Dimon’s Hurrikraine Is The Global Blair Inc. Witch Project Tailwind

"If I practice politics (and economics) unethically, I will be unpleasant to the gods, and if I do it righteously, I will be unpleasant to the citizens." (Chrysippus, parenthesised by the Author)

Summary:

· The recent seclusion, in the refined mountain air, of Jackson Hole, would appear to have heightened some central bankers’ sense of independence to the rarefied heights of unaccountability.

· There are more Deformed Hedgehogs than Well-Informed Foxes, post Jackson Hole.

· Global aggregate demand is driving inflation not constrained supply.

· Federal subsidy and “Friend Shoring” private capital flows will create bubble valuations in the US “Hypergrowth Phase”.

· Speaker Pelosi’s Bottom is allegedly a “forgotten” US City where President Biden looks for votes.

· The Fed should not buy TIPS if it doesn’t want to be embarrassingly conflicted.

· Deep Throat says mind the Fed’s QT (Credible Commitment) Gap.

· The Quality and Quantity of Tightening are constrained by Esther George’s soliloquy.

· Chairman Powell successfully rebuts the assertion that the Fed’s two mandates are in conflict.

· Chairman Powell unsuccessfully smothers the Fed’s failed FAIT new monetary policy framework orphan.

· America maintains the home advantage to host the inaugural Indo-Pacific Economic Framework from a position of strategic strength.

· Germany initiates its own “Friend Shoring” process.

· Taiwan conflates Dope Inc. with the Bay of Pigs in a new series of Narcos.

· The BRICs have reached an internally conflicting and global disinflationary tipping point at which they turn from net energy importers to net energy re-exporters.

· To gain access to the US technology Crown Jewels, India must go through the Taiwanese “Friend Shoring” gatekeeper, thereby, putting itself into conflict with China.

· Russia is at the global strategic loss threshold despite Potemkin claims to the contrary.

· The BRICs tipping point is congruent with a new Ukraine “peace with honour” attempt.

· The Truss Family’s demise is contingent upon the US Mid Terms.

· Dimon’s Hurrikraine is also the (Tony) Blair Inc. Witch Project tailwind.

The Deformed Hedgehog and the Well-Informed Fox….

It is said that the debate in central banking is always between Hawks and Doves. This is incorrect. The debate is between Hedgehogs and Foxes. The Hedgehogs are also disfigured.

It is said that the Fox knows many things and the Hedgehog knows one big thing. It is also said that economists can procrastinate out of either hand. The current species of Jackson Hole 2022 central banker, with a couple of exceptions, seems to be a hybrid of these two aphorisms.

The Foundationalist versus the Coherent debate, over the truth about inflation, has momentarily been resolved by consensus rather than by data. The deformed Hedgehog has beaten the well-informed Fox. But the Fox is just pausing for breath and more information.

The global economy is at the point where deteriorating economic growth is in the baton-changing lane with inflation. Essentially, aggregate demand will become the driver of inflation, rather than constrained supply, going forward. This transition phase is complicated enough, without central banks sticking their own hands in. It should be allowed to occur naturally, but it won’t be because central bankers can’t control their helping hands.

Unfortunately, central bankers are always in a hurry to make things happen. They currently believe that inflation expectations are becoming unanchored, just as the global economy begins to drop the anchor and take expectations in the same direction.

Central bankers, excepting the BOJ, and Christine Lagarde, have come out of Jackson Hole, collectively, as Foundationalist, blinkered and, cognitively biased towards tightening, thereby, ignoring all Coherent evidence of economic weakness. They are in a hurry to kill the inflation that they unleashed, back in spring 2021, when they were equally and oppositely blinkered, and biased, towards promoting economic growth. The infamous two-handed economist is a one-eyed central banker, in practice. They are also in a hurry to prove that they are doing something, thereby, justifying their positions and their salaries.

Richmond Fed president Thomas Barkin is representative of the Deformed Hedgehogs crawling out of Jackson Hole. It must be said that, since he does not vote this year, Barkin’s extended forward guidance talk is cheaper than that of his FOMC voting colleagues. His guidance is, however, representative of the consensus and has the liberty to embellish it. Thus, Barkin has been keen to extemporize that he would move real rates, into the positive zone, and keep them there, indefinitely, until he became “convinced” that inflation expectations had structurally, and irreversibly, weakened.

Even less attention, than is afforded to Barkin, should be paid to Chicago Fed president Charles Evans. Evans doesn’t vote this year, and he is retiring soon. For anyone who cares, to listen to him, Evans doesn’t have a strong view on how much the FOMC should hike by, at the next meeting. Presumably, his indecisiveness is an attempt to give greater freedom to his colleagues who will be voting and, will have to live with the outcome of their votes.

Chairman Powell is, perhaps, the Alpha Male of Deformed Hedgehogs. Unflinchingly bespectacled, therefore myopic, rather than blind, Powell recently re-iterated his commitment, and that of his fellow Deformed Hedgehogs, to the one Big T’ing of beating inflation.

Similarly deformed, and no less meaningful, are the views of the lesser Alpha’s St. Louis Fed president James Bullard and Fed Governor Christopher Waller. Both are inelastically deformed towards a Big T’ing 75-Basis points rate hike, at the next FOMC meeting.

Apparently, this Big T’ing, is now, a “project” for Mandem, and Womandem, in the FOMC Crew, and not a Congressional requirement, of the Man. It is nice for a central banker to be able to pick and choose his projects, rather than have to follow what has been devolved to him/her by way of legitimacy. For pick and choose, think of stealing and getting away with it.

The recent seclusion, in the refined mountain air, of Jackson Hole, would appear to have heightened some central bankers’ sense of independence to the rarefied heights of unaccountability. The only way is down, for them, from here. One hopes that it will be a soft landing when it comes!

There is the consensus and, then, there is the reality.

Then, there is the fall.

Then, there is nothing but the gap.

Deep Throat says mind the QT Gap ….

The Fed’s credibility gap negatively correlates, strongly, with the size of the central bank’s balance sheet. An embarrassing example of this strongly negative correlation can be found in the Fed’s Treasury Inflation Protected Securities (TIPS) holdings. Because inflation has shot up, the value of these TIPS and, thereby, the associated space on the balance sheet have also shot up. Hence, the Fed cannot meet its target for balance sheet reduction.

