· Dimon’s Hurrikraine signals that the current inflation narrative is less important than what lies beyond it.

· Dimon’s Hurrikraine implies that heavy-handed central bankers will need to apply their heavy hands with ambidextrous flexibility, going forward, with the further loss of their credible commitment.

· Dimon’s Hurrikraine confirms the Key Signals Fed easing signal of the first week in May.

· Dimon’s Hurrikraine correlates with the emerging strong US Dollar growth headwind narrative nudging for a global managed trade/FX regime solution.

· Now would be a good time for the Fed to start some thought leadership on a new definition of full employment.

· The Federal Reserve and Federal Government are separately fighting inflation, whilst simultaneously fighting each other.

· It’s Slam Dunk time for the Biden New Multipolar World Order.

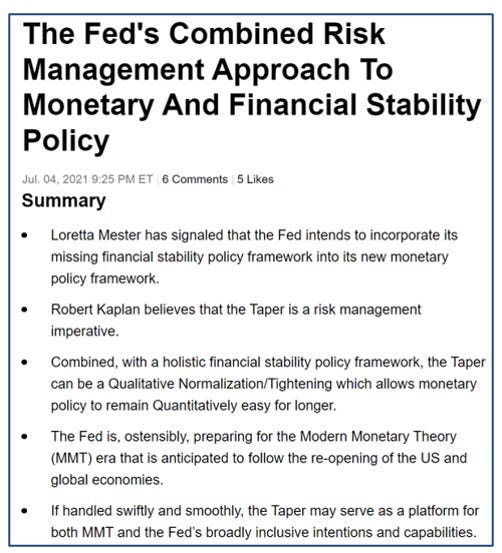

· The Fed is still Qualitatively Tightening whilst Quantitatively Easing to enable a soft landing.

· The Fed is hiking interest rates to salvage credible commitment rather than to fight inflation.

· The Fed is still more interested in MMT than it is about conventionally fighting inflation.

· The Fed’s continued interest in MMT confirms that its real mandate is financial stability policy rather than its dual mandate.

· Alleged Quantitative Tightening, through securities maturing, is not as tight as through outright securities sales.

· Alleged Quantitative Tightening, through securities maturing, is apparently synonymous with an economic soft landing.

· Fed Governor Waller’s Beveridge Curve steals Mr. Market’s valor and frames it as credible commitment.

· The UN is the latest global organization to proselytize “Macklem Doctrine”.

· The recently announced “German Pivot” is the next biggest transformational economic event in the global economy year-to-date after the Biden Slam Dunk.

· The UK PM steals a Bushel of the Queen’s valor to buy a Gross of political capital.

· The Queen’s stolen valor is celebrated with Jubilee industrial unrest.

· The UK Own Goal is the prelude to a Slam Dunk.

Blow me, if we aren’t all Hyperbolic Keynesians, now! (sic)

“Nothing vast enters the lives of mortals without a curse.” (Sophocles)

When Sophocles warned “that nothing vast enters the lives of mortals without a curse”, he may have had the word hyperbole in mind.

Jamie Dimon appears to be the latest AccursedHyperbolist. His timing, as always, is flawless. According to Dimon, his bank is bracing for an economic “Hurricane”, from the combined headwinds of central bank monetary policy tightening and the war in Ukraine. Dimon’s Hurrikrainehas already been claimed to be blowing a Bretton Woods moment. If this “Hurricane” was to blow recessionary headwinds, that were then discounted into falling energy and commodity prices, Dimon’s laconic smile would, doubtless, broaden into an esoteric smirk.

· A Key Signals proprietary indicator signals that the FOMC is, once again, totally off with its timing, this time, on monetary policy tightening.

Transfixed, by Dimon’s enigmatic smile, this author immediately remembered that, back in the first week of May. the Key Signals proprietary indicator had signaled that the Fed should now be easing monetary policy.

Further support, for the Fed easing thesis, has recently been provided by the news of labor market attrition.

News of consumer attrition, and a significant inventory overhang, from Walmart, has also suddenly overturned the tight supply chain inflation-driven narrative.

This author is especially taken by the latest news that the Tech Sector cut nine times as many jobs as it did in the first four months of the year in the first week of May.

Mr. Market is also falling into line, with the slowing growth narrative, as the first net bond fund inflows, of this year, were recorded in the first week of June.

The Accursed Hyperbolist Dimon is not alone. He is in the good company of the Wall Street cognoscenti. Collectively, their voices make a tipping point mantra. Inflation is old news, what lies beyond is where the real action is.

In a recent speaking engagement, Goldman President John Waldron opined that “the independence of the Fed has been damaged in recent years and that it has lost credibility in markets”. The inference is, that the loss of independence is through capture by the political executive. In fairness, Goldman had no issues with this political capture when Wall Street was being bailed out during the GFC. This may, therefore, be a case of the pot calling the kettle black. Nonetheless, the clear nexus of US Treasury and FOMC control has been exposed.

Goldman’s President John Waldron is more understated, than Dimon, but just as alarmist.

Waldron sees a “confluence of unprecedented events”. One senses that the firm is short risk and looking to finesse closing out the position, possibly, even by going long. Timing is everything, so Waldron is collapsing economic time around the firm’s trading book.

Goldman’s Senior Chairman Lloyd Blankfein knows a Credit Crunch when he sees one; because he presciently Big-Shorted and covered, at the bottom, when he was at the helm of the firm during the GFC. His old colleague Hank Paulson was also Treasury Secretary, at the time, so this suspiciously conflicted relationship must have helped too!

