The Unholy Trinity of Hyperbolic Inflation, Oligopoly and Hyperbole: A Bretton Woods Moment

The Unholy Trinity of Hyperbolic Inflation, Oligopoly and Hyperbole: A Bretton Woods Moment

“This might well be our Bretton Woods moment. Let’s not waste it.” (Angela Ellard)

Summary:

· Current inflation-fighting mission creep, from procrastination to hyperbole, raises the threat to credibility.

· Mission creep, from Lend Lease to Friend Shore, may drive the next US fiscal stimulus.

· Financial stability policy consideration moves the delta of the “Bostic Put” to in the money even whilst Inflation Mandate policy moves its delta the other way.

· G20 beggar-thy-neighbor Friend Shores disinflation via the oil price.

· The traditional Fed Put can be seen by reading between the lines, of the Fed’s recent Financial Stability report, using Lael Brainard’s lenses.

· Loretta Mester hints that the Fed’s hyperbolic recalibarting will be conditional on the unrealized losses, on the Fed’s balance sheet, in addition to the incoming economic data.

· The UK is aggressively 1980s rebooting, Submerging Markets style, whilst its European trade partners reboot in a more peaceful fashion, and America tries to reboot 1990s style.

· The Ukraine War is also becoming a war for full EU national integration.

Hyperbolic Inflation, plus Procrastination, begets Hyperbole.

The hyperbolic rise of inflation has become more significant than the collective procrastination of what to do about it. Hyperbolic inflation, has, thereby, caused the procrastination to become hyperbole. Central banks, and elected policymakers, have adopted hyperbole, in communication, to avoid larger incremental anti-inflation policy action upfront. The hyperbole, literally, frames the global economy at a contemporary Bretton Woods moment. Hyperbole threatens radical action, which elevates the hyperbolic risk of recession.

History has, so far, been kind to those who have written it, so the Hyperbolists have precedent on their side. They just need some time, and space, for the incoming economic data to fall within their hyperbolic frames of reference. For now, guidance hyperbole is a halo that has yet to enclose all of the incoming data. Halos are ephemeral. Frames are more durable, but they require real action, in the form of tighter monetary policy, on this occasion.

Hyperbole, without action, erodes credibility, even more than procrastination, without action, does. Central bankers and policymakers have, thus, raised the stakes, for themselves, by becoming hyperbolic. During the requisite time and space, therefore, the Hyperbolists must build the frame, for their ephemeral halo, with a credible modicum of inflation-fighting actions.

The Globoligopoly that shall not speak its name ….

In the last two reports, the author has outlined how the innate Oligopolies, constricting the beating heart of global supply chains, have exploited the combined monetary and fiscal stimulus response to COVID-19. This exploitation has been in the service of Oligopoly shareholder value in lieu of lost revenues at the onset of the pandemic. The cost to the customers, and the global economy, has been an inflation spike. Customers didn’t consume more, in aggregate volume terms, they just paid more, for the privilege of consuming the same, thanks to consumer financing from their governments and central banks.

“The optimization of global value chains led to the production of many critical inputs becoming highly concentrated in certain geographical areas.” (Author’s emphasis)

(Source: ECB)

ECB Executive Board member Isabel Schnabel recently used the “O-Word” in relation to global inflation. She did not say Oligopoly, however, instead, she euphemistically said optimization in relation to the practice.

Having avoided the smoking gun, Schnabel then called time on the Oligopolists. Sadly, this means that the ECB will also be calling time on economic growth with tighter monetary policy. This coincides with the Fed calling time on the Oligopolists and economic growth via the same modus operandi.

Because of its location, in the heart of North American oil and gas production, the Dallas Fed has to mind its P’s and Q’s when talking about the oil industry and pricing tactics. The Dallas Fed is even more careful not to say the “O-Word”, therefore. Instead, the Dallas Fed uses the “F-Word”. F is for friction.

The Dallas Fed has written, what amounts to be, a get out of Federal jail card for the anti-competitive behavior of the upstream exploration and production sector of the petroleum supply chain. Allegedly, this Oligopoly “situation reflects frictions in the retail gasoline market rather than the supply of oil or the price of oil.” Furthermore, there is apparently no point in the global upstream sector producing more crude oil, because “even under the most favorable circumstances, higher production growth is unlikely to materially lower global oil prices—and, thus, U.S. retail gasoline prices—in the foreseeable future.”

So, basically, unless the downstream petroleum supply chain is not unblocked even higher oil production won’t drive gasoline prices lower. America, therefore, has a supply-side problem in the downstream petroleum sector. The Dallas Fed having identified the problem, does not go further and name it with the “O-Word”. As far as the Dallas Fed is concerned, there is no price-gouging occurring, although the commentators are careful not to quantify what gouging is in price terms. A trucker or a hockey mom might have a different metric for gouging, however, so it is all relative. The perspective that matters is the consumers’, however, and this is feeling decidedly gouged. All the Dallas Fed can do is say that this alleged gouging is accepted legal business practice.

