Beggar Thy Neighbour Friend-Shoring, From Behind The Curve: Federal And Commonwealth Games

Beggar Thy Neighbour Friend-Shoring, From Behind The Curve: Federal And Commonwealth Games

“Beggars can be choosers. Or can they?”(Unattributed)

Summary:

· Oligopolists are currently defeating Capitalism, possibly for the last time.

· G20 Beggar Thy Neighbor Friend-Shores G7, and itself.

· Whilst President Biden is beating Chairman Powell, in the race to be blamed for inflation, President Putin may ultimately win by technical default.

· The miscommunicated/misunderstood “Powell Put” has joined the eponymous list of Fed guidance procrastinations.

· The Fed has lost the initiative and implicitly accepted that it is behind the curve.

· A Key Signals proprietary indicator signals that the FOMC is, once again, totally off with its timing, this time, on monetary policy tightening.

· Only a 1990s Greenspan repeat will rebuild the Fed’s credibility.

· Only repeat 1990s-style data will deliver a 1990s Greenspan repeat.

· Faced with populist protest, Eurozone policymakers transfer wealth, for votes, and simultaneously sell Federalism.

· Britain conflates the Commonwealth regime with the concurrent G7 global governance best practice regime.

When Stagflation is everywhere, and always, a greed phenomenon …. (reprise)

The last report discussed how a handful, of Oligopolists, in the transportation sector, of the global supply chain, helped to boost global inflation, to where it is today, in their enthusiasm to make up for profits lost during the 2020 COVID lockdown. A new round of profiteering is set to be launched unless policymakers and/or a global recession intervene.

In Ocean, revenue increased 64pct. to USD 15.6bn during Q1 as strong rates more than offset a 7pct. decline in volumes. Revenue for the full year is expected to continue to be strong as the increase in freight rates on our long-term contract portfolio will add approximately USD 10bn to revenue in 2022 compared to 2021. This will more than offset the significant increase in costs, which were up 21% in the first quarter given higher fuel costs and inflationary pressure on network and container handling costs.(Author’s emphasis)

(Source: Maersk)

The Maersk shipping line recently boasted of its ability to bake higher long-term inflation expectations, into the global economy, by raising long-term contract prices in the face of short-term declining volumes. Costs were up 21%, volumes were down 7%, but revenue was up 64% thanks to aggressive rent-seeking. Bravo! But there’s not exactly a lot of competition in this space, is there? Shooting fish in a barrel seems to be more like shooting fish in a shipping container in this case.

The company also recently announced that it has lost $700 million due to the Ukraine war. From this author’s perspective, this represents 700 million reasons for Maersk to try and recoup its losses with higher prices. In the unlikely event that central bankers are paying attention, they will note that creating recessions, with tight monetary policy, will, potentially, create a more rapacious response from the Oligopolists that boosts inflation even further.

In the event that policymakers are paying attention, they will note that the pricing formulas within oligopolies require their scrutiny.

In the Eurozone, this policymaker observation is already occurring. Unfortunately, a political, rather than economic, solution has been offered. Political solutions, sadly, lead to mispricing and misallocation of resources. The conclusion appears to be that wealth transfer, from Oligopolists to consumers, is preferable. This preference yields political capital for the policymakers and also advances the European Project. This is, presumably, why it has been adopted.

The lack of proportionality of the cost, volume, and pricing metrics of Maersk’s business practice appears to be wildly out versus the business environment in which it operates. It would appear that the company, simply, decided that it wanted to recoup its 2020 COVID losses asap, upfront, and then solved backward to get customer prices that achieved this objective.

This divergence, in business metrics, has clear implications for global inflation. It also has clear implications for the strategy recently adopted by G7 nations to confront the, perceived, economic threats emanating from Russia and China. Maersk would appear to be exploiting the G7 strategy. Indeed, the greater the global tension the greater the opportunity for Maersk. The misalignment of values, and strategies, appear to be egregious to the point of threatening the G7. This won’t be the first time that Capitalists have got in the way of Capitalism. Strictly speaking, Oligopolists are defeating Capitalism. It may, however, be the last time.

There may be blood ….

The Oligopolists, especially the Oiligopolists, have also got in the way of G7 plans to defeat Russia and simultaneously “Friend-Shore” supply chains, out of China, and back into friendlier territories.

