Officer Victor Dodig, has recently challenged policymakers to focus on generating fiscal revenues by investing in growth rather than through taxation. This sounds like the Ghost of Fiscal Past Keynes rattling his chains. It also sounds like the Ghost of Fiscal Future, Tiff Macklem rattling his sabre.

By the way, Tiff, Vladimir Putin’s Dacha still needs painting, capisce?