Q1: Stagflated By Oligopolists

Q1: Stagflated By Oligopolists

“If you are not part of the solution, you are part of the problem.”

Summary:

· Q1 2022 was Stagflationary by varying degrees throughout the global economy.

· Global inflation may be in some part due to the oligopoly structure and predatory nature of global supply chain operators.

· G7 policymakers and central bankers would rather blame Russia and China exclusively than other supply chain oligopolists for Q1/2022 Stagflation.

· Macklem Doctrinaire Friend-Shoring is the G7 solution to Stagflation.

· Price Discovery Control is the G7 solution to the Oligopolists’ inflation threat to Macklem Doctrinaire Friend-Shoring.

If you are not part of the solution, you are part of the problem ….

The incoming economic data and earnings seasons confirm that the global economy Stagflated in Q1/2022.

The causes of this Stagflation are not all that G7 policymakers make them out to be.

The incoming dismal data had, priorly, been anticipated by various strategic signals from policymakers and central bankers. President Biden had called for a New World Order. Treasury Secretary Yellen had, then, underlined the President’s call with her own view that World Bank is not currently structured to deal with global crises. Villains and solutions have been identified at the recent IMF/World Bank Spring Meetings.

The cause of the dismal data, and the solution, can now be embellished, nudged, and resisted, respectively, going forward.

What Is an Oligopoly?

An oligopoly is a market structure with a small number of firms, none of which can keep the others from having significant influence. The concentration ratio measures the market share of the largest firms.

(Source: Investopedia)

Oligopoly was the real name of the elephant hiding in the earnings report and economic data named Stagflation in Q1/2022. The real name has largely gone unnoticed in all the hysteria about Ukraine and Inflation.

This author hopes that policymakers look into the murky business of global freight companies. These companies appear to have bucked the global economic slowdown, in Q1, based on their reporting of record earnings. Kuehne and Nagel is a classic example. The company recently reported that net earnings had improved by 162%. It also reported that shipping volumes had fallen 4%, in line with the global economic contraction.

With shipping volume down 4% and net earnings up 162%, it is fairly obvious that the big earnings driver has been price increases. Air freight volume, admittedly, was up, but on aggregate more can be shipped in volume terms by sea than by air. Air freight volume increase is, thus, a red herring.

The big question policymakers, regulators, and law enforcement agencies should be asking are whether a 162% net earnings increase, on a 4% shipping volume decline, does not suggest egregious, not to say, illegal price increases, and price-fixing within an oligopoly market structure. The question should be asked of the whole industry and not just this one company. Congressional hearings would be a good place to start.

Economists should also be asking whether the, by now infamous, supply-side constraints, which are allegedly driving global inflation, are not just sharp business practices by a handful of practitioners who control the supply chains. It is noteworthy that in China, where inflation has been controlled, oligopolists have had their franchises appropriated by the State.

Sadly, G7 policymakers do not wish to question the owners of existing supply chain companies about their business practices. Sadly, oligopoly is deemed to be synonymous with the free market in the G7 market places where the oligopolists prosper. Apologies and apologists rank scale economies, allegedly delivering lower consumer prices, higher than market pricing power in these market places.

Instead, of questioning, G7 policymakers wish to use the suffering wrought by these oligopolists as a catalyst for the restructuring of global supply chains and the global economic order. It is not clear who is who’s useful idiot, in this context. It is however clear that global consumers are everyone’s useful idiot in practice.

Thesis, Counter Thesis, Synthesis ….

· A multi-polar global economic order was born at G20 Indonesia 2022.

(Source: the Author)

Russia and China have been identified, by G7, as the villains and the main causes of current Stagflationary global economic conditions. Coincidentally, or much rather not, these two protagonists have also been presented as the main threats to the civilized democratic policy. Stagflation is, hence, conflated with dictatorship.

The villains are not taking this condemnation lying down. In response, they argue that they are the “New Model”, of an alternative New World Order, that will be adopted through the medium of G20.

· The FOMC’s barnstorming domestic economic landing has reached global “Friend-Shoring Junction”.

· Macklem Doctrine ticks all the “friend-shoring” boxes.

· US “friend-shoring” will be achieved with “Build Back Better” and “Make More In America” fiscal drivers.