This time around, Blankfein is advising all market commentators to “dial back a bit”, thereby, avoiding another self-fulfilling prophecy. Goldman called the economic slowdown back in December 2021, when it revised its US GDP targets for 2022 downwards. Blankfein wants to be vindicated by a soft-landing rather than another GFC.

Blackrock’s CEO Larry Fink sees intractable inflation, beyond the Fed’s reach, in blocked supply chains, for years to come. This implies that the current monetary policy tightening is, in fact, all about credible commitment optics rather than inflation-fighting substance.

Fink is, in fact, making the case for a supply-side fiscal stimulus, which, presumably, is what Blackrock will already be positioned for. Fink also makes the case for G7-led global governance rules, with his disclaimer that asset managers should not be performing this task. Presumably, Blackrock is also invested appropriately for this new global governance architecture.

The head of Carlyle Group has recently opined that the momentum trade is dead. This author notes that the momentum currently resides in the energy complex, and is still in robust health. Were it to die, Jamies Dimon’s “Hurrikraine” warning would be more than apocryphal.

Larry Summers’ beaming smile, of late, definitely isn’t cursed. If anything, it is vindicated. Perhaps it is even a little vindictive, like Old MacHeath Dear.

The beaming Summers is, currently, basking in the limelight of calling inflation right. In effect, Summers cursed the Fed, back in early 2021, when the central bank was beguiled, by Secretary Yellen, into being broadly inclusive, amongst other Woke epithets. Inflation, and the rest, is history. The fallout has been epic, with all involved seeking to exonerate themselves from the blame for inflation. Some have even gone to the length of publishing their exonerations.

Secretary Yellen’s amanuensis has recently published her exoneration in prose. This latest biography is curious in that it has been published, prematurely, before the subject has officially retired from her current job.

Readers should remember that Ben Bernanke has just released a critique of 21st Century central banking. The coincidence with Yellen’s new biography is suspicious. This is not so much a case of Monday Morning Quarter Backing as a Grand Inquisition of monetary policymakers by fellow monetary policymakers. Usually, central bankers do not eat their own. This sudden cannibalism belies a general loss of credible commitment, for all, followed by blame, betrayal, and recrimination. It is the end of days for central bankers, as we have known them. What lies ahead may resemble even more of a fiscal agency role than the faux independence that central bankers have enjoyed thus far.

Evidently, Yellen wishes to have her own version of events out there, by way of legal deposition, before she gets lumbered with all the blame. Apparently, she wanted to have the Biden fiscal stimulus diluted by one-third of what actually happened. She was overruled by the President and Congress. Hence, Yellen is only guilty of following orders, from a democratically elected set of lawmakers, so she is off the hook legally speaking.

Through his bared teeth, Old MacSummers is currently peddling the thesis that the Fed’s tightening is already working through to building inventories and falling labor demand.

· Aggressive monetary policy tightening may be a vanity project, in pursuit of lost credible commitment, that will undermine the Macklem Doctrine Solution for the New World Order.

In environments like the current one, central bankers should tread carefully. If they are heavy-handed, they should be flexible with said heavy hands. Currently, they are viewed as heavy-handed. By default, therefore, this implies that they will have to become flexible and ambidextrous with intermittent tightening and easing.

· The Macklem Doctrine of America’s global imperative may make bigger fools out of the FOMC than the incoming inflation data.

Therefore, one may expect swift monetary policy tightening to be followed by equally rapid monetary policy easing, assuming that a fiscal stimulus does not get there first. Even if fiscal stimulus gets there first, central bankers will be circumspect about choking off the growth that follows. This ambidextrous flapping, of central bankers’ hands, will do nothing for their already shattered credible commitment. Unfortunately, that is just the way it goes.

In short, expect big a big fiscal deficit and a big Fed balance sheet. Also expect an inflation narrative, from the Fed, which complies with the patriotic narrative. The Soft-Landing would be the patriotic narrative of choice. Then, trade and invest accordingly.

Global macro events, of such magnitude, like these, oftentimes, are the catalyst for Big Change. Big Change, always, requires Big Bucks. Just as often, these changes require the excesses of monetary and fiscal policy which originally led to the crisis that militated for the said change. Plus ca change plus c’est la meme chose.

The founding father of the Twentieth Century New World Order, John Maynard-Keynes, fundamentally understood the Sophoclean curse that he had introduced with his economic solution to end all wars. This curse is not, as Friedman believed, the inflationary outcome. It is the curse that history fails to avoid repeating itself. Inflation does not change the response, it just makes it more creative each time it is repeated.

The reader may, also, note that Keynes’s solution did not end all wars, either. In fact, the current war in Ukraine can trace its lineage back to the failed solution of which Keynes was a part.

If history appears to be going around in circles, that is because it is. Guns and money perpetuate these cycles, and circles because they are the only toys of the only game in town.

It is easier (and often cheaper!) to apply the same solutions, with a different narrative, and artifice, than to re-invent the wheel. Behavioral economics notes that humans are hardwired to take what appears to be the easiest option, at first choice, without exhaustive data and analysis. If one didn’t die the last time the same option was taken, then one can be easily fooled into taking it again even if it is suboptimal. The fact that there are never any real control experiments to observe, to understand different outcomes, only serves to reinforce convictions and biases over time. Even extensive analysis leads to paralysis which then calls for a quick fix. Then there is the fact that history is written by the alleged winners. Winner’s Bias is not currently listed in behavioral economics, but perhaps it should be because it is pervasive and extensive throughout history.

Since there is significant compounded wealth, give it a name “Skin-in-the-Game”, invested in maintaining the economic status quo there is also a significant obstacle to change.