Ostensibly, the Oligopolists have a lot of sunken capital, give-it-a-name “Skin in the Game”, and income manifested in the existing global economic order and its supply chains. This makes them inert. This inertia may inform, but does not excuse their rapaciousness. They are therefore an obstacle to the G7 plan.

This author has noted G7 policymakers’, and their enforcers’, combined abilities to cancel obstacles that get in the way of its plans. The Oligopolists must, therefore, be in G7’s crosshairs.

· Price Discovery Control is the G7 solution to the Oligopolists’ inflation threat to Macklem Doctrinaire Friend-Shoring.

(Source: the Author)

This author has, also, suggested that the defeat of the Oligopolists would be more easily achieved by the application of anti-monopoly legislation. There are signs that the world’s greatest Oligopoly is staring down, potential, G7 cancellation.

Like Lazarus, the eponymously named “No Oil Producing and Exporting Cartels Act” (NOPEC) is making rejuvenated progress in Congress. If it were to be legislated into life, the Department of Justice would, legally, be able to prosecute OPEC cartel members. Clearly, the current economic situation incentivizes Congressmen, from either side of the aisle, to buy political capital, and the chance of re-election, by passing the bill. As will be seen later, the Democratic Representatives have the strongest incentive. Even the mere presence of the draft bill may be applied, as a threat, to persuade OPEC to take a less pro-Russian stance in its pricing policy.

Having addressed the Oligopolists, G7 then needs to work on its “Friend-Shoring” game. The results, of the initial attempts, at “Friend-Shoring”, have been mixed.

G20 Beggar Thy Neighbour Friend-Shores G7 ….

Both walkouts, however, left a significant critical mass, including some G7 members, to negotiate with Russia. The rump G17-ex Anglo Saxon bloc, still, remains a medium of dialogue that the Anglo-Saxons can interface with. One may, thus, infer that G7 has softened its attitude towards G20 also. Having initially wished to break up G20, over Russia, and China, G7 now wishes to “friend-shore” some of its members.

(Source: the Author)

The attempted process of “Friend-Shoring” by which G7 relocates global supply chains, from China, into friendly G20 democracies has begun with India. On behalf of G7, German Chancellor Olaf Scholz has extended an invitation to PM Modi, in addition to some other Asian and African G20 satellite nations. Presumably, this is because India is availing itself of cheap Russian Crude and aligning itself with the BRICs.

PM Modi sets the price, of Indian BRIC fidelity, at 70$ per barrel of Russian crude. India will, apparently, trade morality for cheap hydrocarbons. It is not yet known what price the Indian PM has extorted from the Germans, and other G7 nations, for his nation’s tradable loyalty. This marketplace is what currently serves as diplomacy in the world of nations that is “Friend-Shoring”.

Bridgerton Revisited: “Now in Injia’s sunny clime, Where I used to spend my time ….”

(Source: the Author)

With Britain, the Indian hustle has involved the provision of IT jobs, and immigration visas for Indian nationals, in addition to the scrapping of trade deals, with other nations, where the scrapping will benefit India. Presumably, therefore, this will be how it works for Germany and other G7 nations.

Beggars, apparently, can be choosers. Or can they?

Such pecunious fidelity, in the global arena, however, comes at the price of the loss of credibility, and trust, from those who are being hustled. The cost of this hustle falls due later and falls heavily when it falls.

Mas Que Nada ….

This author has noted how the BRICs have an antipathetic attitude, towards the New World Order of “Friend-Shoring”, which has been recently endorsed at the IMF/World Bank Spring Meetings. The B part of the quartet has now become active. It is interesting to note that the B is far more conciliatory than the aggressive R and C, and also less overtly pecuniary than the venal I.

Brazilian presidential front-runner Lula was critical of President Biden for not doing more to deflate tensions before the war in Ukraine began. This criticism is not, however, unequivocal support for President Putin. Lula does not want to fight an election and the USA simultaneously. He wishes to play the peacemaker and the global statesman, thereby maintaining good relations with G7 and China’s alternative global order. Lula is hedging. He is also beggaring his BRIC neighbors. This indicates that Russia and China are on the back foot, economically and politically speaking. India, as advertised by PM Modi, is up for sale to the highest bidder. The BRICs cannot afford to lose Lula, and have him as a competitor.