(Source: the Author)

The G7 solution has been identified as the combination of global growth with the “Friend-Shoring” of global supply chains in countries that follow the code of free trade and the democratic governance regime that is synonymous with it.

In addition, “Friend-Shoring” includes personnel, in order, to denude those nations targeted of their most talented professionals and scientists. “Friend-Shoring” is hence destructive and constructive. Offense is, evidently, the best defense in this case.

· The World Bank endorses and proselytizes Macklem Doctrine, whilst the IMF multi-polarizes it.

(Source: the Author)

This author has dubbed the process of “Friend-Shoring” Macklem Doctrine. This doctrine was articulated by Bank of Canada Governor Tiff Macklem, as a supply-side investment-led initiative to promote disinflationary economic growth. Trillions of US Dollars, Euros, Yen, etc., etc. are going to be created in the pursuit of this agenda. Inflation will, thus, be a constant threat and central banks will, hence, be required to talk a good inflation-fighting game.

· Regime change by Cancel Culture could be on the G7 agenda.

· Disinflation price discovery by Cancel Culture is on the global commodity and capital markets agenda.

(Source: the Author)

This author notes that it may be cheaper and more effective to reinforce legal anti-monopoly rules into the governance regimes of said democracies. He also notes that this will require far less in terms of investment and, hence, deficit-financed credit creation. Clearly, this legal panacea is no Keynesian stimulus. Presumably, this is why it is a dog that is not hunting the oligopolists.

Neither does this anti-monopoly strategy have the desired objective of political restructuring that is conjoined to the economic objective. Presumably, this is also why it is a dog that doesn’t hunt globally. There is, however, a far more dangerous global predator. This beast is totally political in nature.

· The recently released Global Regime Change virus is highly contagious and wildly indiscriminate.

(Source: the Author)

If one is not part of the solution, one is part of the problem. To address this identifier problem, the Global Regime Change virus has also been released. This virus is, however, indiscriminate and will blowback, on some of the proponents of the global solution, especially in countries with a democratic election process.

· Whilst united, on Ukraine, at the global level, G7 nations and their central bankers are diverse at the national level.

(Source: the Author)

The recent experiences in the G7 democracies of Germany, the United States, and the United Kingdom illustrate the fickle natures of the economic solution and the indiscriminate regime-changing virus.

From Eurozone to Weimarzone, by way of Kyiv ….

Going into the World Bank/IMF Spring Meetings, renowned strategist, author, legend, and former US national security consultant Edward N Luttwak had been heard to ask “if the monetary authorities are up to their tasks”.

The G7 “monetary authorities” have a plan, and events in Ukraine could be said to neatly act as a catalyst for it. All that is required is some rhetoric to conflate current global threats, and their causes, on the surface of this catalyst.

Malpass’ sublimely inculcated form of economic warfare requires its own supply-side investing, and fiscal deficits of considerable magnitude. It also requires its casus belli which is understood by its taxpayers.

(Source: the Author)

Coming out of the Spring Meetings, there was a guarded response, to the question, from said “monetary authorities”. What initial disclosure there was, came off the record. Such arcane disclosure served to heighten the uncertainty even further.