· Some G7 central banks are self-isolating, from the regime change virus, to save themselves by fighting inflation.

Hence, as Milton Friedman observed, “we are all Keynesians now.” It seems that we were born this way. It also seems that, in practice, Keynesians must, by default, cooperate if they are to be successful. This cooperation is a necessity of the requirement for combined monetary and fiscal stimulus to deliver true Keynesian outcomes. When the monetary and fiscal policymaking executive is in conflict, one can expect sub-optimal outcomes. Currently, the two are in conflict.

The Fed is currently trying to redeem its credible commitment, by appearing to fight inflation, whilst the Federal Government is trying to redeem its political franchise with fiscal expansion. The two are destined to clash and the Fed is destined to lose because it devolves its legitimacy from the political executive.

What then will become of the 21st Century Fed?

A New World Order through Managed Trade and Managed FX Rates? (II)

Back in the day, when President Trump was engaging in his own form of “Friend-Shoring”, this author suggested that the outcome would, most likely, be a brief currency war that would lead to a managed trade/FX regime. Under this regime, central banks would become little better than currency boards. Given their recent inflation-fighting performance this is, arguably, all that they are good for. This option now must be placed back on the table, and its level of estimated probability evaluated continuously.

A recent report explained that it may be time to dust off the managed trade/FX regime playbook again. Recent news from US software companies suggests that the time is right. US Dollar strength is repeatedly cited as an earnings headwind going forward. For earnings headwind, one should read economic headwind.

Alternatively, or correlatedly, the strong US Dollar may get cited, by the FOMC, as a reason not to tighten aggressively. Such hinting would also suggest that the Fed’s ultimate 21st Century role, in a world of managed trade/FX would be that of a simple currency board manager. The Hong Kong Monetary Authority has been performing this role admirably for years, so there is a precedent.

Mr. Marketis wearing his Global Macro hat, nowadays, more than any other trading style, so one senses that an impending global macro policy solution is being framed and inculcated into his price discovery narrative.

If the Global Macro hat is to fit, appropriately, then, it also needs context. There is no shortage of context on offer in the form of guidance, and opinion, these days.

Time for a new definition of full employment?

· In view of the thirty-year narrative timeline compression, the Fed has limited time and space available to taper.

· The Fed’s pivot from its inflation mandate to its employment mandate will require a new definition of what full employment means in relation to the COVID-19 experience.

At the beginning of the year, this author suggested that a new definition of full employment would be required, this year, when the Fed realizes that tight labor markets can co-exist with a slowing economy. This time has arrived.

Now would be a good time for the Fed to start some thought leadership on the new definition of full employment, so that by the time Jackson Hole rolls around, and the pressure is on to deal with a slowing economy, the central bank at least has a bookmark to refer to when it U-turns.

When inflation is everywhere a political phenomenon ….

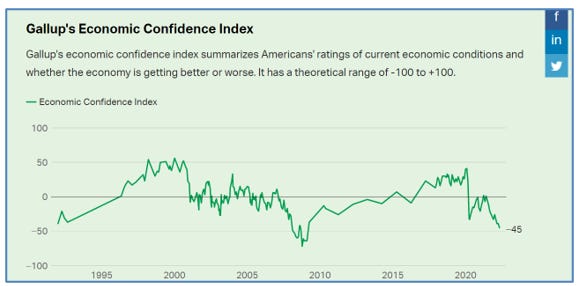

The latest Gallup economic sentiment indexes show pessimism plummeting, through the COVID-19 lows, towards the Credit Crunch lows. The data also show that poor political leadership is still conflated with high inflation. High gasoline prices are not conflated with high inflation. In fact, gasoline prices and Russia are way down the list of worries. High inflation is not conflated with Russia and or Chinese supply-chain issues.

Coincident, with these Gallup sentiment revelations, was the widely advertised meeting between President Biden and Chairman Powell. This was, clearly, an opportunity to try a bit of blame laying by both gentlemen. It was also the opportunity to come together with a plan to get out of this mess. There was no meeting of the minds. Biden blamed the Fed for inflation and swore to implement interventionist policies that would make it appear to disappear. The Fed and the President are fighting inflation, individually rather than as a team. They are also fighting each other. There may be no “I” in team, but this means that there is a big “I” in inflation.

If only the Fed and the Federal Government could find someone else to blame for the global supply chain woes and inflation. If blaming this someone also required disinflationary, deficit financed, supply-side investment then both could stop blaming each other, and get on with the financing.

President Biden has, so far, failed to convincingly blame either President Putin or China, for America’s current economic problems. His attempt to deliver the solution, in the form of more supply-side stimulus is, thus, challenged. The facts have clearly changed. These facts signal that it is game over for the Biden administration.

Faced with defeat, President Biden will change the play rather than concede. This is what he does.

The New World Order, that Biden has proselytized, is, currently, stillborn at home. Furthermore, any attempt at a Greenspan-style 1994 economic landing, by the Fed, is also getting seriously challenged. The economy is now more likely to crash-land, under the combined vectors of high inflation and rising interest rates.

US Presidents never let the facts get in the way of their own subjective truth, however. Neither do FOMC members. The reader should remember how stubborn permanent inflation did not get in the way, of the infamous transitory inflation thesis, until it did. The author expects the President to start blaming the Fed for undermining his supply-side solution. FOMC speakers are providing opportunities for the President’s means and motive. Presumably, these same speakers are also blowing the “Hurricane” that is cooling Jamie Dimon’s pies.

Bada Bing, Bada Bang Bang, Bada Economic Boom ….