The beggar-thy-neighbor process of “Friend-Shoring”, and hustling, especially in the Asian time zone, is going to be complicated. Evidently, India’s new regional best friend Australia thinks so.

A rainy-day fund for when your luck dries up ….

Seemingly, the Australian government, initially, takes a somewhat protectionist’s dim view of the “Friend-Shoring” process. The Aussie sovereign wealth fund has been instructed to invest at home. The reason given is the view that rising inflation, and rising interest rates, make the global economy look risky. This reasoning is credible and further supported by the fact that the RBA has just embarked on its interest rate hiking process. This global combination of factors also makes Australian assets look risky to foreign investors. Clearly, there is an element of creating a domestic savings cushion to potential capital flight out of/away from Australian assets. This cushion then, also, means that Australian interest rates do not need to rise as high to attract global capital. In essence, this is what sovereign wealth funds are supposed to do in times of domestic crisis.

And then there is China.

One would confidently expect that the relocation of supply chain components, away from China, would benefit Australia as the obvious first relocation point of contact. The relocation out of China is, however, an obvious economic headwind to China that will logically, then, blow through to Australia, since the latter is one of China’s most important trade partners.

For example, the Australian wine industry has suffered a massive hit from China which has not been compensated for by other trade partners. On that note, therefore, a general global economic war of attrition with China, via “Friend-Shoring”, is a derivative headwind to the Australian economy.

Whatever the real reasoning, Australia is preparing for the worst by creating a financial cushion. Clearly, the Australian government intends to raid its sovereign wealth fund, to prop up its domestic economy, before considering raising debt, as it did in the COVID-19 crisis, to do so.

Australia used to be known as the Lucky Country, which never experienced a recession in its economic history, even as its trade partners suffered from the swings in the global business cycle. This trend has now been broken, and Australia is no longer lucky.

The Eurozone is also preparing a rainy-day fund, for the kind of “Friend-Shoring” that will create a federal superstate, with a bit of luck and a big nudge from Russia.

From Eurozone to Weimarzone, by way of Kyiv: Step Two ….

· The internally conflicted Eurozone will become a managed command economy for the duration of its structural transformation towards a Federal Republic.

(Source: the Author)

The Eurozone’s predicted transition, towards managed command economy Federal Republic status, has received new impetus from events in Ukraine. The project has, recently, run into domestic obstacles, at the national level, from within Eurozone nations.

May Day kicked off the traditional round of protests from organized labor. Noticeable in the milieu, this year, were ordinary consumers who were concerned about the inability of their salaries to match rising prices. Eurozone governments have used subsidies, and price caps, to control energy prices. They may now attempt to do the same thing for goods in the consumers’ basket.

Italy is the perfect example of a Eurozone government’s response to political and economic unrest. Italy is a Republic constituted by weak, ephemeral, coalition governments. To sustain their political franchise, Italian politicians must appear to lead their voters by following them.

Italian Prime Minister Draghi’s response, to the crisis, has involved a simple transfer of economic wealth from the beneficiaries of inflation to those who are suffering from it. Consequently, taxes on the energy sector have been raised and energy prices have been controlled. In addition, tax breaks have been given to energy-intensive sectors of the economy. Italian economic winners, and losers, are, thus, being politically chosen rather than through the market. The apparition of a massive misallocation of capital and resources presents itself. Currently, the Italian economy appears to be outperforming the German economy as a result of Draghi’s intervention. The corollary story is that this is all costing the Italian government more in interest costs on its debts. Hence the Potemkin economic façade is unsustainable in the long term.

In the long term, however, salvation, in the form of a New Rome, maybe just around the corner.

“Project SPQE”: Crossing the Rubicon, by way of the Main …. Bring me my (European) Shield.

PM Draghi is not just a Prime Minister, as it happens, he is also a custodian of the European Federal Project. His domestic economic strategy must, therefore, be seen as a blueprint for how the European Federal Republic would operate. It is, hence, likely that other Eurozone nations will align their monetary, and fiscal, regimes with Draghi’s model, thereby, enabling the ultimate Eurozone Republic to be achieved smoothly.