Ostensibly, the Oligopolists have a lot of sunken capital, give it a name “Skin in the Game”, and income manifested in the existing global economic order and its supply chains. This makes them inert. This inertia may inform, but does not excuse their rapaciousness. They are therefore an obstacle to the G7 plan.

(Source: the Author)

This author would reiterate, the point made in the previous report, that there is no incentive for the downstream operators to unblock their part of the supply chain, because it would eat into their margins. There is, hence, no need to gouge, because the scale returns to the Oligopoly, in this sector, delivers acceptable shareholder returns. Inflation is, thereby, baked-in through conventional business practice. One consumer’s baking-in may be another’s gouging.

· Disinflation price discovery by Cancel Culture is on the global commodity and capital markets agenda.

(Source: the Author)

This author also notes that the Democrats couldn’t give two hoots about what the Dallas Fed says about price gouging. Inflation is eroding political capital, and the prospect of re-election, swiftly. The Democrats are using the “E-Word”, therefore, instead of the “O-Word”. The E is for excessive in relation to fuel prices. Consequently, the Democrats wish to pass a bill that gives the President the authority to decide what is excessive and thereby illegal. This author is reminded of the application of “Cancel Culture”, in relation to legislated disinflation, of which he has written previously.

With little in the way of help, currently, from executive policymakers and lawyers, the central banks have to deal with the supply-side structural inflation issue using the inappropriate tool of tight monetary policy. Collateral economic damage, on the demand side, then lowers inflation and the Oligopolists live to fight another day when monetary policy conditions become a tailwind.

Fortunately, there is a G7 mitigation strategy in place that may soften the blow from the tightening of monetary policy. This mitigation strategy may, also, divert the economic slowdown towards China, and its supply-chain satellites, through the process that this author calls “Friend-Shoring”.

Applied Macklem Doctrine: Crank Up the “Friend-Shoring” via Lend-Lease ….

Vladimir Putin’s house needs painting too Tiff, capisce?

(Source: the Author)

The last report discussed the state of the combined Federal nudge to align the Fed’s balance sheet with the fiscal imperative, to stimulate the economy, and the global imperative to “Friend-Shore” global supply chains away from named nemeses. Lockheed Martin’s CEO has just picked up the baton, or javelin, depending on how one perceives it.

If an external, and existential, threat, which drives the supply-side initiative, can be found, then, the process of aligning fiscal deficit with the Fed balance sheet can be made easier. An existential threat, which constrains supply chains, thereby increasing inflation, is even better.

(Source: the Author)

Facing the Nation, Lockheed Martin CEO Jim Taiclet said that his company, and thus the USA, by default, needs to “ramp up” production in support of Ukraine. This can only be achieved by reforming and ramping up supply chains, in his view.

The US Commander In Chief has responded to Mr. Taiclet’s bugle, with alacrity by signing the Lend-Lease program for Ukraine. Mission creep, inevitably, will see the program’s parameters expanded to anything that can be tagged with a national security label. This label basically fits the whole economic supply chain from food to technology. Woe betides any Federal Reserve official who gets in the way.

· The Macklem Doctrine of America’s global imperative may make bigger fools out of the FOMC than the incoming inflation data.

(Source: the Author)

Congress should, henceforth, also, respond with alacrity by, doing what Janet Yellen has preached, and Bank Canada Governor Tiff Macklem has embraced, through “investing” in supply chains. In the short term, this process is inflationary. There are signs, however, that the short-term inflationary picture is improving.

If only the Fed and the Federal Government could find someone else to blame for the global supply chain woes and inflation. If blaming this someone also required disinflationary, deficit-financed, supply-side investment then both could stop blaming each other, and get on with the financing.

Which brings both to the war in Ukraine.

(Source: the Author)

Congress has, initially, responded, with bipartisan alacrity, by passing a much larger Ukraine emergency spending bill than the President had originally envisaged. It is not so much a case of the President finding the bipartisan sweet spot. It is more the case of Congressmen, from either side of the aisle, falling over themselves to be seen as patriots. This patriotic disporting buys political capital and stimulates the economy.

In the last report, the author suggested that “Shootin’ Putin”, rhetorically speaking, of course, could be just the ticket to kickstart a combined monetary and fiscal policy stimulus. All that appears to stand in the way now is inflation. A careful spinning, of the supply-side disinflationary component of this combined stimulus, should be easier to sell, to a skeptical Mr. Market, through the associated patriotic halo effect.

The global narrative spinning is, already, at an advanced stage at the WTO level. Deputy Director-General Angela Ellard has literally framed the situation, in relation to Ukraine, as a “Bretton Woods moment”. Hyperbole indeed.

Such gravitas and import go way beyond the immediate Ukraine war and the ensuing reconstruction process. Ellard’s words invoke the New World Order of the global economic reset previously invoked by President Biden. The global financial system is, therefore, just about to have a reset, just as a new financial crisis threatens. What a coincidence!

