A Multi-Polar World Order Was Born At G20 Indonesia 2022

If you are not part of the G20 global growth solution, you are part of the problem.

Summary:

· A multi-polar global economic order was born at G20 Indonesia 2022.

· The G20 embrace of the growth risk narrative, behind Macklem Doctrine, will increase the pressure on central banks to swiftly conclude their monetary policy tightening cycles.

· America is pivoting towards a strategic reset with China.

· Faced with potential expulsion from the WTO, China is swiftly trying to build a global alternative.

· The US inflation spike has been blunted, in the short term, thereby, enabling Macklem Doctrine to be rolled out sooner than the FOMC currently estimates.

A Multi-Polar World Order is born ….

The current confluence of events, ranging from inflation to Ukraine, have all met each other at G20 Indonesia. It is hard to believe that this confluence was a coincidence. In addition, a new challenge was strategically positioned to frame and resolve all the conflicting agendas at the summit. This new challenge is the threat to global economic growth.

G20 did not deliver a solution, however, it did provide the context, and the platform, for the attempted resolution of the specific issues over the coming year. The final communique prosaically announced that: "We (G20) will also continue to monitor major global risks, including from geopolitical tensions that are arising, and macroeconomic and financial vulnerabilities."

G20 has signaled that it is going to focus on growth, rather than inflation, going forward. Hence, the pressure on central banks to tighten monetary policy, already, and join the G20 agenda will increase throughout the year.

The invisible hands that signed the paper ….

China and Russia, heavily, censored the abridged version, of the final G20 communique, in order to provide a statement that included them as part of the solution rather than to be identified as the problem.

It is noteworthy that China and Russia were able to pull off this G20 communique coup relatively unopposed. There is, apparently, no appetite to confront them, on the ground or, at global economic forums. The increasing pressure recently exerted, on the ground and sea, by China and Russia, respectively, in Ukraine and the South China Sea could be seen as probing attempts to force the desired outcome at G20 Indonesia.

G20 has, thus, been established as the first platform that gives China and Russia the greatest level of global influence that they have enjoyed to date. This influence is, arguably, greater than any that they may achieve by annexing the territories that they currently covet and threaten. This G20 summit was, thus, significant in establishing the strategic parity of China and Russia in global affairs, effectively, for the first time in the group’s history. At some point, in the future, looking back, some may say that a multi-polar global order was born at G20 Indonesia 2022.

China, also, transcended G20 as being the major only economy to already be promoting the economic growth that is allegedly being threatened. Whilst the growth threat has been introduced, at G20, China has already positioned itself in advance of it. China, therefore, controls the global growth narrative for now, and may thus promote itself as one of the good guys.

A previous report has discussed the thirty-year growth narrative, currently, under construction in the developed economies.

The threat to this thirty-year narrative is the ugly statistic that global economic growth is being cannibalized, and thereby threatened, by despots and dictators. The question now is whether the 74% remaining democracies compromise, with the dictators, in pursuit of economic growth. G20 Indonesia was the latest opportunity to view this dialectic and potential compromise in progress.

The precedent, for compromise, already exists, in the swift dropping of the low-Carbon narrative in order to address the energy component of the current inflation spike. Furthermore, supporting hydrocarbon energy sources could, easily, be framed as supporting global economic growth.

The Chinese and Russian leaders appear to think that the compromise fix is in, and intend to exploit perceived weakness to increase their respective shares, of the global GDP pie, going forward. Their multi-polar worldview sees three poles. One pole is in the (contained!) NATO region, one is in Eurasia and the other is in Asia. Evidently, their worldview is to minimize the American sphere of influence in each pole and maximize their own respective influences.

The free press in western democracies has an interesting view of the growth story. The despotic 26% has, neatly, been framed to replace the 1% (who currently control most of the developed world’s GDP) as the new global bogeyman. Thus, attention, and blame, have been diverted to the 26% as being the greatest threat to the global economy. The 1% can, hence, mobilize the 73% to blame the 26%, for their current economic suffering, rather than confiscate the extreme wealth of the elite few.

