Regime Change(s) You Can Believe In

“A feat of daring can alter the whole conception of what is possible.” (Reprised by Christine Lagarde, originated by Graham Greene)

Summary:

· Ex post-ECB Governing Council meeting, the IMF has updated its plan for the Eurozone.

· The updated IMF plan frames the Ukraine war as the cause of “German Sickness”.

· The updated IMF plan frames the Ukraine war as the primary source of Eurozone Fragmentation Risk rather than the ECB’s actions and current divergent economic fundamentals at the national level.

· The updated IMF plan, thereby, frames the Ukraine war as the catalyst for Eurozone consolidation, initially in defensive terms, and, secondly, in expansionary terms to include Ukraine as a full Eurozone member.

· The Green Transition framed as Green Manumission (from Russian Oil & Gas) will start to dominate the Fiscal Submission in the IMF/ECB narrative for the Eurozone.

· Green Manumission is also a narrative through which to frame Eurozone consolidation, and expansion, in terms of Energy Independence, in order, to defeat Fragmentation.

· The Green Manumission structural tailwind can overcome the Brown Sectoral Bondage structural headwind, in a way that is consistent with Brimmer’s Law, if it is skilfully/geopolitically framed by the IMF/ECB.

· The halo of the “stagnating/stagflationary” flow, of commerce, through the Rhine artery, is being used as an allegorical factor in the “German Sickness” and the Green Solution diagnosis.

· Germany has traded the Brown Sectoral Bondage to Russian Oil & Gas for Brown Sectoral Bondage to domestic coal and wood rather than Green Manumission.

· The failure process, for President Macron, follows a pattern that implies agency and design.

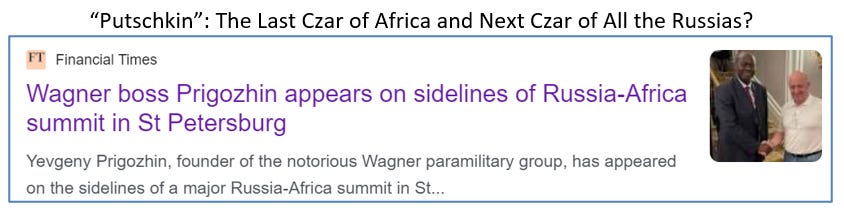

· Macron’s Dien Ben Fubar, in Niger, is a dish, best served cold, and cooked, in Wagner’s kitchen, by “Le Chef Putschkin” following “Joe Le Patsy’s” global recipe.

· The US Treasury’s “unanticipated” extra borrowing provides the real taxpayer-backed collateral to exchange with the QT loss-covering (“out of thin air”) assets on the Fed’s balance sheet that is consistent with the “Holistic” Fiscal Domination ex-post Sintra strategy of the US.

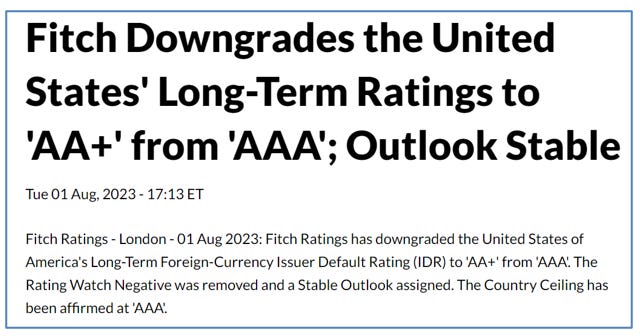

· Fitch correctly criticizes the process of “Holistic” Fiscal Domination but, incorrectly, fails to call out the Fed’s dubious laundering/layering process of exchanging real taxpayer-backed collateral with the QT loss-covering (“out of thin air”) assets on the Fed’s balance sheet.

· Fitch should in fact, downgrade the Fed and its performance to sub-investment grade status, and leave the US Federal Government credit rating at AAA.

· “Friends-and-Family Shoring” is the Ungoverned Kingdom’s (UK) Polycrisis strategy.