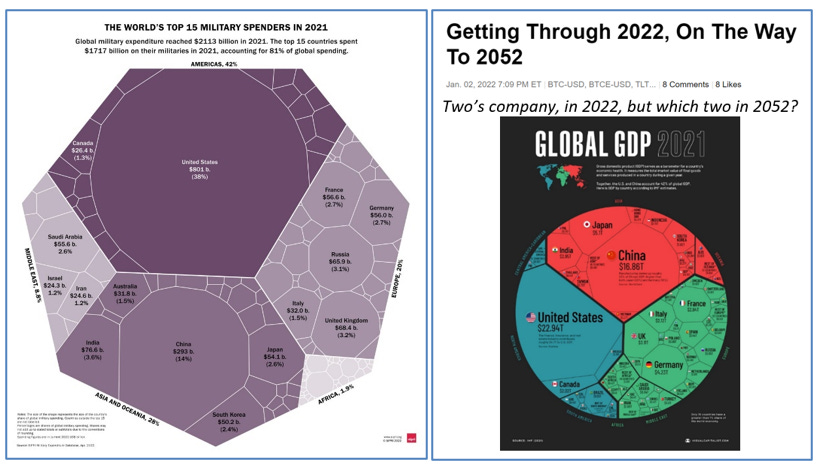

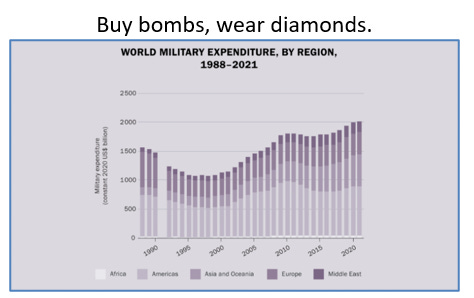

World Bank Group President David Malpass had mumbled euphemisms about the need for “security” to guarantee global economic growth. This only served to identify the elephant in the room aka military spending. The size of this elephant was recently estimated at $ 2 trillion by the SIPRI institute.

Military spending correlates strongly with the global credit cycle and central bank balance sheet growth. There must, therefore, by default, be some correlation with the global business cycle that needs spinning into a positive narrative by the folks doing the military spending and related borrowing.

Military spending, and associated fiscal debt, clearly, have a place in the global economy and on central bank balance sheets. This needs to be framed as an enabler of economic growth, that opens supply chains, rather than of conflict that closes them. Not surprisingly, there have been few takers of this rhetoric mission so far. President Biden and few good men and women in Europe are, however, waxing lyrical on the subject.

President Biden isn’t talking about the cost, to the US taxpayer, of the war in Ukraine. Instead, he is itemizing, in general terms, how the money will be spent. These itemized expenditures can be found in the latest report on the European Democratic Resilience Initiative (EDRI) that he launched on March 24th.

This initiative is now being enhanced to form a core principle of US foreign policy, in the wider European arena, beyond the Ukraine war. It is a policy initiative that POTUS hopes will transcend the partisan divide in order to gain momentum and endure for the long term.

Apparently, the EDRI budget will, initially, be spent on the following:

Advancing Accountability: To promote justice and accountability for atrocities committed by Russia’s forces in Ukraine,

Defending Journalists, Civic Activists and At-Risk Groups: The EDRI will enhance the safety, security, and operational effectiveness of journalists, and pro-democracy, human rights, and anti-corruption activists inside and outside of Ukraine.

The State Department and USAID are the executive functions where the EDRI is located. They are its custodians and executors. They have some medium-term objectives, which are the points at which the EDRI takes on a formal global policy role. These objectives are:

Bolstering Human Rights and Democracy in Europe,

Advancing Anti-Corruption Efforts,

Sustaining Civil Society and Independent Media.

Broadly speaking the EDRI’s spending closely follows the agenda discussed for the Macklem Doctrinaire supply chain “Friend- Shoring” at the recent World Bank/IMF meetings. Biden’s EDRI is, therefore, scalable and, no doubt, it will be scaled in due course.

The EDRI is, thus, a form of Constitutional amendment, in essence with hints of a Marshall Plan, in practice, about it. Interestingly, the EDRI supports individual European nations rather than the European Union (EU). How the EDRI co-exists alongside the EU is not clear. It is easy to see the two falling out, not only in Ukraine but, also, in Eastern Europe in general. The prospect of Eastern Europe falling under American, rather than EU, influence is most likely even less palatable to President Putin.

The EDRI, thus, signals a general escalation of the conflict in Ukraine, beyond its borders, into Eastern Europe and the Eurozone. Former National Security Adviser John Bolton has already noticed some gaps between the USA and its NATO allies. It is not clear if the EDRI is filling these gaps or creating them.

So, what of America’s NATO allies and their military spending? Many have been falling short of the NATO, 2% of GDP military spending, membership threshold. Faced with COVID debt, and Ukraine-driven recession, purse strings are tight. NATO membership is thus a fiscal problem for some of the members.

· The internally conflicted Eurozone will become a managed command economy for the duration of its structural transformation towards a Federal Republic.