Strategists also know the maxim “that it is pardonable to be defeated, but never to be surprised”. President Biden is looking neither surprised, nor defeated. In fact, POTUS predicted the Ukraine invasion days before it happened. Unfortunately, he did not make a prediction when he was Vice President and NSA Rice issued the original threat alert. The maxim that one should never interrupt an enemy that is making a mistake also now comes to mind.

The last report discussed the probability that President Biden has been involved in the endgame for President Putin, ever since he was Obama’s Vice President.

Further details of this endgame thesis have recently come in, with the news that President Putin had been operated on for cancer, and had also survived an assassination attempt in March. President Biden is nothing if not tenacious. Evidently, he is also resourceful. This author would, therefore, not prematurely rule out the tenacious US President getting his fiscal stimulus and removal of President Putin just yet.

It's Slam Dunk time ….

There is, however, a way for the uniquely unfortunate President-Colonel/Brigadier-General in Chief to avoid the Hague, if he is deemed to be too ill to stand trial. Incarceration, and ostracism, in a sanatorium, would be the sentence; thereby leaving the exonerated chain of command upwards to negotiate peace with honor. Strangely enough, this sentencing is already taking place in the criminal court of the public domain.

The last report presented the endgame scenario, for President Putin, of charging him with war crimes whilst mercifully allowing him to serve out his sentence in the sanatorium rather than the Gulag.

This endgame is now being promoted in the media. Before regime change occurs, however, maximum political and economic mileage must be made out of the current situation by President Biden. This mileage is just about to be clocked.

Portentous leaks, from White House trusted sources, have also let it be known that America’s whole national security strategy is currently being redrafted. In short, this redrafting is the incorporation of the Russian narrative into President Obama’s original Pivot toward China.

The Trump interregnum is also, effectively, expunged from the national security strategy by default of the Russian narrative. History is, indeed, kind to those who write it.

But, one simply does not rewrite a national security strategy, on the fly, if one is the greatest superpower that the industrialized world has known so far. If one did, it would imply strategic blindness which should prompt the firing of all one’s intelligence agencies for missing the obvious. Apparent strategic blindness has its uses, however, if it is sold properly. Then, a strategy that has been formed over a much longer period of time can be executed as an alleged matter of unforeseen urgency.

Readers should remember that Russian meddling in the US Presidential election, which led to the Trump Presidency, was called out, on Biden’s VP watch, by Adviser Susan Rice. Rice was supposed to be President Biden’s Secretary of State, but Hillary Clinton nixed it in typical Clinton style.

It is, therefore, highly likely that the current national security redraft, inclusive of Russia, was originally being drafted back when Biden was Vice President. People often wonder what Vice Presidents actually do. As George H W Bush and Dick Cheney have shown, Vice Presidents prosecute the wars that the President can’t make without Congressional approval. It is therefore a myth to say that the US President is the most powerful man in the world. That title belongs to the Vice President. The President’s job is to go to Congress to get approval for what the Vice President has set up. President Biden will thus submit the new national security draft for Congressional approval on behalf of Vice President Harris.

This is what is known as the infamous “Slam Dunk” in policy wonk vernacular. These Slam Dunks have a habit of misfiring, several years later, with unintended consequences. It is the Vice President’s job to create the narrative to deal with said unintended consequences and the new conflict that they will present to Congress, for approval, if and when they become the next President.

The current Slam Dunk also envisages a greater role, in global policing, for a European policeman. A New Multipolar Word Order moment is at hand.

First, however, the US domestic economy and its voters have to be primed for global macro adventure.

When the facts change, it’s more Beige than Grey, at first, then it becomes Black and White ….

· The Regional Fed’s view of the US economy is, currently, more accurate than the FOMC’s.

The regional Federal Reserve districts change their minds, and the Beige Book commentary when the facts change. Of late, the commentary has lowered the growth vectors as the result of the combined pressures, of rising inflation, and interest rates. Four districts see growth stalling, whilst, three see inflation dissipating. The FOMC appears to be oblivious, much rather cognitively blind, to this new regional message.

The change in guidance from the regions is diverging, once again, from that of the FOMC.

The counterfactual, from the labor market, is even more important. The latest ADP data shows that small businesses are contracting, their workforces, in the face of rising costs and tighter credit conditions. It was fondly imagined that small businesses would pick up the baton as the Federal authorities wound back their unprecedented COVID stimulus. This just isn’t happening. In fact, on the contrary, small business owners are abandoning the field as they see the Federal Government retreating. Double-digit layoffs are also being announced from the alleged, growth sector, of Large Cap Technology so the weak employment story is universal. This weak employment story did not hit the latest employment situation report, however, the next report will be scanned for evidence of its appearance.

When the facts change, we still hike fifty basis points …. Go figure.

A trinity of FOMC speakers, spanning the Doves and the Hawks, all hold the consensus to proceed, with 50-basis points incremental interest rate hikes, regardless of signs of an economic slowdown. It is, in fact, the economic weakness that they crave, in order, to fight inflation.

One of the trinity, San Francisco Fed president Mary Daly, openly admits that she is “comfortable” weakening economic growth with 50-basis point interest rate hikes until she sees that inflation has irreversibly turned lower.

· The “Bullard Put” seeks to avoid recession by promising to ease in 2023.

Daly’s colleague, St. Louis Fed president James Bullard, appears to be anything but comfortable. His discomfort has prompted him to frame the potential recession, portended by the FOMC’s actions, as the “Disinflation”. In response, to said “Disinflation”, he intends to start easing again in 2023.