G20 Beggar Thy Neighbor “Friend-Shores” Disinflation by way of the Oil Price ….

The last report discussed the race to the bottom, in which non-G7, loosely aligned, countries undercut each other as the process of “Friend-Shoring” supply chains, out of China, turns disinflationary.

· G20 Beggar Thy Neighbor Friend-Shores G7, and itself.

(Source: the Author)

India has been a key “beggar” in this process, brazenly, demanding significant discounts for Russian hydrocarbons. Combined with the COVID-Zero slowdown in China, the hydrocarbon bid discounting has recently knocked on to Aramco’s pricing policy.

· Oligopolists are currently defeating Capitalism, possibly for the last time.

(Source: the Author)

Aramco is already facing a big hurdle from the accelerated progress of the “NOPEC Bill” in Congress. A confluence of factors has, thus, prompted Aramco to offer 5$ discounts per barrel to Asian customers. The discounting force is by far greater than the recent increasing force from OPEC’s commitment to keeping supplies tight. Hence, less supply is now being offered at a lower price. The price/volume dissonance continued, as global oil prices continued to slide. Perhaps in an attempt to arrest the slide, and/or to explain why the country has not been able to fully respond to President Biden’s calls for more supply, the Saudi Oil Minister explained that Aramco is facing supply capacity constraints. The speech may also have been informed by President Putin’s executive order for his team to find payment solutions for “unfriendly” nations.

Those riveted to spiking oil and commodity futures prices, on their screens, should remember that the complete opposite occurs in the real world in times of crisis.

(Source: the Author)

Thus, global disinflation from recession, in Asia, and via emerging markets, is coming just at a time when the pundits, and the central bankers who listen to them, are beating the drum about commodity-driven inflation.

The drum beating the assonant sotto voce monetary policy easing mantra, that has recently been playing in the background is, however, getting louder.

It’s the “Powell Put”, but not as we know it….

The last report discussed the, poorly executed, delivery of the “Powell Put”, by its namesake. Chairman Powell has further undermined the poor execution, with recent guidance which implies that a recession is now unavoidable as the FOMC hardens its anti-inflation stance.

The “Powell Put” was understood, by this author, as a commitment, from the Fed, to take a nuanced approach to perceived labor market tightness. This nuance would inform the context of incoming labor market data. The output would, supposedly, then be a monetary policy tightening less likely to trigger a recession.

The Kansas City Fed’s recent labor market nuances, in a labor market bulletin, support the thesis. The report finds two major demographic factors significantly driving the labor market tightness. These drivers are low fecundity and advanced geriatrics. Monetary Policy has no direct impact on these two factors. Neither does it impact immigration, which has also tailed off, thereby, choking labor supply. If demographics explain the missing 2 million US workers then tight, or loose, monetary policy will not, immediately, bring them back. Supply-side reform may stand a better chance if the partisan political demagogues can be kept out of the process.

The “Bostic Put”, nearly in the money ….

· The “Bostic Put” joins the “Waller Put” on the list of “Fed Puts” being extensively forward-procrastinated.

(Source: the Author)

The “Bostic Put” was identified, some time ago, by this author, as a commitment not to trigger a recession with monetary policy tightening.

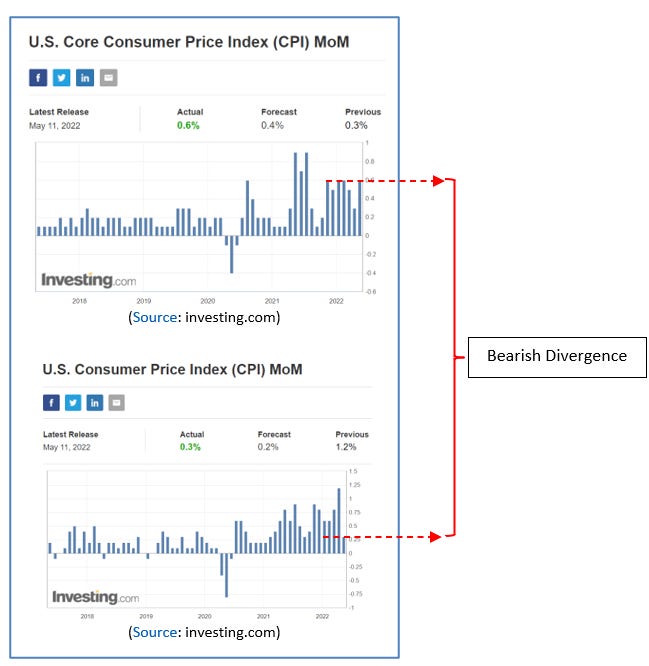

The author has also suggested that the “Bostic Put” was based, in part, on the observation, of the Atlanta Fed’s Sticky CPI data, which showed Sticky inflation-driven non-discretionary Core spending cannibalizing discretionary Flexible spending.