If the Fed desires to shrink its balance sheet, it must, therefore, create a disinflationary recession. And thus, the Deformed Hedgehogs believe that the employment mandate must be ignored. It’s an act of self-preservation, in balance sheet terms, but self-destruction in employment mandate terms. Either the two mandates are conflicted, or the Fed needs to avoid buying TIPS if it doesn’t want to get embarrassed in the future.

· Monetary Policy tightening is ending because the Fed has reached the technical “unrealized” insolvency event horizon.

(Source: the Author)

The reality, for this author, is that the Fed has reached the technical “unrealized” insolvency event horizon. At this point, the unrealized losses on the Fed’s balance sheet, from the spike in bond yields, will oblige the Fed to ease monetary policy, in order, to move the balance sheet back into the black.

· The Fed’s self-embrace of financial stability policy is going ultra vires at the technical “unrealized” insolvency event horizon.

· MMT lurks beyond the Black Hole in the Fed’s balance sheet.

(Source: the Author)

A leaky Fed source, appropriately named Fed Guy, recently tried to explain how the central bank would deploy a form of basic accounting fraud, in order to, create “deferred assets out of thin air” to, cover the unrealized losses.

The author then described the magic trick, of accounting fraud, whereby, these “deferred out of thin air assets” would be marked-to-market, with an unrealized gain, by nature of an inverted yield curve.

This illusion is, however, ephemeral. The logistic problem, with this form of fraud, is that the “out of thin air assets” must be replaced, with real cash-flow backed assets, to make up for the missing “out of thin air” cash flows.

In addition, the “out of thin air assets” lose their value, over time, because they are converging, backward, up an inverted yield curve, toward today’s valuation date. This convergence could be viewed as Yield Curve Backwardation. This form of backwardation is exactly why the Fed’s balance sheet, currently, has unrealized losses that need covering. The profit associated with the “out of thin air assets”, thus, converges backward, to a market-to-market loss, in addition to there being no real cash flows to sustain any real net present valuation of them. Hence, the Fed is, in practice, covering an unrealized loss with an “out of thin air unrealized loss”. This is about as unsustainable as the accounting fraud gets, in central banking, until the central bank U-turns and the fiscal authorities come up with some real cash-flow assets for the balance sheet.

The only long-term solution is for the Fed to buy replacement US Treasuries, and to cut interest rates, to put the balance sheet back into profit, on the asset side, so that the real economy can be stimulated with reserve creation on the liability side of the balance sheet. These are difficult things to do when inflation is way above target. The smoke is less opaque and the mirrors are less shiny when the prestige of monetary policy easing is delivered before inflation has been fully made to disappear.

Fed Guy has recently been crossing the wires, again, explaining how the unavoidable, and embarrassing, Fed easing can be avoided. This evasion requires the US commercial banks to play ball. The whole point of the matter is that the banks aren’t playing ball right now. The banks are preparing for the inevitable economic contraction, inflationary and/or disinflationary, that will require a monetary and fiscal policy stimulus.

According to Fed Guy, the converse side of the Fed’s balance sheet, that is liabilities, in the form of bank reserves, is apparently shrinking at such a rate as to trigger the Fed’s worry about economic growth. The commercial banks have no need for reserves since they are shrinking their own lending books, in line with an expected economic contraction.

Since credit creation is a private function, in the US, the Fed cannot influence the banks’ lending behavior. Thus, once again, as always, the banks are staring down the Fed and daring the central bank to tighten. Soon, once again, the same banks will be daring the Fed to ease again.

Given the failure of Fed Guy, the New York Fed has attempted to address the balance sheet issue directly. The unenviable task has fallen to Pro Tempore System Open Market Account Manager Patricia Zobel.

Zobel does not have a full-time job, of balance sheet management, at the Fed yet. Her presumption of full-time, gainful, employment shrinking the Fed’s balance sheet does not appear to be a strong one either.

Zobel has basically confirmed the leak from Fed Guy, thereby establishing his credibility as a source. This did not, however, give credibility to the message from either source.

Fed Guy’s case for the commercial banks to actively engage in replacing their massive holdings of Fed reserve liabilities, in the form of US Treasury security collateral financing agreements, known as Reverse Repos (RRPs), with real US Treasury Bills was reiterated by Sobel.

As already stated, the commercial banks aren’t playing ball. They are preparing for an economic contraction, which basically means that Zobel if she gets the job, will be engaged in expanding the Fed’s balance sheet rather than shrinking it. When the commercial banks smell rate cuts and Fed balance sheet expansion, they will then buy US Treasury Securities, themselves, in addition to expanding bank reserves.

This author wishes Zobel well in her full-time employment quest at the New York Fed. He also wishes her well, for balance sheet expansion, if and when she gets the full-time position.

As the balance of risks tips growth into a higher priority ranking than above-target inflation, the Fed will have to ease, prematurely, before it can claim victory over inflation.

· Loretta Mester’s deliberate ignoring of the employment mandate is professional misconduct, on a par with her previous “broadly inclusive” failure to follow the inflation mandate, rather than a form of clear extended forward guidance.

(Source: the Author)

This author would remind the reader of the opprobrium for Cleveland President Loretta Mester, in the last report, for her totally dropping the Congressional Employment Mandate from her watch.

· Neel “Ex Culpa” Kashkari’s sadistic pleasure in poor Fed communication policy weakens the central bank’s credible commitment even further.

(Source: the Author)

Similarly, the reader should be reminded of the “binary” jerking about by Minneapolis Fed president Neel “Ex Culpa” Kashkari as he overplays the Hawk burlesque.

Chairman Powell also appeared to respond directly to the criticism, leveled by this author, that the Fed is unprofessionally ignoring its employment mandate because it is in conflict with the current course of action. According to Powell’s assumed rebuttal "in particular in the current moment, I (Powell) don't see the two goals as in conflict at all because, without price stability, we will not be able to achieve the kind of strong labor market that we want for a sustained period that benefits all, so I don't see a case for moving to a single mandate."

· Chairman Powell confirms the thesis that monetary policy will be framed as creating a disinflationary base for the Biden “Slam Dunk”.

(Source: the Author)

So, in fact, Chapeau to Chairman Powell for re-confirming, for a second time, the author’s thesis that the Fed is pretending to create a disinflationary base upon which a strong economic expansion is grounded.