The third member of the trinity, Richmond Fed president Thomas Barkin, believes that it makes “perfect sense” to tighten monetary policy.

Whilst the trinity frames the windows, of the next two FOMC meetings, their Hawkish colleagues are already framing the windows that lie beyond.

Maam, Yes, Maam! Gimme fifty more ….

Cleveland Fed President Loretta Mester has explained why she is discounting the slowing growth evidence, in order, to focus exclusively on bringing inflation back to target. This is, allegedly, a matter of risk management. On balance, in her balance of risks, high inflation is a much worse thing for an economy than high unemployment.

This author remembers a time, only a year ago, when Mester was being broadly inclusive, with her balance of risks, favoring employment creation, with the neat combination of a commitment to overshoot the inflation target. This memory, thereby, debunks the current narrative that Mester is a real inflation fighter, first and foremost. She is capricious and has poor timing.

Recently anointed Fed Vice Chair Lael Brainard is sticking to the script that got her nominated. Gone are the “Woke Luvvy” epithets that used to punctuate and frame her guidance. Vice ain’t no Luvvy, she be a Hawk. Through her Hawkish framed lenses she “finds it hard to see” any case for pausing the 50-basis points rate hiking process in September. Mester concurs.

Brainard is an American first, and second the Fed Vice Chair, after recently being sworn in. In this context, her interpretation of the Fed’s dual mandate is, therefore, subjective and, hence, subject to her patriotism. In these times of uncertainty, where America is threatened, it is, therefore, logical to expect that her monetary policy action will fall into line with the patriotic cadence first, and foremost.

As this author also observed, in the last report, Brainard is a “Cold Amazon” when it comes to enabling America’s global manifest destiny. Indeed, patriotism, beyond the dual mandate call of duty, appears to be an essential job description for all Fed Governors. Governor Christopher Waller is no exception to this rule.

Fed Governor Christopher Waller recently explained how his interpretation of the Beveridge Curve has changed, which thereby obliges him to change his mind about the labor market. He now assumes that tight monetary policy will not lead to falling job vacancies.

The reader should understand that for, at least, one year Waller has ignored the fact that inflation has not been transient. Any thesis he puts forward is, thus, made suspect by the fact that he is slow on the uptake. It may, hence, always be too late when he finally thinks that he has understood what is going on. It, thus, follows that Waller’s new interpretation of the Beveridge Curve is in error.

Waller’s recent speech was most interesting to this author because it picked up the cadence where Fed Vice Chair Lael Brainard left off in the last report. Brainard’s last speech was a Washington Policy Wonk’s cadence for monetary policy combat in a New World Order. The Vice-Chair inspired and challenged a bunch of green college graduates to fall into line, and follow her blazing career trail, into battle for Uncle Sam.

Waller’s recent speech was aimed at America’s German allies from the Institute for Monetary and Financial Stability (IMFS). Apparently, the Fed and a few good German men and women are going to apply their skills, in the dismal science, to defeat their nemesis from Russia. They will simultaneously defeat inflation. From there, they will, then, bring peace and prosperity through sound monetary policymaking decisions.

After the common-bonding stuff, Waller then explained why a soft economic landing is also within reach for the allies. Since bond yields and mortgage rates have spiked, well in advance of the FOMC actually doing anything, the ensuing economic deceleration is now at an advanced phase. Consequently, it will only take a few more 50-basis point rate hikes, from the FOMC, to catch up with the forward curve and the tightening will be over.

Applying his own fitted Beveridge Curve, Waller believes that the labor market will still be tight because (a) there is a skills mismatch between applicant and vacancy, and (b) because the unemployed vicariously flip in and out of the labor pool. The unemployment rate will, hence, not spike and there will be no recession. In reality, the unemployed flip in and out of welfare, and debt-penury, but Waller is oblivious to this.

This author would say that Waller’s analysis is academic at best. Its context is dubious, to say the least. Those people who are flipping in and out of the labor market are living on the margins, hence, they are not great drivers of aggregate demand. They are also being hammered by inflation and rising interest rates.

Waller also fails to address the rate of creation of skilled jobs. In this author’s opinion, this failure is egregious. Just because there are skilled vacancies, it does not mean that they are being created at a rapid rate. Waller needs to go back to calculate the rate of creation of skilled jobs and compare this with the rate of change in GDP. This author notes that an economy that has a low rate of production of skilled jobs, by default, has a lower growth potential. Waller has simply discovered the fact that America is a mature developed economy, with productivity issues that require supply-side solutions.

This author would also say that Waller fails, perhaps deliberately, to understand that the spike in bond yields and mortgage rates was caused, in principle, by the Fed’s failure to react to inflation with alacrity. He prefers to look at the spike as a result of strong extended forward guidance.

The Fed failed to respond, to inflation, so Mr. Market, via the forward curve, tightened for the central bank. Waller and the Fed are, therefore, stealing Mr. Market’s valor and taking credit for the application of said valor. Mr. Market’s stolen valor is egregiously recast as Fed credible commitment. Waller’s dissemblance is misleading at best, and disingenuous at worst.

This author suspects that, in reality, and real-time, the US economy is moving towards a phase in which expensive capital substitutes for expensive labor. The productivity question, that Waller avoids, hints at this outcome. Technology solutions are also being applied to the input costs associated with energy, raw material inputs, and congested supply chains.

Unskilled/less-skilled labor is surplus to requirements and is being forcibly nudged towards the Federal Government’s fiscal soup kitchen window. The Fed used to dish out liquidity at this window until inflation second-guessed this broadly inclusive behavior. Now the Fed chooses to focus, exclusively, on those with skills in demand.