(Source: the Author)

Germany has become the first G7 nation to, arcanely, fess up about its Ukrainian war debt. Unnamed sources have leaked that Finance Minister Christian Lindner intends to borrow an extra 40 billion Euros, to cover the impact of the war, thereby, expanding net new debt for the year to 140 billion Euros. Prior to this leak, the Bundesbank had stated that the German economy is likely to contract for much of this year. The net new debt is, therefore, currently, unsustainable. The rise in Bund yields, to reflect this unsustainability, is a monetary policy tightening in and of itself. This unique tightening comes at a time when yields are, also, rising because of the expected monetary policy tightening from the ECB.

With refreshing candor, Lindner also has highlighted the Stagflation risk from these conditions in Germany. How could he fail to do so, given Germany’s Twentieth Century economic history? To fail to speak out, would be to accept the tyranny of the past, and its sources. Burke believed that tyranny was enabled by the silence of good men. Sadly, inflation has currently been enabled by good intentions, as presumably, it was at the beginning of the Weimar Republic.

Since the Second World War, Germans have been reliable debtors. Post-COVID, and Post Ukraine War, assuming the latter ends, German reliability is challenged in the interim. Germany’s hydrocarbon energy paucity is also a threat to its reliability.

Germany’s struggles with fiscal fidelity may, however, turn out to be nothing in comparison to its even less reliable Eurozone partners. The German breach of Black Zero fiscal rectitude now serves as a precedent for said neighbors. What is good for the German goose is even better for the neighboring ganders. The Southern Europe flock of ganders never was any good at paying its debts, when each bird had its own currency. Devaluation, and a few extra zeros, here and there, on the latest fiat currency of the realm, was, traditionally, the way these ganders waddled out of the hands of their creditors. Now, the collective waddling starts at the Eurozone level since all have the same fiat currency to debase.

The German fiscal precedent, and the bending of EU Stability Pact rules, may, therefore, be an irreversible structural shift in the fiscal status of the Eurozone. The new fiscal paradigm is structurally deficit and inflation prone.

Germany’s former Axis ally Italy is more transparent about its fiscal situation but more disingenuous in its conclusion about it. Evidently, Italians don’t leak, instead, they lie. Bank of Italy Governor Ignazio Visco does not see a recession, ergo, he sees no Stagflation. Presumably, Italy’s smaller reliance, on Russian energy imports, has immunized the Italian economy from German contagion. Italian yield spreads would beg to disagree, however.

The inflation issue in the USA is a political issue.

If you don’t shoot the messenger, who do you shoot?

· The Fed is diverging from the White House and may even, officially, blame the Federal Government, for the current inflation spike, under oath.

(Source: the Author)

The last report observed the progression of the unwanted parcel, known as inflation, in the blame game, of pass the parcel, between the Federal Reserve and the Federal Government.

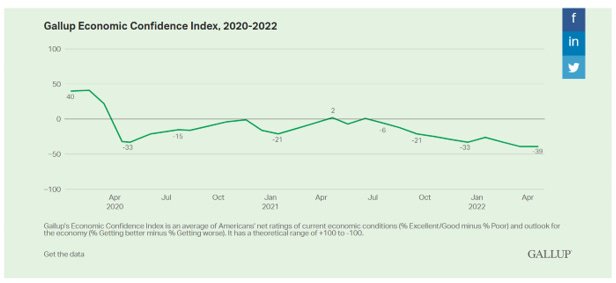

The latest Gallup Economic Confidence Index data puts this passing game into context. Inflation is the consumers’ greatest economic worry, which conflates with lack of government as the greatest non-economic worry. Fear of Russia is way down the list. Ostensibly, therefore, the Federal Government, not Russia, nor the Federal Reserve, is being blamed for inflation.

· On aggregate, the overextended US Consumer is most likely to be subsisting on inflation, rather than gorging on it, but the Fed is assuming the latter.

(Source: the Author)

The latest Gallup data also confirms that inflation is a consumer-impacting economic headwind. This confirmation may inform those debating the latest US GDP and CPI data.

The G7 “monetary authorities” have a plan, and events in Ukraine could be said to neatly act as a catalyst for it. All that is required is some rhetoric to conflate current global threats, and their causes, on the surface of this catalyst.

(Source: the Author)

The recent World Bank/IMF Spring Meetings’ impact on consumer confidence has not yet had a chance to influence the economic data. This author previously concluded that these meetings were the opportunity for Russia, and China, to be blamed for the US inflation problem, and for President Biden’s reciprocal strong support for Ukraine to be promoted. The next two Gallup confidence data readings will be an opportunity to see how successful the Spring Meetings have been in this endeavor.