· The most notable thing about this year’s Jackson Hole symposium was the complete sweeping under the carpet of the issue of the Fed’s, too successful, flexible average inflation targeting (FAIT), monetary policymaking framework.

(Source: the Author)

This author welcomes Powell’s rebuttals and now asks the Fed Chairman to rebut the author’s claim that the Fed’s flexible average inflation targeting (FAIT) “orphan” has been smothered.

Coming out of Jackson Hole, there is tangible evidence that the Deformed Hedgehogs are headed for extinction. As usual, it is the Fed’s Beige Book that is the most accurate guide to the state of the domestic economy. The latest readings are that growth and inflation are cooling. The inflation cooling trajectory may not, however, satisfy the FOMC. The Chicago and Philly Fed actually saw recession conditions precedent, so the FOMC is going to have to be nimble. The guidance, at Jackson Hole, was anything but nimble. Since then, however, there has been some modulation to the tone of guidance.

Coming out of Jackson Hole, some FOMC speakers were treading dangerously close to an inflation obsession that totally ignores their employment mandate obligation. Perhaps this was just a dramatic license to emphasize their message. They may consider their job was done by muscling Mr. Market into radically scaling back his easing predictions for 2023 post-Jackson Hole. They were reminded, and warned, about their transgression by their hostess-with-the-mostest credibility.

The Quality and Quantity of Tightening are Constrained ….

· Esther George’s sound monetary policy compass will be sorely missed when she retires.

(Source: the Author)

Kansas City Fed president Esther George continues to be the biggest Alpha Vixen, of central bankers, in the Deformed Hedgehog milieu.

In a recent post-Jackson Hole speech, George reminded her errant, and aberrant, colleagues that the symposium she hosted, the week before, was all about “Constraints”. These real economic “Constraints” should be understood and factored-into policymaking decisions going forward. Evidently, they have been forgotten and/or overlooked.

For “Constraints”, one should subliminally read dual mandate obligations. Coincidentally, and auspiciously, the OECD has recently reported that the global job market is losing momentum despite rising wage pressures. Evidently, George has kept her dual mandate head whilst those around her have lost theirs. Those who have lost their heads, forecasting the terminal rate, were gently reminded, by her, of their previous mistakes in forecasting other targets which became meaningless in the constrained reality.

George cautioned that the real economic “Constraints” not only constrain the scope for interest rate hikes but also balance sheet reduction.

Evidently, the Deformed Hedgehogs, whom George must suffer, for a little while longer, have swiftly forgotten what the Jackson Hole symposium was all about. George reminded them with a dual-entendre, that belied their dual mandate obligations. It was yet another master class, that sailed way over the limitations of her FOMC colleagues.

The quality of George’s mercy is not strained and will be sadly missed when she departs.

“We can’t allow fundamental decisions to be taken by a large male majority; that is simply not on.” (Christine Lagarde)

Fortunately, there are some potential Alpha Vixen Cubs, on the FOMC, who can take up the baton when George takes a well-earned retirement.

If you liked it then you shoulda put a pearl on it ….

Christine Lagarde will not be the only Alpha Vixen in the global central banking pack when Esther George retires.

Since the Jackson Hole hysteria, Loretta Mester has retraced her steps toward the employment mandate. Lately, she has acknowledged that the US economy is slowing but inflation is still not slowing, fast enough, for her to change her tightening bias.

Fed Vice Chair Lael Brainard appears to be, belatedly, coming to her senses also. Her full recovery may, however, be too late. Brainard acknowledges that the US economy is slowing, under the headwind of inflation, and the headwind of Fed tightening. She also admits that price-gougers have much to answer for about inflated prices. All the inflation drivers, that she can see, are waning. Sadly, she is unwilling to hazard an opinion about when inflation will fall back into her comfort zone.

One should not be too hard on incoming Boston Fed president Susan Collins. She comes into a central bank that had lost the plot, on inflation, way back in March 2021. Now it is losing the plot on economic growth, deliberately, to overcompensate for its inflation mess up. Collins has, thus, already, been set up to have a career of failure as an FOMC member. The question, now, is just how much she fails.

Collins’ first interview, in her new role, set out in line with her reputational damage limitation priority. All that she would say, initially, was that she has not yet seen a significant inflation decline. She would not say what she thinks about the deceleration in economic growth. Clearly, inflation is still her priority.

None of the Deformed Hedgehogs and Well-Informed Foxes, so far, have been brave enough to discuss the fate of the elephant in Jackson Hole.

Success has many fathers, and mothers, failure is a bastard ….

· The most notable thing about this year’s Jackson Hole symposium was the complete sweeping under the carpet of the issue of the Fed’s, too successful, flexible average inflation targeting (FAIT), monetary policymaking framework.

(Source: the Author)

The author noted that the Fed eschewed all praise for over-achieving on its flexible average inflation targeting new monetary policy framework at Jackson Hole. In fact, the whole issue was conveniently dropped. Any attention to the matter, and the current inflation rate, would have resulted in further erosion of the Fed’s credibility.

The deficit, in Fed credibility, is about to hit new all-time highs as the Hawkish zeal for QT recedes and the balance-sheet loss-enforced Dovish zeal for QE returns. How much credibility is lost will depend on how far inflation is, above target, when the costume switch occurs.

· The Macklem Doctrine of America’s global imperative may make bigger fools out of the FOMC than the incoming inflation data.

(Source: the Author)

The deficit in Fed credibility will also depend on how much of the new Biden fiscal deficit ends up on the central bank’s balance sheet. POTUS is in a hurry to stack up the next $Trillion in balance sheet assets.

Fighting Talk: Fab-Ready, is the new Shovel-Ready ….

The White House has recently given notice on how the “Friend Shoring” component of the Chips Act will be spent. This spending is a direct subsidy to chip manufacturers who globally relocate back to the US.

· The US “Friend Shoring” valve has tightened from the global singularity to the global economy destructive “Death Star” level.

(Source: the Author)

Ostensibly, this is a declaration of intentions and capabilities to prosecute a “Techno-Economic War” indiscriminately on friends and foes alike. America is making no distinctions, about, whom it attacks as it seeks to win the “Techno-Economic War”.