The soft landing that Waller sees on his Beveridge Curve is, therefore, academic. The reality is much different. This author expects to wait, for at least another year, for Waller to catch up with the reality on the ground and then refit his Beveridge Curve accordingly. This is what academics in ivory towers do.

When the facts change, I change my narrative, but I don’t actually change my mind ….

· The Fed may embrace Macklem Doctrine when it sees the unrealized losses on its balance sheet from the recent spike in yields.

When it comes to “Skin-in-Game” nowhere is so much skin to be found as on the Fed’s balance sheet. The current story goes that this skin is about to begin running down, through maturing securities, on June 15th. The real story is that the skin will not be run down through securities sales.

Playing this game is currently estimated to have cost the Fed $458 billion of unrealized losses, so far, of which some $300 billion is from mortgage-backed securities (MBS). This author has suggested that the realization, of these losses, and the associated loss of credible commitment, would be something that the Fed could never recover from.

· The balance sheet discussion in the latest FOMC minutes was the Soft-Landing signal.

Consequently, in view of the loss aversion, this author suggested that the Fed would let its balance sheet shrink via the maturing and roll-off of assets. The residual balance sheet would, then, be of such a size as to provide the economic cushion required for the Soft-Landing.

Readers may remember that, back in July 2021, this author described, in detail, how the Fed would Qualitatively Tighten whilst Quantitatively Easing. The result of this Qualitative Tightening process has been the credit headwind, and the sudden deceleration in economic activity, which has recently been commented upon by many sources. The result of the Quantitative Easing piece, of the combination, is a legacy Fed balance sheet of the scale which provides the liquidity cushion for the Soft-Landing. The Fed has, ostensibly, maintained this combined position, ever since it was flagged by the author. During this period, inflation has run out of control, but despite Hawkish guidance, the Fed has still adhered to the combined position.

The Fed has paid lip service to the inflation problem, yet maintained its fundamental Qualitative Tightening whilst Quantitatively Easing bias, until now. Even now, the conventional inflation fight is only just happening as the economy is already slowing. The economic slowdown will do far more price inflation-fighting than the Fed.

· Inflation is being primarily fought with financial stability policy tightening rather than monetary policy tightening.

The real story is about the Fed maintaining its loose unconventional monetary policy setting bias and then only tightening conventionally when it is clear that the tightening will not be able to go too far. This behavior is best explained as consistent with a central bank that is primarily targeting financial stability rather than inflation or employment. In effect, inflation and employment are determined by the level of financial stability that the Fed is primarily targeting. Mr. Market’s risk-on/risk-off phase change behavior is further confirmation of this thesis.

There is an implicit acceptance, of higher inflation, in the Fed’s explicit financial stability policy-driven actions. One could almost say that the inflation is desired. As originally signaled, by Loretta Mester, in July 2021, the Fed has been fighting inflation with financial stability policy, at least, since then. This author would set this datum back to May 2019. Tightening financial conditions have delivered the economic headwind that arrests inflation by slowing the real economy down. The Fed accepts that even though the inflation, is supply-side in nature, it has no alternative but to deal with it with financial stability policy tightening.

At the end of the day, however, the Fed is really in the asset price targeting business, since this is the only economic indicator that it can directly influence with monetary policy. Fed Governor John Exter already told us this a long time ago, so take everything else that the Fed says with a huge pinch of salt.

The school of thought which believes that the Fed’s real mandate is to manage financial asset prices would appear to be vindicated by the central bank’s behavior so far. For this author, it’s just déjà vu all over again. Back in May 2019, he observed that the Fed was really in the asset pricing business. This is still the case.

The inflation spike narrative and remedial aggressive conventional interest rate hiking, by the Fed, is, as stated by the author, an attempt to salvage credible commitment. Once the credible commitment has been salvaged, the Fed will, then, be at liberty to revert back to its asset price targeting mandate.

The Fed never was serious about fighting inflation, because it was more serious about Modern Monetary Theory (MMT). The Fed continues to be more serious about MMT than it is about fighting inflation. This is understandable.

The Fed understands that supply-side inflation is beyond its remit, it is however obliged to appear to fight inflation, with an inappropriate financial stability policy tool, in order to rebuild its credible commitment. Perhaps the Fed also understands that inflation itself is the most aggressive and indiscriminate form of monetary policy tightening tool in its toolbox.

The recent appearance of press stories about the Fed’s unrealized losses closely correlates with the Soft-Landing narrative under construction. This narrative neatly segues into the emerging global narrative, in the developed economies, that supply-side economic stimulus is needed to break the stalemate with China and unblock inflationary tight supply chains. This process has been dubbed “Friend-Shoring” by Secretary Yellen, and “Macklem Doctrine” by this author.

The last report discussed the current narratives doing the global economic rounds in relation to Ukraine, Russia, and China, etc., etc. The narratives, under construction, make the case for Keynesian economic stimulus. This author has given the narrative the title of “Macklem Doctrine” with respect to, one of its first movers, Bank of Canada Governor Tiff Macklem. Essentially, the doctrine involves the thesis of supply-side investment, in friendly democracies, to “Friend-Shore” supply chains, away from unfriendly dictatorships, in order to sustain disinflationary economic growth.

The “Macklem Doctrine” narrative has been careful to frame the Ukraine crisis and China’s “COVID-Zero” policy as Stagflationary threats to the global economy. Since the threats are global, by necessity, the solution must also be global.