The latest CPI data confirm this observation. Core CPI rose month-on-month, whilst CPI fell.

The Put option writer, Atlanta Fed president Raphael Bostic, recently, gave a ballpark evaluation of how far in, or out of, the money it currently is. It is, apparently, nearly at the money. Bostic stated that a 75-basis points rate hike is not in his ballpark. He also sees the need for two or three more 50 basis point hikes. At the same time, he notes an accelerating confluence of global events which, in conjunction with the inflation cannibalized consumer spending, are bringing the option Delta towards 0.5.

Bostic was doing quite well, with his recent guidance, until he tried his hand at financial stability policy by way of reading the market. According to him, the fact that the Fed has only moved 25-basis points, up in rate hikes, whilst the bond market has moved up circa 200-basis points, speaks highly of the Fed’s credibility. This author believes that this volatility speaks more highly about the Fed’s lack of credibility and its late arrival at the party where there is a distinct lack of financial liquidity.

Financial stability policy may change the structurally intrinsic value of the “Bostic Put”, from a commitment not to create a recession, to a commitment to ease because of financial instability issues, well before inflation has fallen significantly closer to the Fed’s target.

Hyperbolic financial instability is, hence, becoming more significant than hyperbolic inflation. In fact, hyperbolic inflation, combined with the FOMC’s reaction to it is negatively feeding back, into hyperbolic financial instability, with a growing impedance that triggers financial crisis and then recession. At this juncture, all the various procrastinated Fed Puts are well into the money and have been struck.

Hyperbolic Inflation begets Hyperbole ….

FOMC speaker procrastination may be evolving, into hyperbole, but the song remains the same for now.

Cleveland Fed president Loretta Mester’s guidance has maxed out, in terms of the adjectives used to describe monetary policy in lieu of real action. In transition, Mester now conflates hyperbole with gravitas. The result, of this conflation, is the classification of the Fed’s attempts to move, from being behind the curve, as the “The Great Recalibration of US Monetary Policy”. The only thing great about it, that this author can see, is the scale of the gap in the Fed’s reactions to the consequences of outcomes that it has had a hand in creating.

Despite the hyperbole, however, Mester’s “Great Recalibration” remains the same 50-basis points rate hikes, in the next two FOMC meetings, as previously advertised, with the commitment to be more aggressive if inflation remains stubbornly high. It is, in effect, a great continuation of guidance, appended with the hope of the great gamble, that enough economic momentum is lost, over the next two months, to send inflation lower.

The dismal science is indeed so, but Mester has spiced it up a little with some colorful rhetoric and a wager.

Fool me twice, call me a “Neel” ….

· Neel “Ex Culpa” Kashkari has lost his credibility.

(Source: the Author)

The dismal science continues to be even more so for Minnesota Fed president Neel Kashkari. The spectacle is made worse by the appearance that the subject is, perversely, delighting in being right about the need to inflict a recession in order to beat inflation. Kashkari’s torrid time may continue as he now looks for reasons, to aggressively tighten monetary policy, to the exclusion of the contrary. In a recent episode, of ritual credible commitment burning, Kashkari clung to the belief that the US consumers’ healthy balance sheet will extend a consumption-driven inflation spike. How much tightening the FOMC needs to do will, he believes, will, hence, by default, depend on how quickly the supply-side of the economy eases up.

Kashkari appears to have simply picked out all the data from the latest New York Fed Quarterly Report on Household Debt and Credit which supports his decision to tighten monetary policy aggressively. A Fed president with a hammer only sees nails. Kashkari certainly does not feel clearly evident headwinds from the housing sector in the report.

Nowhere in his latest analysis did Kashkari consider that the consumers are rebuilding their balance sheets, thereby, building a cushion for the expected recession which he intends to inflict on them. This cushion may also be used to support the consumption of inflated goods. Also missing, from his analysis, was the consideration that inflation is driving increased savings behavior, and deleveraging, rather than consumption.

Kashkari may have noted that the deleveraging is the strongest amongst those with higher credit scores. Those with reasonable financial health are, thus, weathering the inflation storm and will weather the recession that he intends to inflict. Those with poor financial health, whom he once championed, back in his broadly inclusive period, are not weathering the inflation storm and stand no chance in the recession he intends to inflict on them.

If Kashkari really understood how a capitalist economy works, he would also know that it is those with the highest credit scores who drive the aggregate demand and pay most of the taxes. This cohort also creates jobs, either as business owners or through their demand and tax paying. The fact that this cohort has been hunkering down, since Q1/2021, does not say much about the prospects for economic growth ahead. It does, however, say something about the need for the glimpse, of a growth driver, on the visible horizon, to give this cohort the animal spirits required to do the future heavy lifting. Currently, he is shaving off their bullish horns and putting them into bear-like hibernation. Inflation was already doing this, so Kashkari’s cosmetic surgery is surplus to requirements at best. At worst it is permanently disfiguring and dangerously counter-productive.