The White House has also given notice that its support for the technology sector, by Federal subsidy, is a direct economic transfer of wealth from the taxpayer to the technologist. This author would remind readers of the bubbles that have, previously, occurred when the Federal Government chooses economic winners. Think of Big Oil and its Federal subsidies. Also, think of the subsidies to the GFCs when housing was the chosen winner. Think of the COVID response, if you’re not old enough to remember the other two. Then think of the booms, and busts, which always come with these fiscal junkets. This is the beginning of the next boom.

The way that Treasury Secretary Yellen is framing the next combined monetary and fiscal policy junket belies the scale and the location of the impact. Yellen would have Americans believe that this time it’s different. The Biden stimulus will, allegedly, be “pro-growth and pro-fairness”. POTUS would certainly like voters to believe, as evidenced by his recent appearance at a new Intel (INTC) chip fabricating location in Ohio.

There didn’t seem to be much “pro-fairness” in the COVID-19 stimulus, which ran to $Trillions. Why would it be any different this time? Ohioans and voters, in general, are rightly skeptical.

The stimulus certainly looks pro-Intel stock!

It also looks pro - “Speaker Pelosi’s Bottom”!

Speaker Pelosi “loves” Microsoft and Apple call options. Madam Speaker’s recent eyebrow-raising leveraged bottom fishing has raised more than a few eyebrows.

(Source: the Author)

In fact, this time, the stimulus looks decidedly focused on capital formation rather than job creation per se. The current focus of the stimulus, through the prism of “Speaker Pelosi’s Bottom”, is perhaps the best indicator of whom the ultimate beneficiaries of this “pro-growth/fairness” stimulus will be. The perceived outcome looks more pro-growth stock than fair. Nothing seems to have changed, much, in the distributional effect of this stimulus, from all those that have gone before, probably, with the exception of Roosevelt’s New Deal.

· The Fed’s financial stability policy imperative supports the great balance sheet “Friend Shoring” rotation thesis, from demand side to supply side balance sheet assets.

· In essence, supply-side growth stimulus is the whole objective of central bank financial stability policy, pretending to be monetary policy, going forwards.

· Don’t fight the Fed’s great balance sheet rotation, track it with a “Hypergrowth Phase” demand-side to supply-side portfolio rotation instead.

(Source: the Author)

The supply-side “Hypergrowth Phase”, that this author envisages, will be subsidized by the Federal Government. Doubtless, the fiscal deficit created will be warehoused on the Fed’s balance sheet because the Federal Government is afraid to lose votes by foisting it off onto the US taxpayer.

The US “Hypergrowth Phase”, however, does not need subsidizing. Private American investors who have prospered on the way up, to this Thucydides Trap confrontation point, with China, and may even have financed it, are now reversing their capital flows to align with the “Friend Shoring” tide’s fundamentals. Consequently, the US “Hypergrowth Phase” will be turbo-charged by the confluence of fiscal subsidy and private capital. The bubble in asset valuations will, hence, be astronomical, also, for this reason.

Despite all the setbacks, least of all the Fed’s dismal inflation performance, US policymakers have been able to maintain the initiative, and momentum, which put them in a position of, home advantage, to host the inaugural gathering of the Indo-Pacific Economic Framework (IPEF). This is no mean feat. Asian attendees must now pay tribute, to their host, and respect his ability, to crush their economies, in addition to his ability to pulverize their armed forces. This is what being a superpower should look like. Other alleged superpowers don’t look anywhere near as powerful, in comparison.

There is one eternal smile, that never goes away, much to the Fed Chairman’s chagrin. This smile has broadened, into the familiar smirk, of late.

(Source: the Author)

Never one to miss an opportunity, for self-aggrandizement, Larry Summers was on hand to steal some valor from successful economic policymaking of which he has been a critic.

According to Summers, the all-conquering US economy and its currency can thoroughly vanquish its global foes.

American timing is impeccable. It coincides with, and therefore challenges, the political center of gravity of a reciprocal move by China to enshrine “Xi Jinping Thought” as the only thought in Chinese hearts and minds.

Just as America was tightening the screw, on China, Germany gave it a few more turns. The Germans have, recently, let it be known that they intend to deploy their own specific form of “Friend Shoring” to the exclusion of commerce and investment flows with China.

Somewhat overwhelmed, China is responding globally after Xi Jinping talks locally.

Crouching (Operation) Mongoose, Unhidden Dragon, Snorting (Bay of) Pigs ….

Those still unpersuaded, by this author’s Bay of Pigs analogy, may wish to read, and watch, the recently released Bloomberg version of events; and note the timing of this story as well as the headline. The Bloomberg editorial headline is that China is winning in South America. This journalistic source and view are guaranteed to provoke a response in Washington.

(Source: the Author)

This author suspects that the wily President Xi Jinping will hit America, in its backyard, thereby reciprocating the perceived Taiwan insult in kind. This Bay of Pigs moment would then strengthen the American resolve and strategy to stay in the game.

(Source: the Author)

This author’s Bay of Pigs moment reprise appears to be unfolding in slow motion.

The American thirty-year narrative involves the funding and creation of a bipartisan consensus from the perceived Chinese threat via Latin America.

(Source: the Author)

This reprise is part of a much larger thesis, in which a bipartisan consensus to respond to Chinese encroachment in America’s Latin American continental backyard is finally achieved. This regional consensus is part of a much broader global consensus to knock China off its perch.

Taiwan is, clearly, at the heart of the US global strategy. Taiwanese Vice Foreign Minister Alexander Yui recently informed the world that China is seeking to build a “naval outpost” in Nicaragua.

This author was, a little, surprised to find that Taiwan is also at the heart of the Latin America strategy. This admitted surprise comes at the lack of subtlety displayed in trying to conceal American intentions and capabilities. Evidently, the point has been reached at which America is going all in. There is, thus, no requirement for stealth and guile. What’s required now are noisy attention-grabbing headlines, editorials, and speeches in Washington.

75% of Americans don’t have a passport, and most Americans couldn’t give a monkey’s about the rest of the world. 100% of Americans know all about drugs and violence, though. So, sell ’em a global riddle, inside crime mystery, clothed in an enigmatic Narco Baron and they will buy it. And thus, President Xi Jinping becomes Don Xi, the Belt and Road become Dope Inc. and China becomes a Cartel rather than a nation. The fact that there is a strong element of truth in all these generalizations makes the story even more credible.

· NAFTA has effectively been re-positioned, by China, as a Belt and Road narcotics free trade zone.