Divide and conquer ….

· The American thirty-year narrative involves the funding and creation of a bipartisan consensus from the perceived Chinese threat via Latin America.

· In view of the thirty-year narrative timeline compression, the Fed has limited time and space available to taper.

(Source: the Author)

One cannot help but notice that China and Russia (the putative 26%) are, currently, diverting American forces, along two fronts, whilst the partisan domestic political situation divides and dilutes the power of said diverted forces.

It is, also, quite easy to discern the American global response.

A bi-partisan initiative, led by Senators Bob Casey (D-Pa.), who is leading a bill with Sen. John Cornyn (R-Texas), has formed to legislate greater oversight, regulation, and intervention over capital and technology transfers between America and China. Senator Casey is on record as saying that America is in an “economic war” with China.

This “economic war” is not just being fought in Asia and Eurasia. It is also being fought in Latin America.

No place for Baby Boomers ….

With the world’s news channels, seemingly, transfixed, by events in Ukraine, a few good men in the US Senate are reprising Operation Mongoose.

El Salvador is one beach on which to, rhetorically, land and Bitcoin is the regional casus belli. The US Senators wish to advance to contact and investigate El Salvador’s use of Bitcoin and its threat to American interest in the region. President Bukele has branded the investigators “Baby Boomers”, with no jurisdiction in his country.

Those still unpersuaded, by this author’s Bay of Pigs analogy, may wish to read, and watch, the recently released Bloomberg version of events; and note the timing of this story as well as the headline. The Bloomberg editorial headline is that China is winning in South America. This journalistic source and view are guaranteed to provoke a response in Washington.

Sanctions, against El Salvador, are the obvious outcome, of a bipartisan Senate investigation, however, a more robust intervention should not be ruled out, especially if China is identified as the invisible hand moving the Salvadorian pieces around the chessboard. It is, also, no coincidence that a White House Executive Order, specifically in relation to Cryptocurrency, is just about to be simultaneously executed.

An ensuing wider US intervention in Latin America may, then, be a small step in a much wider global move to engage China.

America is, currently, on the back foot in relation to this wider global move.

The Pivot slips towards a Clean Break ….

Yuankee go home ….

The Yuan is also establishing its own reserve currency status in the Emerging Markets space, which threatens to challenge the global reserve status of the US Dollar. The Peoples’ Bank of China (PBOC), and its monetary policy settings, are more in sync with the Emerging Markets economic cycle than the Fed and its own settings.

(Source: the Author)

America’s pivot towards Asia is losing its footing on the ground. A recent poll found that more than half of those locally involved now view the Chinese economy as more important for the region than the American one. All this, even before the FOMC has made the US economy even less significant, and weaker in general, by tightening monetary policy. Concurrent with this theme, the Peoples Bank of China is moving to mitigate the regional capital flight that the FOMC will, allegedly, trigger when it starts to tighten monetary policy.

This combination of moves, by the FOMC and the PBOC, will have the long-term impact of weakening the regional influence of the US Dollar whilst promoting the influence of regional currencies linked to the Yuan. The FOMC will, thus, be helping the PBOC dismantle the Dollar’s reserve status, in Asia, and promote the Yuan’s eventual reserve status in its place.

Faced with current trade policy failure, the Biden administration is going for a radical reboot. The White House thesis is that China has consistently failed on its promise to adopt the market-orientated policies of WTO membership. The implication is clear. China either rapidly remedies its protectionist policies or is expelled from the WTO. There is now twenty years of evidence to justify this threatened expulsion.

“We envision an Indo-Pacific that is open, connected, prosperous, resilient, and secure—and we are ready to work together with each of you to achieve it.”

President Joe Biden

East Asia Summit

October 27, 2021(Source: whitehouse.gov)

Momentum for this Chinese ultimatum has recently been nudged, by the launch of the White House strategic vision for the Indo-Pacific region. U.S Assistant Secretary of State for East Asian and Pacific Affairs Daniel Kritenbrink has, recently, clarified that China is, currently, excluded from this strategic vision.