In the meantime, policymakers and regulators are doing their best to create disinflation by fiat. They may have to redouble their efforts. The Q1 contraction in US GDP does not appear to have had a disinflationary impact. It, thus, seems more likely that the inflation has contributed to/caused the economic contraction. This discovery should make for some interesting finger-pointing, between the Federal Reserve and Federal Government. Aggressive monetary policy tightening, from the Fed, is bound to get second-guessed in the process.

This author hopes, but doubts, that the fingers will get pointed at oligopolist supply chain companies.

Who is to blame for the current Stagflation? The chances are that both protagonists will point their fingers at Russia.

Regulated disinflation: If you can’t make it, just fake it ….

· Disinflation price discovery by Cancel Culture is on the global commodity and capital markets agenda.

(Source: the Author)

The oligopolists will not however have it all their own way, going forward. A system of price discovery and price control is going to be enforced upon them.

A previous report discussed the turf grabbing underway, by which central banks will gain oversight and regulation of commodity markets. The cozy old world of “my word is my bond” self-regulation is over.

Coming out of the Spring Meetings, the demise of commodity market self-regulation is now openly discussed. It is not so much a matter of if as when. The speculative use of commodities, under the broad heading of asset allocation, is destined to follow on the list of canceled activities. In short, if you are not a commercial user you will not be allowed to be a commodity trader.

· Meaningless high spot commodity prices on screens are the reference point for meaningful discounts in the “constrained” physical markets.

(Source: the Author)

For Russian physical commodity traders, the future also looks bleak.

The prospect of embargoed Russian crude discounting its way to market is also being openly discussed. Central bank governance of this discounting process will, doubtless, have an innate disinflationary biased set of rules attached.

On the other side of the Atlantic, there is a cost-of-living crisis that is crying out for fiat disinflation. The UK Government’s laissez-faire principles make this outcome unlikely. These same principles, therefore, make regime change more likely.

A Rake’s Progress : (IX) The Jubilee Headwinds of Change

· The UK will become an austere economy with an ungovernable polity.

(Source: the Author)

Chronicling the key intelligence topic, of the demise of the UK economy, has become almost as painful, for this author, as watching ninety minutes of, what is purported to be, football as played by Manchester United. The headwinds of change are blowing through both tragedies.

The author’s predicted austerity has recently appeared in the form of a halved budget deficit. The predicted “ungovernable polity” is, partly, motivated by the cuts in government service provision and associated redundancies. Part of the militancy is motivated by the current cost of living crisis, which has been framed, by one former Bank of England Governor, as 80% driven by Brexit. The rest of the ungovernability is directed at the observable observed sleaze in the government. The Jubilee may be marked by anarchy and political change.

Rebellion has been provoked by the appearance of bloodstains, on the Government’s hands, from the 20,000 martyred Britons, in care homes, who the High Court has recently ruled that the Government failed to protect from COVID-19. The Government’s response is, once again, tone-deaf. Fiscal austerity has been unleashed, which puts the survivors at even greater risk by depleting the health care sector even further.

The government is anticipating the rebellion by moving the legal goalposts to intercept the rebels. Just as parliament was proroguing, in order to undergo local elections, that would serve as a proxy referendum on the government, anti-civil liberties legislation was forced through the Upper Chamber. The passing of said anti-civil liberties legislation will make it more difficult for the population to make their discontent known, in the public arena, and also to openly question decisions made by public bodies.

Perhaps, more alarmingly, the legislation gives the government greater oversight, and control, of the electoral process. Peaceful protest, in public, and via the democratic voting process, is now being eroded. President Trump would admire the UK government’s style. President Putin will, probably, try to copy it. UK democracy and the Union is now hanging by a thread.

Austerity is, clearly, evident in the latest UK insolvency statistics. Company and individual insolvencies are accelerating. The economic threat to the Union is clear, as companies and individuals go under in Northern Ireland and Scotland. Regional populists will claim that they have been abandoned by London. Nicola Sturgeon will be gleefully watching the carnage, whilst Sinn Fein will be preparing the economic case for a Republic. The PM’s recent jaunt to India and the announcement that potential new UK IT jobs will be diverted, from the provinces to the Subcontinent, is just another nail in the coffin.