This author notes the propensity of Kashkari to hold onto a belief, until the bitter end, and then totally go 180 degrees the other way with the same blinkered conviction. When the facts change, he, eventually, changes his mind; but, by then, it is too late in practice.

There is, however, some hope for Les Mis whom Kashkari has abandoned. It has been a long time in the making, but finally, the traditional “Fed Put” is on the table, even if only for financial stability reasons.

Name that Tune? The Traditional Fed Put ….

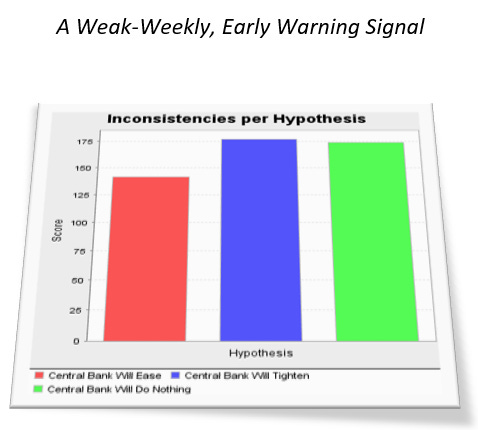

The Key Signals proprietary indicator, recently, gave an early warning that central banks who are tightening should beware. The latest move by Aramco amplifies this signal.

· The recent Wall Street earnings season-wink signals that the US financial sector has, already, become the medium of economic transfer of the FOMC’s “methodical” and “expeditious” tightening which has only just begun.

(Source: the Author)

Wall Street has already told the Fed that tightening financial liquidity conditions are blowing a real economic headwind. The Fed has chosen the timing of the release of its Financial Stability Report to acknowledge the signal. Fed Governor Lael Brainard précised the report. Her words neatly frame the FOMC’s approach to tightening monetary policy.

The good news on financial stability is that businesses and consumers have deleveraged. The US economy should, therefore, be capable of withstanding an aggressive monetary policy tightening to address high inflation. This takeaway was, however, diluted by Brainard’s framing perceptions of the inflation driver, namely commodities.

Brainard chose to frame the potential inflation threat, to the US economy, from the perspective of a negative growth shock resulting from the Ukraine war. She then chose to emphasize the declining liquidity, driven by the combined growth shock and tighter monetary policy as twin amplifiers of financial stability risk. This rising financial stability risk, in turn, feeds back into growth risk and declining liquidity. This author’s takeaway was that Brainard would like her audience to believe that rising financial stability risk is an economic headwind that the Fed is studying, without a conclusion, as yet. Whist the central bank studies, however, the economic headwind gets stronger. One may, thus, conclude that rising financial stability risk is placing limits on how far the FOMC is prepared to tighten monetary policy.

With supply-side stimulus bonds to go, in the near future, Treasury Secretary Yellen embellished the financial stability report frame with brio. Yellen highlighted the rising global uncertainty, primarily driven by the war in Ukraine. Hence policy, in response to said uncertainty, flows directly from the war driver.

The traditional “Fed Put” can, thus, be seen by reading between the lines of the financial stability report using Brainard’s lenses. It is no coincidence that whilst the report was being delivered, and digested, commodities, in particular Oil, were nosediving. In turn, Mr. Market chose to discount this, commodity price action, as an economic headwind that the Fed will make worse by tightening monetary policy.

Brainard’s financial stability study period allusion has given the Fed and the FOMC subjective time, and space, to decide just how aggressive monetary policy tightening should be.

There are, however, some FOMC members who do not want Mr. Market to rush off with the idea that a monetary policy easing is possible any time soon.

New York Fed President John Williams is looking forward to inflation, circa 4% by the end of this year, which is finally tamed by 2023, and back at target in 2024. Weak economic growth is a necessary cost of this cleansing process, according to him. Evidently, Williams is willing to gamble with tightening financial stability for a while longer.

The “Waller Put” how can I explain it …. There’s no room for relationship, There’s just room to hit it ….

· The “Waller Put” signals that the FOMC will not kill the “Build Back Better” and “Make More In America” booms.

(Source: the Author)

The author has previously discussed the “Waller Put”, attributed to Fed Governor Christopher Waller. This Put option is a promise not to tighten too aggressively rather than to ease as soon as the economy weakens. With this formulation, the probability of a disinflationary soft landing becomes elevated. The probability of financial instability is also elevated.

Governor Waller recently repeated this formulation with the added mantra that, since this is not the Volker Era, the Fed can “hit it (the US Economy)” with 50-basis point rate hikes, without having to kill it with 75-basis point rates hikes.

Some of Waller’s colleagues remain unconvinced.

Never say never ….

· The Fed is diverging from the White House and may even, officially, blame the Federal Government, for the current inflation spike, under oath.

(Source: the Author)

San Francisco Fed president Mary Daly loyally continues to toe Chairman Powell’s line, thereby, ruling out the need for a 75-basis points rate hike at this point in time. She has penciled in at least two more 50-basis points hikes by way of mitigating the need for 75.