France already operates a system of energy subsidies, that is transferring wealth from the electricity providers to the consumers.

Germany’s historical experience, with the invisible hand of state allocation of productive assets, and labor, has informed the elected representatives just how this New Republic may, ultimately, play out. Essentially, the outcome is a Fascist re-construct that the current German Federal Constitution can defend itself against. German politicians, therefore, agonize over fiscal wealth transfers inconclusively. It is, heartening to know that the principles of democracy remain alive in at least one part of the European hinterland.

Evincing his Federalist intentions and capabilities, PM Draghi has called for European sovereign nations to relinquish their veto powers, on war-waging, at the EU level, to a higher supernational political authority. Maybe Draghi sees himself as the Commander in Chief of this Federal war-wager one day.

Panetta has set the precedent for this next stage, by laying out the crises, that have driven this imperative, from as far back as its genesis in the Roman Empire. He is, also, quick to note that the burden will be shared, between fiscal and monetary policy, so that the burden is not felt painfully by the people of the Newest Rome. This is code for deficit monetization, and price controls, to make inflation appear to disappear.

(Source: the Author)

Draghi’s henchman, and current ECB Executive Board member, Fabio Panetta cryptically alludes to this higher authority as the “European Shield”. This is not the first time Panetta has pushed his thesis.

If a nation loses its right to autonomously declare and wage war, arguably, it loses its sovereign status. Draghi is, therefore, arguing for the destruction of European sovereign nationhood. Vladimir Putin is trying to do the same thing in Ukraine. The symmetry is perfect.

The Federal Republic of the United States, also, risks losing its sovereignty through partisan disintegration. Consequently, waging war on foreign soil is an opportunity to bind the nation together.

If you don’t shoot the messenger, who do you shoot? (reprise)

· The Fed is diverging from the White House and may even, officially, blame the Federal Government, for the current inflation spike, under oath.

(Source: the Author)

The last report discussed the conflation of inflation, and poor political leadership, in the unfolding blame game between the Federal Reserve and the Federal Government.

The latest FOMC 50-basis points rate increase was broadly expected and, thus, meaningless in the context of the blame game. What happens next is important. The FOMC’s track record in handling what happens next is poor and is getting worse by the day.

From this author’s perspective, the Fed lost the plot and misread the inflation and growth situation back in March 2021. This transgression was occasioned by the Fed’s willing incarceration in the economic policy prison of Janet Yellen. The incarceration obliged the FOMC to adopt monetary policy settings consistent with a pro-cyclical, combined, fiscal and monetary policy stimulus.

The Fed had pre-committed to a new monetary policy framework, obliging the central bank to ignore rising inflation in the short term. To compound the error, the more Wokophile FOMC members, insisted on framing the “Great Resignation” as a justification to be “broadly inclusive”, and to err on the side of easy monetary policy, in order, to create more attractive employment conditions to attract the quitters back.

The corollary story is that loose monetary policy boosted portfolio values which put the Great back into the “Great Resignation”, thereby, making resignations look more attractive than work. In addition, generous COVID-19 fiscal support, and intervention, put the “Broad” back into the ranks of the “Broadly Included”.

Fast-forwarding to today, the “Great Resignation” has just gotten Greater, and inflation is at decennial highs. The Wokophiles have, suddenly, become Hawks and, now, exclusively, blame the Federal Government’s fiscal broad inclusion for creating the Great Inflation.

Former Fed Governor Randal Quarles has, already, prepared his deposition by opining that the tightening should have begun in September 2021, coincidentally, just before he left in December 2021. Hindsight is 2022 vision for Quarles.

More hypocrisy, in the furtherance of absolution, has been added to the milieu by disgraced, alleged insider dealer, and former Fed Vice Chair Richard Clarida. Clarida was a famous, now infamous, architect of the Fed’s Flexible Averaging Inflation Targeting (FAIT) strategy, at the heart of its new inflation target overshooting monetary policy framework. His portfolio, apparently, did exceedingly well as his day job provided the Alpha along the way to his enforced early retirement. Evidently, Clarida is in cash, these days, and looking for a market dip, to buy, in addition to clearing his name by blaming his former colleagues and boss. Now, he advocates that his former Alpha providers should go 1% beyond the 2.5% neutral rate asap.