Bridgerton Revisited: “Now in Injia’s sunny clime, Where I used to spend my time ….”

(Source: the Author)

The last report discussed the headwinds of change blowing, from the Commonwealth, on Westerly and Easterly trade winds. The latest headwind, incoming from indigenous Canadians, is chilling. It’s all hands on deck.

The UK Prime Minister has a trademark, nostalgic zeal to live, vicariously, in a time when the global map of commerce was mainly pink. This is his fighting brand. His, oftentimes, ruthless pursuit of this political agenda has made him a potentially useful idiot in the hands of some wily oriental gentlemen and ladies.

These wily orientals are “they” from over the sea, who reside in the RIC parts of the acronymous BRIC alternative world order.

“They” are culturally, and politically, antipathetic towards the Occident, G7, and its own New World Order. “They”, hence, have a vested interest in undermining the institutions of the Occident which, currently, govern global politics and commerce. “They” have, therefore, pulled the strings, of their oftentimes nostalgic potential useful idiot, in such a way that his comedic self-disporting, on the ascent of the Greasy Pole, has undermined its base, in the UK, and thereby its support for the broader Occidental hegemony.

Unelected custodians, of the UK ship of state, have looked on, aghast, as the potential Useful Idiot has blown holes in the deck and tossed his crew overboard. The last report discussed how a reconnaissance mission, by two senior Royals, had brought back dispatches full of intel on the campaign, by the wily Chinese gentlemen, to undermine British influence in the Caribbean. A second mission has just been undertaken, and the findings are as dismal. It appears highly likely that, somewhere, behind the scenes, some wily oriental gentlemen wish to mark the Jubilee with a crisis, in the Commonwealth, that shakes the realm.

The first official Crown intervention has been observed, by this author, in the BVI, where the Premier has just been busted for drug running. The Commonwealth narcotics supply chain, by tradition, is strictly regulated and governed, by the intelligence and military services; formerly located in the Helmand Province of Afghanistan, until it was devolved back to the Taliban. Evidently, some of the supply chain is being regulated and governed in the Caribbean.

Coincidentally, the PM appears to be increasingly intoxicated with his vicarious endeavors. This intoxication was, recently, highlighted by his well-publicized Indian bad trip, which yielded nothing but bad press, at home and, on the ground. A closer inspection of Indian macroeconomic fundamentals shows that the majority of potential employees there have given up looking for work. The tight Indian labor market is, hence, a signal of economic decline rather than of booming wage inflation. How and why Britain is harnessing itself to this kind of economy is a mystery that only the Chancellor and the Home Secretary fully understand.

It may now be time for a mutiny, on the ship of state, and perhaps even for the potential Useful Idiot to walk the plank, before he vicariously orders another disastrous Charge of the Light Brigade in the Crimea.

As one Greasy Pole totters another one is being erected, along with its own Rake’s Progress storyboard, in the political middle ground.

Polled sentiment signals that the British voters despise Boris Johnson, and don’t trust Sir Kier Starmer. Based on this polling, the middle ground is the place to be. A new middle-of-the-road, yet essentially British Greasy Pole, to erode the extreme Greasy Poles to the left and right, is currently in its project phase. Project execution will require a new party. No wonder the PM wishes to call an early election. The longer he waits, the more likely that the new party will be born.

Practically speaking, it may not matter, when an election is called, since the project is based on a tripartite coalition that will frustrate the traditional whipped-up line of the Commons voting process. The Party Whips will get whipped, by the tripartite coalition of the proto-party. Time and defections will then follow to make the new party real.

The political genotype of this new centrist proto-party, allegedly, has a few chromosomes, to go with the revolutionary oratory, of Tony Blair in its helix. These new parties usually begin well, and then degenerate, as their leaders climb the seductively Greasier Pole, of global politics, which is sexier than the parochial original. The new globalist euphemism of “Friend-Shoring” is also, then, usually, achieved with calumnies, dodgy dossiers, and foreign military adventures contrived by said globally-seduced leaders.

Mayday, Mayday! Let the pole dance-off begin.

Maybe President Biden’s scaled-up EDRI can be Anglicised and rolled out, on the streets of the UK, before the pole dance-off degenerates into a civil war.