The hyperbolic Cleveland Fed president Loretta Mester has, also, tried to support Chairman Powell whilst being careful to ensure that the price of this support is not another inflation increase. Consequently, she qualifies the Chairman’s ruling out, of current consideration, of 75-basis point rate hikes, with the caveat that this is not immutable.

It is not, however, the support for Chairman Powell, her hyperbole, or even the ruling in of a 75-basis points rate hike that is interesting about Mester’s recent guidance. What is most interesting, is her view of the Fed’s hyperbolic balance sheet.

The “Fed Put”: A Hyperbolic act of self-preservation ….

· The Fed may embrace Macklem Doctrine when it sees the unrealized losses on its balance sheet from the recent spike in yields.

(Source: the Author)

Loretta Mester is the first FOMC speaker to address the delicate subject of the potential, realization of unrealized losses on the Fed’s balance sheet. Said losses may, potentially, be realized by the sale of mortgage-backed securities at current prices. This author believes that there is little appetite for such realized losses, as they will require an implicit recapitalization of the Fed, by the US taxpayer, if they continue to get realized. Clearly, the losses are directly correlated with the inflation spike, which informs and energizes the current blame game about who caused it. Clearly, also, the losses erode the credibility of the realizer.

This author suggests that a compromise solution will, inevitably, be found which will try to hide the Fed’s losses behind the shape of the yield curve. Bonds falling due, for outright sale, will be rolled into longer duration bonds at a lower yield cost to the government. Bonds maturing at par will be allowed to do so.

The size of the Fed’s balance sheet will, thus, be driven by the imperative to avoid realized losses. This evasion implies that the Fed’s balance sheet will, therefore, have to remain elevated, thereby, extending the associated monetary policy easing period. Whilst this expanded balance sheet may soften the economic landing, it may also support inflation.

The best, that the FOMC can do, is to follow a steady course of monetary policy tightening which brings the bid back in, for the long end of the yield curve, which is then interpreted as a confidence vote for the central bank’s inflation-fighting credibility. An attendant softening economy will also fulfill this self-fulfilling prophecy. Such a self-fulfilling prophecy will be sold as the famous “Soft Landing”.

After the latest CPI shocker, President Biden has pointed the finger of blame at the Fed. The blame game between the Federal Reserve and the Federal Government, about who caused the inflation spike is, also, entering an insidious phase of the study, and commentary, presumably, in line with Brainard’s new game of understanding who is responsible for rising financial instability. Clearly, hiking interest rates is adding to this instability, and commensurate losses, realized and otherwise, for the Fed.

Do you want chips with your blame?

Though this example suggests that supply chain disruptions might have helped fuel inflation, Leibovici and Dunn noted there were also other likely factors, such as the unprecedented U.S. fiscal policy response to the pandemic. They concluded that a more rigorous analysis of recent inflation would be needed to account for these factors.

(Source: St. Louis Fed)

James Bullard’s St Louis Fed staffers are shaping up to empirically point the finger, of inflation blame, at the Federal Government. A recent study dissembled that it is highly likely that the fiscal response to the COVID-19 pandemic is where the smoking inflation gun is located.

St Louis Fed president James Bullard was on hand to deal with the blowback from the accusation.

The data says hot, but Jim says not ….

Empathy with the Rate Hike Devil ….

· James Bullard no longer has credibility.

(Source: the Author)

James Bullard is determined not to get blamed for a recession, which may follow the Fed’s interest rate hiking. Consequently, in the face of another high print, in the incoming inflation data, he stated that this still does not require a 75-basis points rate hike, just yet.

To be fair to Bullard, his latest call is consistent with his previous one in which he argued that the Fed is not behind the curve. Had he suddenly called for a 75-basis points rate hike he could appear inconsistent.

If the finger-pointing policymakers, and central bankers, can successfully teleport their audience’s perceptions, of the current economic situation, back to their chosen datum, then, they may no longer need to blame each other. Bullard has been doing his own bit of framing and teleporting, recently.

Why we care about the 1990s ….

· The 1990s global economic scenario is hiding in plain sight.

(Source: the Author)

This author has, often, fondly imagined that he can see the 1990s model, of how the Fed will operate, hiding in plain sight.

Only a 1990s Greenspan repeat will rebuild the Fed’s credibility.

Only repeat 1990s-style data will deliver a 1990s Greenspan repeat.

(Source: the Author)

The author has also had to qualify his fond imagining with the admission that 1990s-like incoming economic data will be required to complete the model. Notwithstanding the data caveats, there are still tangible 1990s signals being thrown off by FOMC members.

Richmond Fed president Thomas Barkin is the latest Fed speaker to eulogize the halcyon days, specifically of the mid-1990s, when inflation finally began to behave itself.