· A Reverse Opium War chapter has been added to the “Techno-Economic War” chapter in the American thirty-year narrative of the funding and creation of a bipartisan consensus from the perceived Chinese threat via Latin America.

· China’s Belt and Road initiative may soon be officially designated Dope Inc. headquartered in Hong Kong.

(Source: the Author)

There is nothing noisier than the global fixation with Narco-Barons. Hence, this author assumes that the recent framing of China’s Belt and Road as a vertically integrated narcotics enterprise, subverting NAFTA out of Mexico, is the expected noisy attention-grabbing process in operation.

Throw the Chinese bases in Nicaragua into the plot and all that is missing is Bob DeNiro to direct and star in the screenplay!

The Russians, as always, also, get thrown into the mix.

Margin call ….

· Disinflation price discovery by Cancel Culture is on the global commodity and capital markets agenda.

(Source: the Author)

This author has been expecting a more ruthless form of Cancel Culture, directed at speculators who have no intention of taking long commodity futures contract positions to delivery.

Allegedly, the EU is now considering canceling the trades in energy derivatives for leveraged speculative longs that are not based on industrial risk positions that need hedging. The unwinding of such speculative positions would be seriously disinflationary, not-to-say a trigger for a financial crisis.

Rather than cancel the trades, this author recommends that margin requirements should be raised to astronomic levels for leveraged speculators. Thus, there would be no need for the central banks to raise these margin requirements indirectly, and indiscriminately, with high interest rates, which kill the real economy, along with the speculative longs, in the process. Let’s see if common sense prevails.

The EU, and other developed market energy net-importers, will be relieved that their Cancel Culture, in relation to energy prices, is being reciprocated with alacrity by the BRICs (ex-Russia). Indeed, the BRICs have reached a tipping point at which each member must decide where its true economic future lies. This consideration may put membership of the bloc at risk.

Joe Sixpack, and Blue Horseshoe, love papadoms with their turkey ….

The unity of purpose, of the BRICs, to gain strategic parity with the developed world has become a victim of its own success. Stagflation in the developed economies has seriously weakened the export component of all the BRIC economies.

This faltering exponent feature has led China, and India, to beggar thy neighboring Russia by appearing to support its war in Ukraine, in return for cheap oil and gas which the two then re-export to the global economy. Whilst pretending to stand by Russia, in exchange for cheap energy imports, the two are, therefore, undermining President Putin’s war effort.

Western commentators are keen to stir the BRIC pot, even harder, to then make India fall out with China. It is divide and conquer at its most creative.

· Rumour has it that Blue Horseshoe loves papadoms, so India should be worried.

(Source: the Author)

The carrot and stick strategy, being deployed by America, to prize India out of the BRICs is gaining visibility in economic data. India is now in the top-five suppliers of American Christmas items. India’s economic gain is China’s economic loss.

Low-value goods trade is good for starters, but Indian Finance Minister Nirmala Sitharaman wants Americans to invest in high-tech Indian companies who wish to, ultimately, compete with and put their US peers out of business. All well and good Madam Nirmala, so far, but there is a political quid pro quo. To gain access, to the US technology jewels, India must go through the Taiwanese “Friend Shoring” gatekeeper, thereby, putting itself into conflict with China. There is no free Big Mac, Madam Nirmala.

Sitharaman cannot have failed to have noticed the massive wealth transfer, from US taxpayer to US technologist, recently announced by the White House. Evidently, she wouldn’t mind trying to jib some US taxpayer funds for her own economy. She should call Rishi Sunak, on this one. He is out of work and currently reconsidering his Green Card application status. His track record in jibbing UK taxpayer funds for Indian technology companies is also second to none.

India has shown that it will not easily be bought off with American largesse or threatened by American military muscle.

At the last minute, India opted out of trade talks in America’s inaugural Indo-Pacific summit. This may be a sign of innate protectionism. It may also be a sign of loyalty to the BRIC cause. Further probing of the causation will, thus, be applied by those with a strategic interest in the answer.

· India has been offered the choice of becoming a player, or a battlefield, in the Sino-American “Techno-Economic War” with the “Triad’s” live sales-demo in Afghanistan.

(Source: the Author)

Because of American overtures, and destruction of the global economy, with high interest rates and a strong Us Dollar, China and India now find themselves being nudged into conflict, with each other, born out of their necessity for survival in a global economy that they initially tried to undermine as BRIC allies. The two nations have tried to avoid conflict with each other, even going as far as to de-militarize their contested Himalayan border. The pressure to make them conflict will, hence, be turned up by those with an interest in the conflict.

As stated, Russia is also in the conflict mix.

Would you like some Russian contraband with your Dope?

· Meaningless high spot commodity prices on screens are the reference point for meaningful discounts in the “constrained” physical markets.

(Source: the Author)

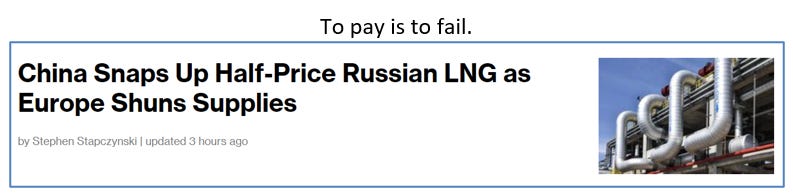

China’s Belt and Road is not only configured for the narcotics trade, as alleged, it is also configured for the hydrocarbons trade as acknowledged fact. Thus, the Chinese energy giants of CNOOC, SINOPEC, and PetroChina now find themselves re-exporting Russian hydrocarbons for which the US-embargoed and the COVID-Zeroed Chinese domestic economy have no uses.

· China is weaponizing its petroleum sector in the same way that Russia is.

(Source: the Author)

The tipping point in the Indian and Chinese BRIC economies, which pivots them from net energy importers to re-exporters, is a major turning point for the global economy. This tipping point is disinflationary. Even Turkey is getting in on the action.

· G7 can now, with justification, claim that China is a combatant in the Ukraine war, and then go on to ratchet up political and economic sanctions proportionately.