In practice, therefore, it appears that both the monetary and fiscal policy executive are complicit in the chain of events leading to the present. Having shut the economy down, in response to COVID-19, both overreacted and overstimulated. This overreaction is acceptable since it is human. The failure to address the overreaction, and the ensuing cover-up, is unacceptable. The current blame game is, sadly, typical, however.

There are, fortunately, signs that the blame game is becoming less acrimonious. This recent concord may have something to do with the fact that both parties now accept that the inflation, which they are in part responsible for, is now a growing economic headwind. This headwind is being felt, initially, by those on the economic margins. TransUnion’s recent earnings report informed that defaults are rising for those with the lowest credit scores. Stagflation is picking off the lowest fruit on the credit tree of Liberty.

The tightening of monetary policy, through inflation, is, hence, already, working most effectively on those who can least withstand it. Worst of all, said worst sufferers have gone deeper into debt, to fund the base survival level of consumption that they can ill-afford. Tightening monetary policy, then, pushes them over the edge and effectively abandons them. For this to occur with a sitting Democrat President would be unprecedented and politically unacceptable. FDR would disapprove.

The Fed and the Federal Government are obligated to address both the inequality and the looming economic slowdown. Their collective challenge is to do so with precision; something they have failed to do in the past without igniting greater inflation for all.

If the latest FOMC meeting is any guide, the Fed will fail to fulfill its obligation. The meeting was a collective failure to execute a simple, well flagged, and widely anticipated, 50-basis points interest rate hike; along with a statement of commitment to continue until the 2.5% target neutral rate was achieved.

The FOMC’s failure represents a further loss of the initiative, and credible commitment, in the face of a suspicious audience.

The FOMC’s latest problem was not with its statement. The statement was concise and consistent with a commitment to attempt a soft-landing, under turbulent conditions. The problem occurs when FOMC members open their mouths. The Fed Chairman is, perhaps, the greatest problem in this regard.

It’s the “Powell Put”, but not as we know it….

· The “Bostic Put” joins the “Waller Put” on the list of “Fed Puts” being extensively forward-procrastinated.

(Source: the Author)

This author has noted the various forms of “Fed Put”, doing the rounds, of late, in the form of the eponymous “Waller Put” and “Bostic Put”. Ostensibly, all the Puts are promises by the Fed not to kill the economy with tightening.

The “Powell Put” recently joined the eponymous list. Most observers believe that the Put was written when Powell stated that 75-basis point hikes are not being “actively considered”, whilst the economy will experience “some pain”, going forward, as the FOMC hikes. This is not the case.

The 75-basis point retraction, in fact, backfired, spectacularly, by intimating that the Fed Chair has, already, given up the long-term inflation expectations fight. The long end of the yield curve, dutifully, crapped out and the curve steepened with disastrous consequences for risk assets. The forward curve now discounts a 75% probability of a 75-basis points rate hike in June, at this time of writing.

After Powell’s disaster, it then fell to Fed Governor Christopher Waller and St Louis Fed president James Bullard to try and save the day. They failed. In essence, the two had been set up to fail because they had accepted the barbed invitation to opine on the topic of "How did the Fed get so far behind the curve?" at a conference about “How Monetary Policy Got Behind The Curve And How To Get Back”. The failure was then completed by their failure to rebut the two assertions, unequivocally, when given the opportunity to do so. No defense was offered, thereby signaling acceptance.

By accepting the invitation, and the subject matter, the two speakers implicitly accepted the assumption that the Fed is behind the curve. The best that they could have done, therefore, would have been to estimate by how much. This estimation would, at least, have been some kind of extended forward guidance of substance and import. Alas, there was no estimation, thereby, widening the perception gap with and suspicion of Mr. Market.

· Unrealized balance sheet losses may have just triggered the Macklem Doctrine embracing “Fed Put”, in the form of the “Waller Put”.

· The “Waller Put” signals that the FOMC will not kill the “Build Back Better” and “Make More In America” booms.

(Source: the Author)

Waller has his own version of the “Fed Put”. This is a commitment not to tighten so far as to trigger a recession. Since Powell had tried and failed to say the same thing, there was no hope for Waller to retrieve the situation by repeating it.