· Bullard’s Greenspan panegyric and Nabiullina’s lament are confirmations of the policymakers’ 1990s model hiding in plain sight.

(Source: the Author)

Where James Bullard has praised Alan Greenspan, in his own 1990s eulogy, Barkin has elected to reserve the praise for himself (and his FOMC colleagues) for, ultimately, getting the US economy back on a similar footing.

Famous last words: “If you can keep your head, and say Holy Cow, when all of those around you are losing theirs, and shouting Katie bar the door, you should be the Fed Chairman my son!”

(Source: the Author)

Barkin’s eulogy also contained a promise, from him, to do whatever it takes, in terms of monetary policy tightening, to get back to this 1990s-like datum. Barkin also alleges that, since he is a child of the Volker Era, somehow, this gives him the credibility, and right stuff, to guarantee that it will not happen again on his watch. The only thing missing from his speech was a pledge of Scout’s Honour.

Where the US economy may have the apparent luxury of time, and space, to return to the mid-1990s, the UK economy does not. There is however a political paradigm shift, in the making, that may transport it there. This paradigm shift quite literally has a preserved strand of Tony Blair’s Cool Britannia 1990s mojo woven into its fabric. How better to celebrate the Jubilee?

It’s One Hyperbolic (Groovy) Nation Disraeli Baby, but not as we know it ….

· The UK will become an austere economy with an ungovernable polity.

(Source: the Author)

The Queen’s contracting of COVID-19, just as Boris Johnson planned to announce the end of pandemic restrictions was a metaphor for the Rake’s Progress key signals, on the UK economy, being followed by this author. The Rake in question has progressed as far as accusations of interference with the freedom of the press, by selectively peddling his own propaganda, through friendly news outlets, in return for generous pandemic emergency support. Some further levity has been introduced through the blame of IT infrastructure for the UK Government’s lack of a response to the suffering of those most exposed to the cost of living crisis. Netflix could not make this stuff up.

A previous report discussed the prospect of a United Irish Republic, in the context of the decline and fall of the post-Brexit Union. This prospect is now an elevated probability after the success of the Sinn Fein party in recent elections. This success is symptomatic of the predicted ungovernability of the United Kingdom in these current times of fiscal austerity, tight monetary policy, and high inflation.

The swift demise of the UK Government should follow but does not. Perhaps, more important, is the fact that the prospects of the traditional opposition Labour Party are also suffering. Allegedly, this is because of the burden, and lack of charisma, of the party’s leader. In fact, it is his failure to reflect a militant approach to the unholy trinity of austerity, tight monetary policy, and high inflation which erode his political capital.

The failings of both, the mainstream parties, therefore, present the motive and opportunity for the hastily being cobbled together alternative. The alternative “Britain Project” is a work in progress. The project’s critical pathways, to completion, in the form of a new party, must, hence, by default, accelerate, from here, as the political status quo unravels.

As the status quo unravels in the UK, President Macron has already served up his cold dish of revenge, for Boris Johnson, laced with some of the champagne that he has also poured for the “Britain Project’s” project management team.

UK Foreign Secretary Liz Truss immediately spat the cold dish back in Macron’s face, threatening a potential trade war in relation to the Northern Ireland Brexit protocols. Given Truss’s inflammatory nature, recently evinced during skirmishing with Russia, her reaction is not surprising. Given that Northern Ireland is now, effectively, governed by Republican-leaning Sinn Fein, her reaction risks undermining the Union even further. The Union now faces a debilitating trade war, and the loss of Northern Ireland, at a time of economic crisis. Gamblers, it would seem, double up when they have everything to lose. It would also seem that Truss likes to gamble.

Whilst Britain fights on the beaches, Europe is searching for peace in our time.

The magnanimous President Macron has invited the UK, in general, back into the European tent that he now calls a new “European Political Community”. Evidently, Ukraine is in there somewhere; and there is presumably some room for Russia, sans Putin, et avec cheap gas too. Community global nuncio, Mario Draghi has been dispatched to, the court of President Biden, to see where the American red lines are.

Both allies are seeking to find the right balance, of peace with accountability, whilst avoiding a repeat of the mistakes, made at Versailles, which will simply create a bigger monster out of what is left of the war-ravaged Russian political executive. A Marshall Plan, of some kind, would seem to be the logical outcome.

The eventual, peace settlement in Ukraine should, thus, be placed into the larger context of improving relations between the USA and the EU post-Trump. The process of “Friend-Shoring” of supply chains, away from China, is at the heart of this relationship. A joint Trade and Technology Council is in the process of negotiating and then setting standards for cooperation on the “Friend-Shoring” of supply chains. These standards are based on the removal of trade obstacles and protectionist legacies from the Trump period. This standardization and cooperation are an inherent supply-side economic reform, that will yield disinflationary growth over time.

The UK, and its current government, are, thus, an obstacle to the unfolding trans-Atlantic cooperation. UK regime change is, hence, in the interest of said cooperation. By default, therefore, the “Britain Project” is in the interest of said cooperation.