(Source: the Author)

Russian energy minister Nikolai Shulginov has announced that Russian hydrocarbons will be directed to Asia from Europe going forward. He has failed to note that Asia doesn’t have use for them. Gazprom, the state within the State, has already adjusted its business model to the new competitive fundamentals. Gas that would have been destined for the EU is now being bottled and sold as LNG. Russian gas, will, thus, find its way back to the EU via a myriad of Asian middlemen, some of them in India and China. Ostensibly, this is Shell’s business model. This is also disinflationary, with a time lag.

Russia’s bet on Asia was, finally, confirmed by a speech from President Putin geo-symbolically delivered in Vladivostok. In the speech, the West was berated for giving Russia no choice other than to, go East and, weaken the global economy in the meantime. This was clearly a thinly veiled swipe at President Macron, and Angela Merkel, for moving closer to Russia only then to abandon it. The penalty for this action is higher gas prices and economic revenge. This revenge will also include starving the West, as well as freezing it, by withholding Ukrainian grain exports and redirecting them to friends. Apparently, Russia has been given no choice other than to make Asia a friend who will become stronger than the West. It was all very exculpatory and plaintiff. Rather like a Catholic confession, except that Putin is Orthodox. Gone was all the trademark bellicose confidence and aggression.

To this author, President Putin also looked and sounded like someone who was threatening to commit suicide unless he was taken seriously. A kind of take me seriously or else I’m jumping off the ledge speech.

The suicide in betting on Asia is evident.

As Russia bets on Asia, Asia may be abandoning this Russian misplaced faith. Previously, this author noted that China was being framed as a combatant in Ukraine. Apparently, China wishes to get out of this frame, so to speak.

China’s new approach to Russia is not just limited to jibbing, and then jobbing, its ally’s hydrocarbon base. China is showing tangible signs of indirectly abandoning its ally on the battlefield in Ukraine.

· In view of the fact that there are now two Ukraines, the “Sanatorium Exit Strategy” will need to be tweaked.

(Source: the Author)

Western observers have observed the recent nuanced change within the BRICs. The strategy of divide and conquer may, thus, prove to be the acme of skill for the observers with axes to grind. There will be a price to pay for this changed nuance, however. Prices like this are usually paid by the small countries that are pawns in the big game being played. Thus far, it appears that this price will be paid by the Ukrainians. One of those peace with honor, appeasement, moves so popular in European history may be under construction. The “Sanatorium Exit Strategy”, that this author suggested needed tweaking, now appears to be being tweaked.

Consistent with the cut and thrust, of diplomacy, and haggling over gas prices, the much-heralded Ukraine counterattack has been a subdued event. Despite that, Russia is giving ground in all but areas directly adjacent to its borders with Ukraine. Political negotiating imperatives require the counterattack to be an irritant rather than a full-scale eviction of Russian forces. According to Von Clausewitz, war is politics by another means. In this case, however, politics is economics by another means. Hence, the counterattack is constrained by economic rather than military and logistic calculus. The current objective is to make Russia sell gas to Europe rather than leave Ukraine. Vae victis!

Those watching the recent, failed, OPEC+ attempt to arrest the decline in crude prices will have noted that global aggregate demand is now more important than supply in determining prices. They may also have observed that Russia was the main standout arguing against output cuts. This objection belies a tipping point, in the Russian economy.

Divide and Conquer: There’s no R in BICs, in fact, there’s no BRICs ….

There are no secrets in Russia, despite all the stern Slavic faces that pretend otherwise. Everything in Russia is for sale, at a price. A recently classified document illustrates both of these assertions.

A not-secret secret Russian government document has painted the Potemkin façade of an economy that is not walking President Putin’s tough talk. Time is not Russia’s ally, and neither are its BRIC allies.

Russia is experiencing a drain on its human and economic resources that will take generations to repair, even if arrested now. If these drains continue, the country will cease to function normally. The threat is existential. The integrity of the nation is now at risk. Even if it wins in Ukraine, which is unlikely, the strategic cost is a strategic global loss.

The rationale for continuing to fight is non-existent, hence its continuation can only be about the personal survival of a few. The specter of Hitler’s Bunker looms. The Russian few, in any case, have never fared well, at the hands of the majority, once the majority turns.

The said Russian majority is currently migrating, rather than regime-changing. This demographic fact leaves the minority in control of something that it cannot control in practice without majority cooperation. Coercion will only go so far in an economy that intends to modernize.

Russia, therefore, needs to maximize its export revenues. Since global hydrocarbon demand is now driving the price, rather than supply, Russia must expand its hydrocarbon export volume to maximize revenues.

Secretary Yellen’s nuncio to Europe, Wally Adeyemo is eager to give credence to the gloomy not-secret secret Russian report of economic doom and gloom. This eagerness betrays a willingness of America to conclude a peace settlement, in Ukraine, in order to focus on China.

America is also eager to conclude operations in Europe by settling the UK problem.

He’s Creepy and She’s Kooky ….

The Special Relationship has reached a new milestone with the arrival of the new UK PM on the Trans-Atlantic dating website. Hitherto, this author had observed some prerequisites for a happy marriage.

· The rekindling of the symbiotic Special Relationship is pending the tall New World Order of the permanent sacking/resignation of the Butler, the conviction of the Oxford Apostles, the UK re-joining the EU, the closure of the VIP Lane, and India leaving the BRICs.

· The rekindling of the symbiotic Special Relationship is also pending the syncretic bicameral Anglo-Saxon political cleansing simultaneously occurring on either side of the Atlantic.

(Source: the Author)

These strategic prerequisites involved some reformed behavior by both suitors. Britain would have to ditch Johnsonian Sleasez Faire and America would have to become Progressive.

Little progress appears to have been made on either side of the Atlantic. America is still rabidly partisan and Britain has elected for Sleasez Faire Lite. Both partners, in the Special Relationship, thus, remain ideological opposites.

They say opposites attract.

But then, they also say keep your friends close and your enemies even closer.

Sadly, the new UK PM is a chip off the old Boris Block, so the new relationship will get off to a rocky start. Fortunately, the new UK PM also fancies herself as a chip off the old Thatcher Block so there is scope for the Special Relationship to prosper in the realm of foreign policy. Truss is apparently tougher on China than Boris, so this stands Britain in good stead. This prosperity, however, hinges on a mutually beneficial Brexit outcome. Brexit is an Achilles Heel for Truss’s conflicted Tory stiletto heels which may topple her ultimately.