If you accept that you are behind the curve, then, by default, you cannot also write an economic Put and hope to be taken seriously.

Waller got off to a bad start by implying that Mr. Market has got ahead of the curve, rather than that the FOMC has fallen behind it. Evidently, his original Put was directed to close this gap and it didn’t work.

Waller, then, swiftly, retracted his Put and went about trying to explain how he had totally got his monetary policy calls wrong, since March 2021, when the economy started “to rip”, in his own words.

For anyone who cares, Waller believes that his broadly inclusive view of the labor market, through the prism of the employment mandate, “in real-time”, prevented him from applying the brakes in the face of an inflation spike, also “in real-time”. From a child, this would be laughable. From a grown man, this would be unacceptable. From a Fed Governor, this is egregious. If, and when, Congress holds the Fed accountable, Waller will get eviscerated if he repeats this performance.

· Neel “Ex Culpa” Kashkari has lost his credibility.

(Source: the Author)

Waller’s ex-culpa was almost as unpalatable to endure as that previously given by Minneapolis Fed president Neel “Ex Culpa” Kashkari. Kashkari now meekly opines that the FOMC must deliver on its promise to tighten monetary policy. He also notes that Mr. Market has already tightened financial conditions significantly for the Fed. Kashkari thinks that being data-dependent is better than moving interest rates to where Mr. Market already thinks that they should be. By insinuation, rather than implicitly, Kashkari signals that he thinks Mr. Market has gone too far. Mr. Market would say that the incoming inflation data justify his zeal. Kashkari, thus, still, has yet to regain some lost credibility.

James Bullard stood no chance because he is already on record for wanting to hike 75-basis points. To say that he was satisfied, with the latest 50-basis points move would, thus, be hypocrisy not much short of perjury. This handicap, of his own making, did not prevent him from loyally trying to support his Chairman and colleagues, though. The Fed, and its credible commitment, are, clearly, under assault. Bullard’s attempt at loyalty was, however, half-hearted, thereby, evincing a strong self-preservation instinct on his part.

Bullard’s weak defense, against the accusation of being “behind the curve”, defaulted back to his prior equivocal baseline guidance on the subject. Consequently, his recent musings on the subject were rehashed and given today’s date in order to make them appear timely and fresh. On the one hand, of the Taylor Rule, the Fed is far behind the curve. On the other hand, of the Fed’s own subjective extended forward guidance curve, the Fed is not so far behind.

Empathy with the Rate Hike Devil ….

· James Bullard no longer has credibility.

(Source: the Author)

Bullard’s equivocating would be fine, if he had not also gone on record for wanting a 75-basis points rate hike. The fact that he only got 50-basis points, at the latest FOMC meeting, thereby, implies that the Fed has slipped, at least 25-basis points, further behind his curve. The fact that Bullard failed to say this, says everything about his loyalty. This loyalty, however, may come back to bite him in the proverbial.

Famous last words: “If you can keep your head, and say Holy Cow, when all of those around you are losing theirs, and shouting Katie bar the door, you should be the Fed Chairman my son!”

(Source: the Author)

On the subject of a potential 75-basis points rate hike, Richmond Fed president Thomas Barkin has emphatically slammed it back on the table. Barkin, apparently, “would not rule anything out”.

· Bullard’s Greenspan panegyric and Nabiullina’s lament are confirmations of the policymakers’ 1990s model hiding in plain sight.

(Source: the Author)

Bullard’s delicate balancing act, between supporting the FOMC consensus whilst remaining true to his own words has reached back in time to the 1990s. This reach has involved a form of regressive extended forward guidance, that has embraced Alan Greenspan and his tactical tightening back in 1994. This is interesting to this author, primarily, because of a similar frame of reference. Bullard’s reach is, hence, a confirmation signal for this author. This author can empathize with Bullard’s current predicament, whilst not sympathizing with the Fed’s failure to act in March 2021 when things started to get out of hand.