The “Britain Project” has received a further, perverse, boost from the defiant UK Prime Minister. The latest thinly disguised embrace of Thatcherite fiscal austerity, from the tone-deaf PM, appeared like the leadership failure of abandoning those 1 million Britons left behind in the cost of living crisis. Well, they all vote Labour don’t they? Presumably, they will soon be voting “Britain Project”.

Britain requires competent economic stewards, not demagogues, like the PM and the Foreign Secretary, who create and then exploit divisions in society. Whereas American policymakers, and central bankers, are groping for the 1990s reboot, their UK peers are grasping at the 1980s reboot. As Britain disintegrates the EU, which it abandoned, comes closer together; and the EU and the USA also come closer together.

Britain is out of sync with its two main trading partners. It is trying to replace them with former colonies, whose economies are being undermined by exiting capital flight. These emerging economies are becoming submerging economies, in the economic sense. Britain is converging, by submerging, on these submerging economies.

The fulcrum of the UK economic submersion, identified by Prince Charles, in the Queen’s Speech, is the location of the City at the financial heart of some Submerging Markets trade bloc reminiscent of the Empire. Said submerging Empire is, currently, being “Friend-Shored” by the USA, and the EU. Why Britain continues to offshore everything, in these “Friend-Shored” submerging economies, with the exception of financial services, is a mystery, perhaps, only fully understood by the PM and Chancellor Sunak.

Recently commenting, on the prospects, for the City, in the future, as outlined by Prince Charles, the CEO of NatWest has opined that the Square Mile is currently at the epicenter of a banking fraud “pandemic”. This comment makes one wonder just exactly what kind of financial center the PM and the Chancellor are trying to build, and what kind of Empire they also envision.

The UK economy is coupling to the kleptocratic unregulated side of submerging economies, which are in a downswing, and decoupling from increasingly regulated developed economies, which are driving the submerging market downswing, whilst, engineering their own upswing. The submerging economies are also Beggar Thy Neighbouring each other, and their G7 trade partners. What’s the betting that they don’t also Beggar Thy Neighbour their old imperial master?

One assumes, therefore, that Britain will have to do its own fair share of Beggar Thy Neighbouring, on the lowest cost of production basis, once it has eradicated inflation and much of the economy by blunt 1980s austerity trauma. Maybe Britain will try and do all this simultaneously as Margaret Thatcher did on the advice of Sir Keith Joseph.

This process will be painful for Britain, possibly hyperbolically so. The pain may herald the “Britain Project” when it becomes unbearable.

In contrast, the “European Project” is gaining momentum, also, possibly, hyperbolically so.

From Eurozone to Weimarzone, by way of Kyiv: Hyperbolic Steps ….

· The internally conflicted Eurozone will become a managed command economy for the duration of its structural transformation toward a Federal Republic.

(Source: the Author)

The prospect of a command economy, foreseen by this author, in the Eurozone, has begun to crystallize in Germany. The German government has made it known that as a contingency, to a big outage of Russian oil and gas supply, the Federal Government may nationalize key parts of the economy. The prospect, therefore, now has a real precedent in the Eurozone’s largest economy.

What appears to be happening, however, is both a top-down EU-level and bottom-up national-level drift towards command economy status.

· Faced with populist protest, Eurozone policymakers transfer wealth, for votes, and simultaneously sell Federalism.

(Source: the Author)

In the last report, Mario Draghi was discussed in the context of his position as the custodian of the New Republic of the Eurozone. Draghi is currently gutting the Berlusconi-Putin Axis, in Italy, and re-aligning it with the strategy of the New Republic. This gutting also, as in Germany, has made provision, for nationalization, via the euphemism of the protection of key industries and companies. Mussolini must be beaming, wherever he is.

President Macron’s latest entente with the UK and cryptic signaling about a “European Political Community” are evidence of this New Republic. Further evidence has been confirmed with the latest Franco-German entente, which deepens, and aligns, their military and foreign policy strategies further.

Where President Biden is delicately allowing mission creep to drive his supply chain stimulus, from global military to domestic fiscal stimulus, the Europeans are actively driving the process. This is what happens when the political executive is not directly accountable to a national electorate.

The EU is currently formulating plans to issue joint bonds for the reconstruction process in Ukraine. Hence the Ukraine war has become a war for economic European political integration, via fiscal integration, into the New Republic.

In addition, Climate Change and the pivot away from Russian hydrocarbons are binding the New Republic together. This pivot has begun with a draft EU plan for renewables and energy saving. The cost of the plan is set at $205 billion. This is trivial and will not move the pivot needle. If the EU is serious, Trillions of Euros will need to be printed and spent. The initial cost is, hence, a baseline estimate that will not scare taxpayers. From this baseline, the cost, and, hence, the size of the fiscal stimulus will grow over time. The ECB’s balance sheet will then be called upon when it’s time to avoid scaring the taxpayers even more.