Austerity is, clearly, evident in the latest UK insolvency statistics. Company and individual insolvencies are accelerating. The economic threat to the Union is clear, as companies and individuals go under in Northern Ireland and Scotland. Regional populists will claim that they have been abandoned by London. Nicola Sturgeon will be gleefully watching the carnage, whilst Sinn Fein will be preparing the economic case for a Republic. The PM’s recent jaunt to India and the announcement that potential new UK IT jobs will be diverted, from the provinces to the Subcontinent, is just another nail in the coffin.

(Source: the Author)

Some believe that President Biden’s mother was a Fenian and that her son passionately believes that Ireland can (and will) be a nation once again. The Irish border issue may, hence, be of more interest to Biden than the Brexit deal context within which it resides.

Thus, it’s personal and, the Union may get broken asunder, by POTUS, ultimately, despite all alleged attempts to hold it together for the sake of the Special Relationship. And then, again, Biden may just be a tough negotiator who is threatening Britain with a Trans-Atlantic breakup, and an internal breakup, if it does not toe the American line on all things global.

Truss is doing her bit, for survival, by de-emphasizing the role of the UK’s Endangered White Male species, in Cabinet, to make her government appear more like the herd of multi-ethnic buffaloes that roam in Joe Biden’s home. It looks like a freakshow and could well turn into a Rocky Horror Show, just in time for Halloween, as the Sterling/Cost of Living Crises meets the winter weather.

The new cabinet freakshow is hard to reconcile with Truss’s Daughter of Boris and Daughter of Thatcher joint sobriquets, as her fighting brand, which require White Male Spitting Image characters to be credible. Thus, one may assume that the new cabinet is window dressing, and, that the characters’ disguises conceal an acerbic White Male streak at heart.

There is, as always, no good substitute for regime change. Hence, Lizz Truss remains on short time as long as there is a Democrat in the White House. If President Biden survives the Mid Terms, Truss and her team are, immediate, toast.

It’s all a matter of who gets swiped right, and who gets burned at the polls.

Then it will be game on for the Britain Project, with its 1990s Tony Blair DNA. This game is already happening in the high street shops that are selling out of 1990s fashion.

(Source: the Author)

Assuming (prematurely) that they are toast, this author suspects that the Truss Family will be replaced by (or subsumed into) the outcome of the Britain Project after many swipes, of weak coalition dates of convenience, which are iterations of the end product.

Former PM, soon to be Lord Johnson, of wherever he so chooses (preferably of Bullingdon!), will not quietly shuffle off his political coil, however. The threat of a kiss-and-tell memoir will always be out there for those who have been leveraged over. A statue, that is untoppleable, and the biggest portrait ever, in the Palace of Westminster, would also seem to be fitting severance package contents/bribes to accompany the massive financial golden parachute extorted. The band of the Grenadier Guards may, also, be on hand to play My Way as the curtain falls. In short, he’s havin’ it large coz them’s his breaks. His Greasy Pole remains standing. Disraeli would be happy, Churchill less so. Walpole would be ecstatic.

(Source: the Author)

As expected, Boris Johnson won’t go quietly so he is being nudged. Also as expected, Johnson is more concerned about a golden parachute than guerrilla warfare. Hence, one of his post-PM gigs and platforms has been canceled, recently, by JP Morgan.

This never happened to Tony Blair when he went down the same route, to Morgan, post-PM.

The well-trodden route taken by Blair, and other “retired” political leaders is not just a golden parachute, however. It’s a real parachute, into clandestine action, behind enemy lines, changing regimes, and building a New World Order. The parachutists fly first class with all expenses paid, including regime change financing, by JP Morgan.

JP Morgan CEO Jamie Dimon can also be relied upon to blow some economic headwinds and tailwinds, every now and again, depending on the mission underway, as readers will know.

When one is facing global adversaries, who do not have a democratic process, like Russia, and China, it becomes necessary to fight dictatorial fire with undemocratic fire, at times, whilst still preserving the veneer of democracy. War is then waged by the unelected and their unregulated financial activities.

Enter stage-left the International Council.

The Dimon Hurrikraine is the (Tony) Blair Witch Inc. Project Tailwind ….

Britain is famous for its traditions, and institutional continuity, even if they lead to nowhere politically and economically. It is reassuring to know that this is still the case in this time of national mourning.

There is a new old face at the helm of the realm. This face will soon be on the coin of the realm.

The same-old new face is not on the coin of the realm, even though its invisible hands are still on the wheel and still all over the coin of the said realm.

Both sets of hands and faces intend to hold the realm together. But this is not within their gift. It is a quid pro quo gifted to them by higher powers. It is certainly not the gift of the British people, who have now become passengers on the ship of state. Some might even call the passengers economic hostages.

Evidently, Brexit-hater-in-Chief and JP Morgan CEO Jamie Dimon has been lobbied to deny Boris Johnson his rite of passage to a golden parachute. Dimon would, probably, not need much lobbying. In fact, it is perhaps Tony Blair, who chairs the bank’s prestigious International Council, that Johnson dreamed of joining, who nixed the appointment of Johnson.

The great thing about the International Council is that it appears to be a corporate governance function, at the global level. It is, however, at the granular level, utterly unregulated by any globally recognized regulatory body and, thereby, being self-regulated, it is autonomous. Basically, it has a free hit at whomever and whatever it pleases. And boy, does it have some hitters?!

Vae victis.

When one considers that Blair is a founding father of the Britain Project, and chairs JP Morgan’s International Council, everything starts to become clear. When one considers that his co-chair is ex-CIA Director Bob Gates everything is now crystal clear. Regime change, political, and otherwise is, presumably, planned here and financed by the bank. Project finance for the Britain Project was, presumably, conceived by this fertility treatment method also.

One may also wish to consider that Liz Truss has Tony Blair’s number in her political-Tinder equivalent dating app. Apparently, the two are in frequent contact. Perhaps they are planning a platonic assignation in the political middle-ground! They are, most likely, having a policymaking assignation on the Irish Border.

Tony Blair is rumored to be crafting a Brexit deal that will, satisfy Joe Biden and, allow Truss to look like a Brexiteer until she can get her feet under the table and start kicking shins into the Re-join line.

The bottom line is that Tony Blair is, apparently, the acting UK Foreign Secretary on the issues where the Tories are, allegedly, ideologically out of sync with America and the EU. How many of the deals done, through this side door, are elected UK government policy decisions or globalist-agenda Blair Inc. policy remains moot. Suffice it to say, that although James Cleverly is, nominally, the UK Foreign Secretary, in practice, he is not.

