Rational Exuberance: Mr. Market Re-correlates With @1990s

“The financial system is on the cusp of significant change. Central bank digital currencies (CBDCs) are central to this effort.” (Augustin Carstens)

Summary:

· The current China-US reset trades Chips for Fentanyl.

· Strictly speaking, it’s 2-1 for Xi Jinping because he bags Chips plus Taiwan goals.

· Strictly speaking, FAANG is the biggest winner of the Chips for Fentanyl reset.

· The Chips for Fentanyl reset is the supply-side basis of a soft landing in developed economies.

· UBS GWM Likes the KeySignals @1990s Thesis.

· The UBS GWM Worldview is “Macklem Doctrinaire” from the Supply Side upwards.

· Mr. Market’s conjoined twins of correlated equity, and bond market, returns have come full term.

· Mr. Market now fully accepts and leverages up, the managed FX regime thesis of apparent US Dollar strength.

· Mr. Market now fully accepts, and leverages up, the “No Plus in OPEC+” thesis.

· Strictly speaking, once again, in history, the US Baby Boomers are the biggest global winners before taxes and death.

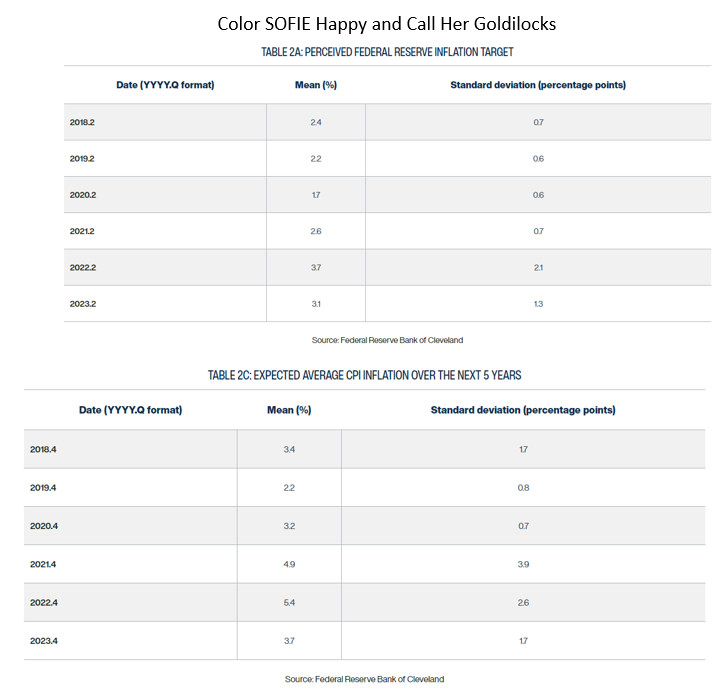

· Mr. Market is allowing the Fed to get away with an implicit higher short-term inflation target that is consistent with, a new definition of full employment and, lower long-term inflation expectations.

· APEC’s unfriendly shores raise the probability of an “Asian Debt Crisis rinse and repeat” along with regional risk premiums.

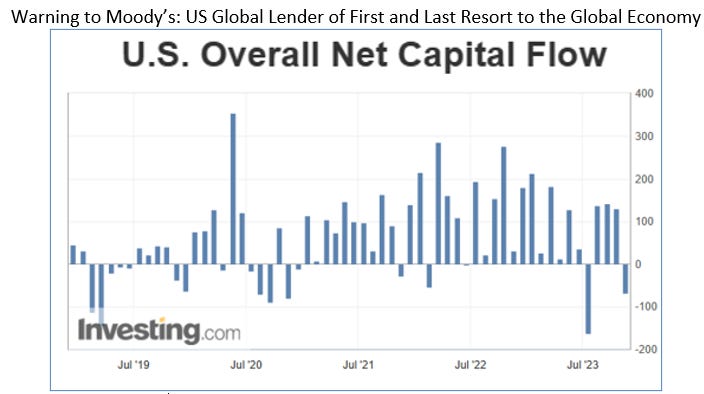

· Capital flow data, and the wars in Ukraine and Gaza, illustrate how the USA has become a global source of scarce/expensive reserve currency.

· The global demand for reserve currency requires the liquidation of US Treasuries at the same time as the Fed is liquidating its balance sheet.

· Global financial instability will prompt the Fed to reverse course and start providing scarce reserve currency more abundantly and cheaply.

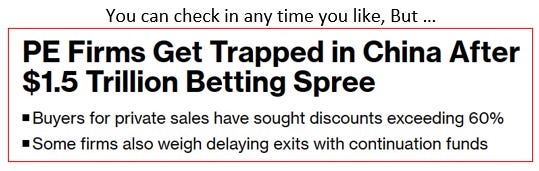

· The USA may be Unfinanceable, off the Fed Balance Sheet, but China has been downgraded, from Un-investable Grade to Un-exitable Grade.

· The process by which US fiscal deficits finance Chinese trade surpluses, which then finance US investment in China, is strategically broken.

· China is highly likely to be the trigger for an “Asian Debt Crisis rinse and repeat”.

· The recent USA and China downgrades are market-positive for Barbarous Relics and their contemporary Crypto-derivatives.

· The “Ungoverned Kingdom” (UK) reshuffles its pack of “Uninvestable” face card Jokers.

· The reshuffled UK pack of cards is a prelude to a split into two Right Hands that are larger than the current single one.