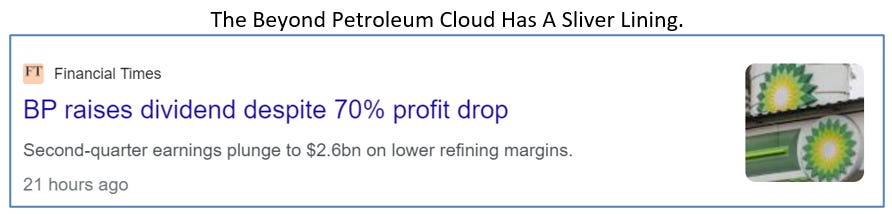

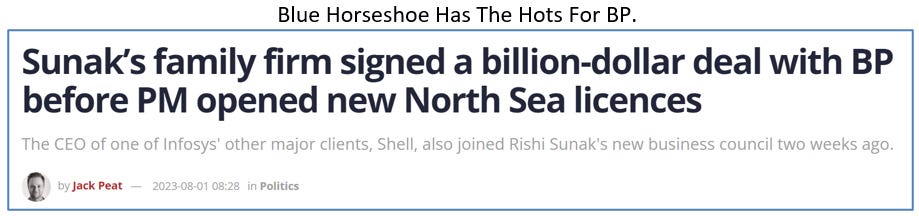

· Blue Horseshoe loves INFY, but he’s really got the hots for BP.

· Behind the next great fortune, in the Ungoverned Kingdom (UK), lie the lies about Energy Security.

· The Carbon Footprints in the Ungoverned Kingdom (UK) follow the VIP Lane, by way of a private jet, away from the Green Transition, to great fortune behind which lies the familiar/familial nepotism.

· Conflicted commercial and pecuniary extended family interest has been obscured behind a plausibly deniable cloud of Energy Security.

· The post-Ardern regime change in New Zealand sets the new global precedent for Inflationary Fiscal Dominance.

· Inflationary Fiscal Dominance recapitalizes the insolvent RBNZ with the inflationary proceeds of tax receipts from the central bank’s original QE process.

· There is no such thing as real economic growth in the Banana Republic of New Zealand.

· The RBNZ’s policy mandate is meaningless.

Extracts

· The planned “Great Consolidation”, around the stagnating/stagflationary Germanic Core, in the Eurozone, is unraveling to the point at which Grexit has become “Grescape”.

· Ex Post-Sintra, the Germanic Core Consumer is extending and pretending while the Peripheral Consumer has become Austerian.

(Source: the Author)

· Christine Lagarde has acknowledged that the swift loss of Euro strength has tipped the balance of risks towards Fragmentation over her desired Consolidation/Expansion outcome of the monetary policy tightening process.

· Lagarde dares, to win, by returning the ECB to solvency, while, simultaneously, enabling banking sector consolidation, and, avoiding Fragmentation, by scrapping the interest paid on reserves.

· In theory, a solvent ECB can evade Fragmentation by easing again once banking sector consolidation, during a period of economic weakness, has been achieved.

· At best, the Eurozone has a hard landing, with banking sector consolidation, and, at worst Fragments.

(Source: the Author)

· The IMF advocates saving the Euro, and the ECB, at the social cost of the European Project.

· Removing fiscal dominance requires the submission of governments, and the suppression of militant voters, to depressionary economic fundamentals.

· Populist demagoguery and large disenfranchised cohorts, of the Eurozone polity, will violently resist the IMF’s prescription and its agents.

(Source: the Author)

· Failure is an orphan, and so is Emmanuel Macron.

(Source: the Author)

· The ECB’s Sintra version, of Jackson Hole, may testify Brimmer’s Law.

(Source: the Author)

· Ex Post-Sintra, the Fed intends to interpret the IMF’s new monetary policy framework edict by sustaining Fiscal Dominance in pursuit of the Friend-Shoring imperative.

· Proposed higher Reserve Requirements must be balanced by a larger Fed balance sheet.

· A larger Fed balance sheet will provide the taxpayer-backed assets to “layer” with the lossmaking “out-of-thin-air assets” currently causing the central bank’s insolvency.

· A larger Fed balance sheet will provide the taxpayer-backed assets to “layer” with the lossmaking “out-of-thin-air assets” currently causing the central bank’s insolvency.

(Source: the Author)

· In the Polycrisis, Beyond COVID(BC2), there is Beyond Petroleum (BP).

· Thanks to the Ukraine War, Beyond Petroleum (BP) is now closer than you think.

(Source: the Author)