Cleverly is clearly out of sync with Blair, America, and the EU on Brexit. So, best he stays out of the negotiations and just gives the press briefing once the deal has been done by Blair et al.

The Truss Family may, thus, not be toast as this author (prematurely) assumes. Their toasting is just for effect. Some of them may also have to get eaten, in order for the charade to look authentic. Those who get eaten will be from the Right of the party. For example, Jacob Rees-Mogg walks (and talks) like one of the condemned to be eaten. James Cleverly is clearing on Tony Blair’s hit list after his, toadying, association with Boris Johnson, and strong Brexit credentials. The Family insiders will understand the game, however, and will survive. In fact, the survivors will be rewarded in the new middle-of-the-road party that supersedes them.

Hence, Truss’s ship may appear to be taking on water, right now, but this may only be a prelude to it being thrown a life raft by the Blair Inc. Witch Project. The noisy Sterling Crisis and related economic disasters are, hence, in fact, props and nudges which will make the ultimate political outcome appear to be a natural conclusion.

It is easy to see Truss going through the motions of appearing to support ancient Tory shibboleths, as the ship sinks, only to hijack them and merge them into Blair’s new middle-of-road project. She had to embrace them to get elected as Tory leader. It’s what she does, going forward, that will indicate her real intentions and capabilities.

After all, Truss did start her own Rake’s Progress as a Lib-Dem. Clearly, she has the ability to change political hats as swiftly as she changes her designer clothes. Who better, than this kind of political chameleon, to engineer and survive a great transition, in UK politics, at a time of change for the monarchy?

If this author observes that the Labour Party goes into a similar “metanoial” breakdown, as the Tories have, he may conclude that the two major UK political parties are being deconstructed with a view to reconstruction, from the sum of the parts, in the middle ground. Let’s call it the Blair Witch Inc. Legacy, in homage to the puppet master of this latest series of Spitting Image.

A hung parliament, at the next general election, would be the condition precedent most desired by the Britain Project. It would even call for a grand coalition, of the main parties, something not seen since World War II. If the pundits are correct, the world faces a similar conflagration, so Britain would be in good political shape to cope.

The tangible engineering of hung-parliament dynamics, by all those involved, would, hence, be the key signal that the Britain Project is being executed by both main UK parties. The re-framing of Tony Blair, favorably, in the British psyche would also be a key signal.

Whilst considering Truss, one may wish to re-read the article entitled Dimon’s Hurrikraine Is The Summers’ Curse And The Biden Slam Dunk. This article may provide context.

After re-reading, one may then consider that this author’s global macro thesis, for 2022, is less fictional and more factual.

If still skeptical, after reading, and considering, the reader may then wish to peruse a photograph album of the JP Morgan International Council’s 2019 meeting in New Delhi.

· India has been offered the choice of becoming a player, or a battlefield, in the Sino-American “Techno-Economic War” with the “Triad’s” live sales-demo in Afghanistan.

(Source: the Author)

After perusing, and reminiscing, the reader may then wish to replay what has happened, globally, since then, including COVID-19, and culminating with PM Modi’s recent announcement that India wishes to become a developed economy, in 25 years’ time, along with all the bizarre courtship rituals, on display, between China and the USA toward the Subcontinent.

· The MSP and the Biden G7 “Slam Dunk” “Friend Shoring” G7 Infrastructure Plan are Vinod Khosla’s “Techno-Economic War”.

(Source: the Author)

Modi’s announcement is a firing pistol for a new race, synchronous with President Biden’s firing pistol for a “Techno-Economic War” race with China. Modi is suggesting that this will be a marathon-plus-one-year race. Uncoincidentally, Vinod Khosla is, himself, of Indian extraction and “Techno-Economically Armed” to the teeth, as well as being a firm supporter of “Speaker Pelosi’s Bottom”, has heralded both firing pistol shots.

The two shots do not signify a false start, it’s the real thing this time. It may even be the Big T’ing that the FOMC Crew, of Deformed Hedgehogs, are totally overlooking. Hence, if it is difficult to accept this author’s report, of the audible firing pistol shots, it is much harder to doubt Khosla’s expert opinion of their caliber and trajectory.

Even if any of the events in the reader’s own Event Time-Line Analysis, seem to be coincidences, he or she cannot help in concluding that they have also been helpfully sequential in fitting the broad aims of the International Council as stated in 2019. Helpfully sequential, implies the agency(ies) of invisible, at arms-length, hand(s). One sees, and feels, the actions, of the hands, but one just can’t see the connections, of the same hands, to the bodies making the decisions.

The vote-calculating, culturally-obtuse PM recently chose to rekindle the flames of Partition by athletically disporting himself at a manufacturer of machines, which are used to demolish Indian Muslims’ homes, during the Holy Month of Ramadan. Well, “they” all vote Labour, don’t they?

(Source: the Author)

The reader should also think back to Boris Johnson’s, failed, currying of favor with India through his inspired cabinet selection of scions of the Subcontinent. Evidently, some informed bets were being placed by Johnson.

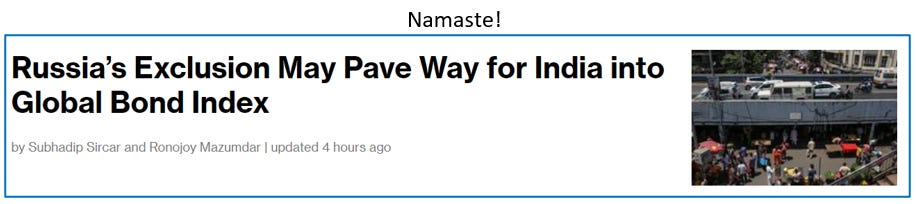

If the perplexed reader is still not guided then he, or she, could, perhaps, focus on the new news that JP Morgan is widely expected to drop Russia from its emerging market bond indexes and replace it with India.

If one still doesn’t get it, then, one has no hope. One should, hence, let JP Morgan Asset Management seek one’s Alpha and apply to the International Council to seek guidance and enlightenment. Alternatively, one can read fiction and fairy stories instead of the Key Signals Report.

Superb analysis, and always challenging and edifying. Thank you.