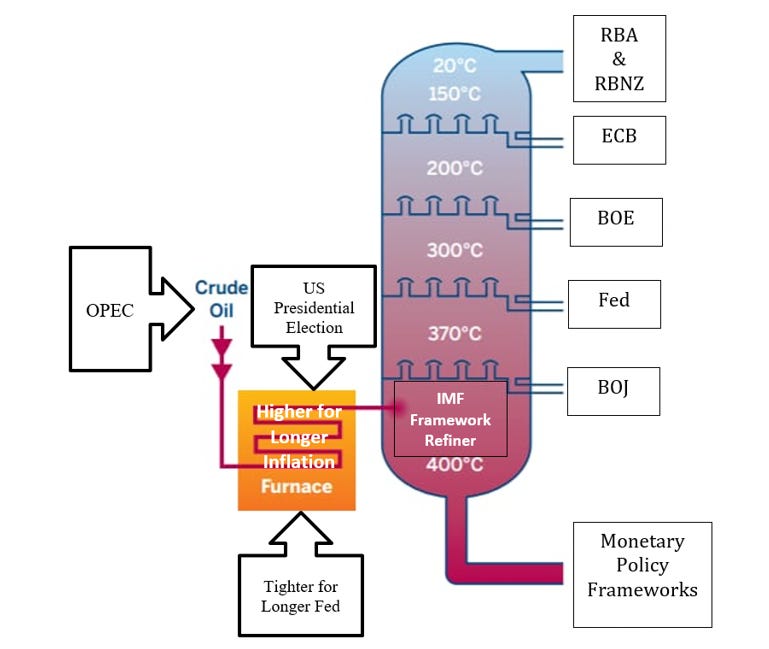

The Volatile Light Antipodean Fraction Separates First, From The Heavy Crude USA Fraction, In The IMF’s New Policy Framework Refinery Process

“We have to refine our monetary policy framework.” (Gita Gopinath)

Summary:

· The Sino-American Techno-Economic War, and the Friend-Shoring imperative, are catalysts for structural policy change in the Antipodes.

· The Antipodes cannot wait for the US Presidential Cycle and ‘Higher for Longer’ US inflation to run their respective courses before domestic/regional policies are enacted.

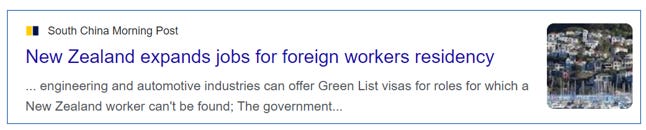

· The “Banana Republic of New Zealand (BRNZ)” is adopting immigration-driven supply-side stimulus policies.

· The Sino-American Techno-Economic War, and the Friend-Shoring imperative, mean that Australia is no longer the “Lucky Country” of perpetual structural economic growth.

· The combination of the US Presidential Cycle, and ‘Higher for Longer’ domestic inflation, have prevented the USA from leading the IMF’s new global economic/central banking framework directive from the front.

· The combination of global and domestic factors has prompted the Antipodes to take the IMF baton of global economic paradigm shifting from the USA in the developed economies.

· The Antipodean initiative follows the “Macklem Doctrine” supply-side directive.

· The “Stronger for Longer” US Dollar meme blows “Pseudo-Tightening” headwinds, through ASEA, to the Antipodes.

· After creating Alpha, Jamie Dimon asks investors to “Sikh Alpha” with him and his firm.

· The “Ungoverned Kingdom” (UK) has become statistically “Uninvestable” for the first time since 2011.

· The Broad Money Supply data in the “Ungoverned Kingdom” (UK) confirms “Un-investment”.

· Chairman Powell informs Mr. Market that he has not price-discovered “Macklem Doctrine” by the desired process of a strong US Dollar, lower oil prices, and lower bond yields, as anticipated from the recent FOMC signaling.

· The broken FOMC signaling implies a loss of credible commitment and, thereby, greater risk to the desired Soft-Landing outcome.

· Extended OPEC/Russian production cuts have had the unintended effect of strengthening the US Exorbitant Privilege, and US economic relative outperformance/attractiveness which are discounted into the “Stronger for Longer” US Dollar.

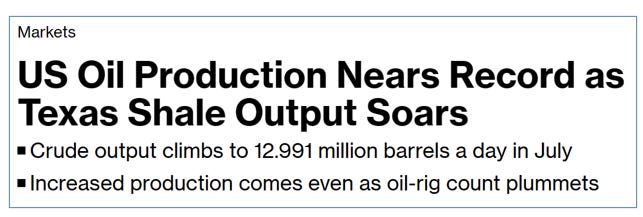

· American “Swing Producer Status” is, effectively, “Texas Swing Producer Status”.

Extracts

· The post-Ardern regime change in New Zealand sets the new global precedent for Inflationary Fiscal Dominance.

· Inflationary Fiscal Dominance recapitalizes the insolvent RBNZ with the inflationary proceeds of tax receipts from the central bank’s original QE process.

· There is no such thing as real economic growth in the Banana Republic of New Zealand.

· The RBNZ’s policy mandate is meaningless.

(Source: the Author)

· Classical “Brimmer’s Law” cannon is allegedly a new (post-Covid) supply-side inflation-driven ‘innovation’.

· The “Brimmer’s Law” ‘innovation’ frames supply-side inflation as a monetary policy tightening.

· The Fed’s supply-side innovation adheres to “Macklem Doctrine”.

· The Fed’s supply-side innovation leads to productive capital investment rather than inflationary consumption.

(Source: the Author)

· The “September Surprise” is happening.

· The “September Surprise” is US Dollar “Stronger for Longer”.

· The “September Surprise” triggers capital flight from what is perceived to be “Uninvestable” towards that which is “Shore-Friendly”.

· The surprised “Wave of Liquidity” will be a tailwind for “Hypergrowth”.

· A strong US Dollar mitigates the inflationary tailwind within the “Hypergrowth Phase”.

(Source: the Author)

· Post “G20 BRecCsit”, Jamie Dimon invites India to apply for G7 membership via his firm’s emerging global bond index.

· India responds to Dimon’s invitation by promising to be Basel III compliant by next year.

· India’s G7 emergence is challenged by its “Sikh and Destroy” human rights track record.

(Source: the Author)

· The Ungoverned Kingdom (UK) is “leaping” off the Great Wall of Worry onto the “uninvestable” side.

(Source: the Author)

· OPEC’s “ill-advised” response to the “Platts’ Brent Tweak” reinforces the doctrine and dogma of US Friend Shoring, whilst, strengthening and rewarding the Exorbitant Privilege.

· OPEC’s “ill-advised” response to the “Platts’ Brent Tweak” makes the US economy relatively stronger than its trade partners and adversaries.

· The USA has been afforded Swing Producer status, hence, the opportunity to influence short-term inflation expectations in addition to even greater influence over long-term inflation expectations.

· America now has the opportunity to exert greater influence on long-term inflation expectations, and energy security, on China’s front doorstep, in Asian Friend-Shoring supply chains.

(Source: the Author)