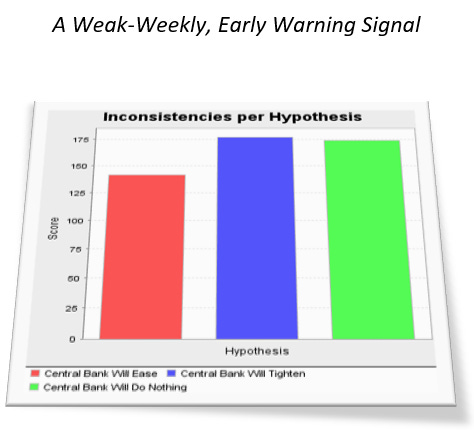

If the 1990s frame of reference is apposite, the US economy must be at an inflection point where inflation has already begun tightening monetary policy for the Fed. A Key Signals proprietary indicator has just signaled that this point has been reached in the first week of May.

The “Powell Put” Key Signal ….

The real “Powell Put” was written, at the post-FOMC meeting press conference, in answer to a question about the tight labor market. Chairman Powell’s answer revealed the way that the Fed is understanding the incoming labor market data.

The Fed’s approach to the labor market is holistic, if nothing else, in that the central bank looks for context in the incoming labor market data. Consequently, the mismatch in skills and job openings is of greater significance to the Fed than the aggregate level of tightness in the labor market. If the mismatch is not addressed, the tightness will always be there. This implies that the Fed is committed to working with the Federal Government to address the mismatch. In practice, this means that the Fed will be committed to supporting Federal stimulus programs which have a clear supply-side mission to address the mismatch. The Fed’s interpretation of its employment mandate has become nuanced, in order to inform its application of its inflation mandate. The nuance is supply-side in focus.

This author is particularly interested, in the “Powell Put” signal, because it confirms a weekly, proprietary, Key Signals indicator that has just signaled that the FOMC should be easing monetary policy. The signal informs that a Fed easing should be the least unlikely scenario, based on the indicator’s inputs from the first week of the new month. The signal also suggests that the Fed is, once again, totally off with its timing, this time on monetary policy tightening.

This author’s suspected “Powell Put” supports the proprietary signal by underlining the Chairman’s fumbled misgivings, despite his commitment to a series of interest rate hikes. If a recession were to occur, swiftly from here, the Fed would be to blame. Adherence to the rate hike schedule raises the probability of recession going forward.

The author has also noted the sudden, yet slight, change in tone of the Fed’s most vociferous critic. This change in tone is also a useful context for the recent Key Signals proprietary indicator’s recent weak signal. Larry Summers recently remarked on seeing some softness in the labor market of late. Whilst he does not cite this as a turning point, it is a weak signal, of sorts, that the economy and, more importantly, inflation is softening.

· The 1990s global economic scenario is hiding in plain sight.

(Source: the Author)

This author suspects that the FOMC is trying to be perceived as reminiscent of the Greenspan years, circa 1994. St. Louis Fed President James Bullard, in a recent panegyric to Greenspan, has also tried his hand at framing current perceptions through the 1994, alleged, belle epoque frame. The nudge is gaining traction, as observers strain to see something positive in the apparent fin de siecle.

The recherche aux 1994 temps perdu is starting to filter through to the analysts and strategists, in the investment community, although, perhaps, out of sheer desperation rather than successfully nudged inculcation.

The Federal Government has already been inculcated. In fact, it seems to have done some inculcating of its own.

We’ve been expecting you (late) Chairman Powell ….

The Biden Administration seems to have anticipated the Fed’s nuanced approach, and Chairman Powell’s chaotic behavior, towards its inflation mandate through the prism of its employment mandate. The risk of recession from an overzealous Fed tightening also seems to have been anticipated by the White House.

· US “friend-shoring” will be achieved with “Build Back Better” and “Make More In America” fiscal drivers.

(Source: the Author)

The Biden administration continues to be pro-cyclical and broadly inclusive. Biden’s “Build Back Better” and “Make More In America” initiatives have been recently conjoined with a Student Loan debt forgiveness program. All these deficit boosters are compounding alongside the slowly expiring Federal response to COVID-19, the proceeds of which have now been devolved to State and local governments. In summary, there is a strong fiscal stimulus tailwind. This tailwind is also inflationary.

The fiscal tailwind requires sustenance if it is to have any stimulative impact, at an affordable interest rate cost to the Federal government. Prior to the inflation spike, the Fed was happy to oblige this sustenance with its balance sheet. Post inflation spike, in the current blame game, the Fed’s balance sheet is neither available nor is the affordable rate of interest.