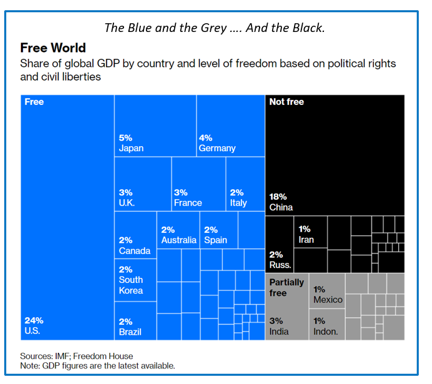

· The United Nations is the first global casualty of the new multi-polar world order.

It is, therefore, timely that the United Nations has recently called for a concerted global supply-side investment program to defeat inflation, avert disasters and evade conflicts. It’s win, win, win. The UN has been on the back foot since a robust outbreak of global hostilities, through competing visions of what the New Multipolar World Order (NMWO) should look like, occurred earlier this year. The UN is now using the results of the hostilities to regain the initiative by framing a solution under its aegis.

The UN has been vague about who will pay for this solution. It is, however, clear that there will be a big peace dividend in the form of economic growth and low inflation. Presumably, this economic outcome will beget low rates of interest and higher levels of productivity that will make the massive pile of debt, that underpins it, sustainable. This author observed a similar narrative playing out, after the first Gulf War, under the careful stewardship of Chairman Greenspan and a handful of good central bankers. He notes that all these narratives always seem to have energy as their basis.

· The ultimate New World Order, enabled by Macklem Doctrine, will have its own specific financial bubble in addition to “intransient” structural inflation.

This author thinks that for the current NMWO thesis to work, cheap energy is required. What he has noted is that hydrocarbon energy is not cheap and neither is clean energy. This does not, however, mean that high energy price inflation will require tight monetary policy. On the contrary, the high cost of energy, in manufactured goods prices, will not be able to be passed on to consumers because they are also spending most of their incomes on energy themselves.

The cost of energy will, thus, become a significant tax on both consumption and production. The problem for elected policymakers will be in telling this truth to the electorate, whilst keeping their political franchise. Currently, the electorate is being bought off with energy price caps and other fiscal fudges. If the electorate remains passive and accepts this form of a social contract, then, this Green New Deal may survive the test of time. What is certain, however, is that consumers will have to be happy consuming less. Since the eternal quest for economic growth, and shareholder returns, is predicated on happy excessive consumption, there is a big wake-up call for all developed economies ahead.

As the Eurozone wakes up, the ECB’s thought-leadership police are hurriedly making the case that unified fiscal policy is the great solution to the challenge. Missing from the proselytizing is the fact that unified fiscal policy is the gateway drug to full political integration Nirvana.

Eurozone enlargement is going further than just thought leadership. The ECB has gleefully announced, much to the chagrin of Russia, that Croatia is converging on a full Eurozone membership basis in 2023.

· The Villeroy and the Bosch strategy achieves economic union through the destabilizing of national democracies with EU sanctioned fiscal irresponsibility and central bank moral hazard.

· Villeroy’s New Multipolar World Order (NMWO) seeks to share Liberty, Equality, Fraternity, and the American Exorbitant Privilege to finance fiscal irresponsibility.

Seemingly, in anticipation of the arrival of the twentieth Eurozone member, Bank of France Governor Francois Villeroy de Galhau has continued to blow his trumpet. The movement being played, by him, is one of economic and political integration, with a subtle undertone of global reserve currency status for the Euro equal to the US Dollar.

This author has named the piece Villeroy and the Bosch in homage to its progenitors. Further evidence of Eurozone integration, via consolidation, has also been provided by Spain’s Acerinox’s recent consolidating move on Holland’s Aperam. A similar wave of consolidation is currently conjoining Southern European telecommunications operators.

As Europe pulls together, Britain pulls away. More on this divergence later.

The European Pivot, to the Federal Republic, by way of the Great Wall and the Luhansk Wall….

· Sanitization efforts are turning towards China, even before Russia has been sanitized.

The last report noted the haste with which China was being framed as the Global Bad Guy, even before President Putin had been “sanitized”.

We’ve been expecting you, Chancellor Scholz ….

Readers should not be too worried, by Germany stepping beyond its borders. Germany chairs the G7 this year, and is, thus, obligated to appear to lead, from the front, by following behind the global consensus. This chair position is, in fact, a nightmare for Germany because it has exposed all the country’s conflicted double-dealing interests in Russia.

This author has, also, noted Germany’s awkward advance to contact, with the New Multipolar World Order, through the prism of its historical experiences with New Orders past. This has not, however, dissuaded German policymakers. It has simply made them more cautious.

It was with great caution, therefore, that Chancellor Scholz began the German, hence Eurozone, Pivot towards confrontation with China. These are tough times for Germany. Russia is/was its biggest energy supplier, and China is currently its largest trading partner. Germany has more skin in the NMWO game than any other Eurozone nation. Turning away from its two biggest trade partners is no small thing. Turning away is also irreversible for Germany.

Germany is, however, uniquely blessed with the historic ability to make big moves. Readers should think of the collapse of the Roman Empire, the Saxon Invasion of Britain, the Holy Roman Empire, the Teutonic Knights, the Protestant Reformation, and the Religious European Wars, in addition, to the Two World Wars, and Unification as examples of historical German big moves. It’s what they do. These big moves are often unpleasant for those on the receiving end. Germany is now making a big move and taking Europe with it.

A genocide speech in relation to the Uighurs should now be expected. The ground has already been prepared, with leaked information about the detention and abuse of Uighurs in concentration camps.