· The Orient Express VIP Lane is re-opened for business in the “Ungoverned Kingdom” (UK).

· The “Uninvestable Kingdom” (UK) surrenders to Fiscal, and Monetary Policy, Domination by the “Masters of the Asset Class Universe”.

· The Central Bank of the “Uninvestable Kingdom” (BOE) confirms that “Uninvestability” will manifest as financial instability in the NBFI sector.

· The RBNZ intends to meet an “Asian Debt Crisis rinse and repeat” with more reserves.

· The IMF decrees that digital currency debasement is consistent with its new global monetary policy frameworks edict.

Abstracts

· The 1990s global economic scenario is hiding in plain sight.

(Source: the Author)

· Incremental Ukrainian Anschluss, plus monetary policy tightening, equals global recession followed by Macklem Doctrine.

(Source: the Author)

· President Biden’s New World Order speech has revealed the 1990s global frame of reference for the perception of current global events.

· The promotion of global free trade, within the New World Order, is being used to stimulate disinflationary economic growth.

· The FOMC may be sacrificing its credibility, in order, to lower price inflation with higher market volatility.

· Aggressive monetary policy tightening may be a vanity project, in pursuit of lost credible commitment, that will undermine the Macklem Doctrine Solution for the New World Order.

· The ultimate New World Order, enabled by Macklem Doctrine, will have its own specific financial bubble in addition to “intransient” structural inflation.

(Source: the Author)

· Mr. (Bond)Market is giving the “@1990s” thesis the “Mother of All Likes” with a Yield Curve Bull-Steepener.

· Mr. (Bond)Market’s price action is consistent with a new definition of full employment.

· Mrs. (Equity) Market is estranged from Mr. (Bond) Market, but he is right.

· A happily consummated re-union, of Mr. and Mrs. Market, will give birth to strongly and healthy correlated bond and equity market children.

· He/She/They Gold has the correct global macro view.

(Source: the Author)

· “He/She/They Gold” is exclusively a central bank gender, with an exclusive agenda, that Mr. (Bond) Market and Mrs. (Equity) Market do not fully understand, yet.

· A happily consummated re-union, of Mr. (Bond) Market and Mrs. (Equity) Market, is beginning its correlated honeymoon period.

(Source: the Author)

· Chairman Powell informs Mr. Market that he has not price-discovered “Macklem Doctrine” by the desired process of a strong US Dollar, lower oil prices, and lower bond yields, as anticipated from the recent FOMC signaling.

· The broken FOMC signaling implies a loss of credible commitment and, thereby, greater risk to the desired Soft-Landing outcome.

· Extended OPEC/Russian production cuts have had the unintended effect of strengthening the US Exorbitant Privilege, and US economic relative outperformance/attractiveness which are discounted into the “Stronger for Longer” US Dollar.

· American “Swing Producer Status” is, effectively, “Texas Swing Producer Status”.

(Source: the Author)

· The BOJ upholds globally coordinated MMMT, which is predicated on a managed foreign exchange rate system that maintains the appearance of US Dollar strength.

(Source: the Author)

· Fed procrastination attempts to disguise the tactic of conflating an implicit higher inflation target, with an implicit lower unemployment target, because the latter is less damaging, for central banker credible commitment, under the current tightly-resourced economic circumstances.

· Fed procrastination nudges and frames a new definition of full employment.

· A new definition of full employment would soften the economic landing, of Jefferson’s Airplane, and normalize the yield curve.

· Fed procrastination is an abuse of Congressional dual mandate guidelines for, self-interested expediency and, politically motivated economic agency aka Friend-Shoring.

(Source: the Author)

· The Boston Fed has raised a glass, half-full, to toast the new definition of (half-)full employment, by facilitating thought leadership.

(Source: the Author)

· The IMF is preparing for an Asian Debt Crisis rinse and repeat.

(Source: the Author)

· The action of the Thai Central Bank is a global risk-off signal for non-developed economies asset prices.

(Source: the Author)

· The US Treasury’s “unanticipated” extra borrowing provides the real taxpayer-backed collateral to exchange with the QT loss-covering (“out of thin air”) assets on the Fed’s balance sheet that is consistent with the “Holistic” Fiscal Domination ex-post Sintra strategy of the US.

· Fitch correctly criticizes the process of “Holistic” Fiscal Domination but, incorrectly, fails to call out the Fed’s dubious laundering/layering process of exchanging real taxpayer-backed collateral with the QT loss-covering (“out of thin air”) assets on the Fed’s balance sheet.

· Fitch should in fact, downgrade the Fed and its performance to sub-investment grade status, and leave the US Federal Government credit rating at AAA.

(Source: the Author)

· The US Dollar transcends the “Uninvestable” Great Wall of China.

(Source: the Author)

· The Ungoverned Kingdom (UK) is “leaping” off the Great Wall of Worry onto the “uninvestable” side.

· Cleverly’s “stupidity” reprises the controversial UK Butler Model.

· The Butler is a Trojan Horse within G7.

· Cleverly’s “stupidity” risks transferring UK taxpayer revenues and intellectual property to China in addition to those being transferred to current “Friends-and-Family Shoring” recipients.

(Source: the Author)

· Since the systemically important, and insolvent, UK banks are effectively nationalized, the next financial crisis will hit the NBFIs.

· Deputy Hauser, of the insolvent Bank of England, is preparing the precedent for Modern Monetary Monopsony Theory (MMMT) to bail out the insolvent NBFIs.

(Source: the Author)