With some supply-side nuancing, and earmarking of Federal stimulus programs, however, the Fed, and its balance sheet, may become more readily available. This affinity will grow, further, if inflation falls and the economy slows.

Political emphasis on the supply-side component, of all the deficit-financed fiscal stimulus programs, is required if the Fed is to be entertained in accepting that they are disinflationary in nature.

If an external, and existential, threat, which drives the supply-side initiative, can be found, then, the process of aligning fiscal deficit with the Fed’s balance sheet can be made easier. An existential threat, which constrains supply chains, thereby increasing inflation, is even better.

Vladimir Putin’s house needs painting too Tiff, capisce?

(Source: the Author)

If only the Fed and the Federal Government could find someone else to blame for the global supply chain woes and inflation. If blaming this someone also required disinflationary, deficit-financed, supply-side investment then both could stop blaming each other, and get on with the financing.

Which brings both to the war in Ukraine.

Shootin’ Putin ….

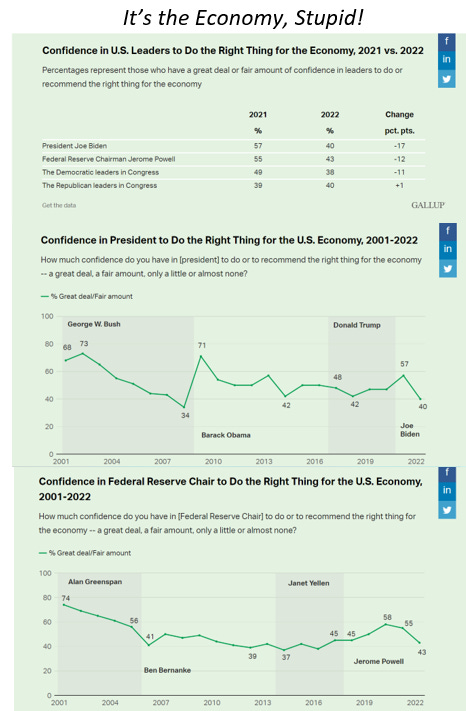

Gallup has recently provided further empirical context to the US inflation blame game.

In a clear race, to the bottom, President Biden has the edge, over Chairman Powell, in being blamed and removed for the Great Inflation. The highly bifurcated partisan influence on the data is equally important. Republican dissatisfaction with the Federal Government is extreme. Ironically, Republican-leaning Fed Chairs do not seem to do well, seemingly, because they tighten monetary policy and trigger financial crises.

Quite simply speaking, America needs a President who can be trusted, on both sides of the aisle, and a significant economic/political diversion on which to build consensus trust. Clearly, the Ukraine War and wider conflict, with Russia and China, are the lowest fruits on the “tree of liberty” that will require ritual cleansing, “with the blood of patriots and tyrants”, in order to be picked by the trusted US President.

Britain has always tried to resolve its conflicts, with tyrants, through urbane legal means, before resorting to violent bloodshed. Essentially, this process represents global governance best practice. This is G7 global best practice. This best practice is, allegedly, the modus operandi of the Commonwealth.

Come (from London) Mister Tallyman ….

Day-O, Day-O, Daylight Come: Black Gold, Banana Republics and Old Habits ….

The American thirty-year narrative involves the funding and creation of a bipartisan consensus from the perceived Chinese threat via Latin America.

(Source: the Author)

The key intelligence topic of the disintegrating British Commonwealth, and related potential Bay of Pigs moment, in the Caribbean, has been under increasing scrutiny from this author. The first Crown intervention, in the BVI, was discussed in the last report. Subsequently, it has now been confirmed that this sunny place, for shady finance, may be governed directly by London for the next two years.

The Commonwealth has been saved, for now, and the cause of global governance best practice may have been advanced. The natives are not happy, though. Presumably, Russian Oligarchs and other financial miscreants, who are viewed suspiciously by G7 compliance teams, are not happy either. What is incorporated in the BVI, and gets laundered in BVI, may no longer stay in the BVI. London is not exactly a paragon of virtue when it comes to money laundering, but at least the bad guys, who are aligned with the G7 good guys, will be allowed to continue to prosper.