In the last report, this author suggested that China’s treatment of the Uighurs would replace Putin’s Ukraine occupation as the new global genocide narrative. Chancellor Scholz has recently embraced and promulgated this new narrative. Well, if anybody is able to call genocide when he sees it, it is most likely to be a German!

The Chancellor then went on to accuse China of creating the next Emerging Market debt crisis, through its opaque lending and poor global governance practices. The irony, that German lending practices in Russia have done, exactly, the same thing was clearly invisible up on the moral high ground that Scholz was preaching from. Well, if anybody is able to call corruption and poor governance when he sees it, it is most likely to be a German!

Scholz’s condemnation, of China, contrasts strongly with the gentle reminder from the UN that any such ethnic clampdown should follow the rule of Chinese law. The UN condones, whereas, Germany condemns.

After crossing the Rubicon, by calling the Chinese kettle manufacturer black, there is now no choice, for the German pot manufacturer, other than to decouple from its largest trading partner.

The German Pivot, away from Russia, and China is the most significant event in the Eurozone, since its inception. After President Biden’s national security policy redrafting, it is the next biggest thing to impact the global economy so far this year. And, it is only June, so how many more big things are coming before year-end?

The German Pivot is a structural economic event of great magnitude, and profound importance, for the global economy. This singularity is also the kind of event that the UN was hinting about, previously, as critical to the transformation of the global economy. All that is now required is for Germany to drop its dogmatic embrace of “Black Zero” fiscal policy and John Maynard Keynes will be smiling down from his exalted position in the firmament.

Big German historic moves have traditionally involved military adventure, in the quest for natural resources. The latest German move has a similar military vector.

We’ve been expecting you, Chancellor Scholz ….

Where Germany is successful, in helping other nations, it struggles to become a greater military presence in the global arena. This latter failure is not so much a case of embarrassment about its inglorious past militarism. Rather it is because the weak German coalition government cannot decide on how to spend its growing military budget. German fiscal Black Zero was helped, in no small way, by the country’s failure to meet its NATO threshold membership level military spending. Now, quite literally, German needs to embark on a deliberate policy of militarization, to meet global obligations and does not know where to start because there are so many military things to do.

A previous report discussed the awkward coming to terms with the need for militarization in Germany. The Germans appear to have swiftly gotten over their hang-ups. Perhaps this is because Russian forces appear to be consolidating their grip in East Ukraine.

The German coalition government recently achieved the required majority to exempt military spending from fiscal limits, in order, to make up for decades of underfunding. “Black Zero” was, thus, an artifact of military underfunding, to appease Russia and maintain the flow of Russian oil and gas.

The whole German economic and political policy mix has now changed irreversibly. Oil and gas are now expensive in real and fiscal terms for Germany. Perhaps, one day, German will decide, once again, that it is cheaper to acquire its raw materials and energy inputs by conquest. Who knows? But we should all care.

The return of German militarism appears to be moving in conjunction with the underlying strategy for deeper Eurozone political and economic integration. Germany is not creating a worrying domestic military-industrial complex again. On the contrary, Germany is promoting a Eurozone military-industrial complex, through mergers and acquisitions. Confluent with this strategy, Germany’s Rheinmetall is now building a non-aggressive minority stake in Italy’s cannon maker OTO Melara.

German militarism may not, necessarily, end in military expansion East. The Russian bridgehead in Eastern Ukraine appears to go accepted, rather than challenged, by the Western allies. There is a distinct sense of appeasement about this latest development.

The Three Slam Dunks ….

The general lack of enthusiasm, amongst the Western allies, to undermine the Russian bridgehead, in East Ukraine, suggests that the territory is a bargaining chip that will be negotiated away in the ultimate peace with honor settlement. This settlement must avoid the mistakes of Versailles, that the Western allies so deeply desire in order to pivot into confronting China. Ukraine is going to be partitioned. Russia is already issuing Russian passports for the Russian diaspora in East Ukraine. President Biden’s Slam Dunk is, also, in mid-air. The German Slam Dunk is also in mid-pivot.

Standing back, one can see three Slam Dunks. One Russian, one American, and one German.

Standing back, one can also see an own goal.

One Own Goal: A Penny for your Bushel of Gross Imperial Thoughts ….

The Danbury Mint’s Jubilee 50 pence coin’s deep 50% discount is allegorical. Inflation, it would seem, has eroded British patriotism’s purchasing power and inflated apathy’s unrealized capital gain.

UK Prime Minister Boris Johnson’s strategic misalignment with the New Multipolar World Order (NMWO) under construction, is finally getting the kind of editorial attention that can only mean one thing. This thing is regime change.

The last report discussed Britain’s loss of the Special Relationship, with the United States, in addition to its loss of any kind of relationship with the EU. These two strategic losses have been replaced with the nostalgic embrace of the Imperial connections from the past.

Just to emphasize the UK’s strategic reset, Prime Minister Johnson is promoting a return to the Imperial System of weights and measures. Presumably, this resonates with the pensioners who have not been decimated by COVID-19. Presumably, it also resonates with this year’s Jubilee theme and steals the Queen’s well-deserved valor to support the PM atop the shaky Greasy Pole.

· The UK will become an austere economy with an ungovernable polity.

Whilst the elected leadership degenerates, the growing political vacuum is filled with growing resentment and anarchy. Industrial unrest is flaring up, initially, in the case of the postal service, swiftly, then followed by the transport sector. If there was a coal industry, it would already be on strike!

No doubt, the Government’s response, to the industrial unrest, will be privatization of the sectors resisting. This will simply inflame matters and broaden the unrest, within the public sector, among workers who fear being privatized/downsized/rightsized/whatever.