Faced with, potential, impending expulsion from the WTO, China is quickly trying to build an alternative trade system with its Belt and Road strategy. In addition, China has also backed the world's largest free-trade bloc, which excludes the United States, the Regional Comprehensive Economic Partnership (RCEP).

The FOMC will be under pressure, not only to embrace the global growth narrative but also, to embrace American global geostrategic interests. Both of these agendas require fiscal stimulus, low interest rates, and sponsorship on the Fed’s balance sheet in order to be achievable.

The window of opportunity for the Fed to fight inflation is closing.

No place for trigger-happy old men and women ….

With the beat of the war drums getting louder, in Ukraine, and rising oil prices blowing stronger global economic headwinds, San Francisco Fed president Mary Daly is keen to emphasize the need to avoid “abrupt and aggressive” monetary policy action from the FOMC.

James Bullard no longer has credibility.

(Source: the Author)

Daly’s warning, initially, appeared to have gone unheeded by her FOMC colleague James Bullard. Bullard began to embar on a Kamikaze mission, to frontload interest rate hikes, and start balance sheet reduction in Q2, with the objective of restoring the FOMC’s credibility at the expense of economic growth. Crashing the US economy, with front-loaded interest rate hikes, allegedly, restores the FOMC’s credibility. It seems to be an absurdly high price to pay for credibility.

Long live King Thomas, or at least until the March FOMC meeting!

Famous last words: “If you can keep your head, and say Holy Cow, when all of those around you are losing theirs, and shouting Katie bar the door, you should be the Fed Chairman my son!”

(Source: the Author)

Evidently, Bullard, has, since then, reconsidered his position and announced his modifications on CNN. Whilst reconsidering, he has also embraced Richmond Fed president Thomas Barkin’s advice, to swiftly return monetary policy settings to neutral before acting again. Bullard believes that these neutral settings are circa a 2%-plus Fed Funds rate.

Cleveland Fed president Loretta Mester appears to be going half-Kamikaze. Currently, she foresees a process of interest rates hikes, and balance sheet reduction in H1/2022; with the option to go full-Kamikaze, in H2, depending on the inflation situation

Minnesota Fed president Neel Kashkari has decided to be qualitative, rather than quantitative, under the current circumstances. He would, thus, not like to “overdo it” with rate hikes, without being able to estimate what this overdoing might be in terms of basis points over time.

To improve her chances, alongside Post-Tempore Chairman Powell, Brainard has sworn under oath to be a tough inflation fighter. Brainard must therefore be that same Hawkish trope, that she swore an oath to be, in order to avoid being perjured. Consequently, she is keen to get cracking on a process of interest rate hikes and balance sheet reduction soon.

Chicago Fed president Charles Evans is no longer in denial, about tightening monetary policy, but the rueful syntax and language, of his latest guidance, show that he is still reluctant to acknowledge that interest rates will rise soon. He feels that he and his colleagues have been “wrong-footed”, but shouldn’t necessarily become right-footed in a hurry. Unfortunately, Evans has no credible explanation of why he and his colleagues have been so easily misled.

Consequently, Evans deploys the euphemism that, over the long-term, less restrictiveness may be needed. This less restrictiveness, therefore, does not need a large initial interest rate hike in March. Twenty-five basis points would appear to be as far as Evans would go in March, and probably at subsequent meetings.

New York Fed president John Williams, like Evans, is procrastinating and dragging his heels over the inevitable tightening of monetary policy. His latest hold-out is an observation that a big-step rate hike in March is not warranted. Nonetheless, Williams remains committed to the process, of incremental rate hikes, outlined at the last FOMC meeting.

Don’t shoot the messenger ….

Fed Governor Christopher Waller’s latest research piece has provided the empirical underpinnings of the FOMC’s hasty future rate hike actions.

Waller finds that monetary policy stimulus narrows racial income disparities, but not the level of labor force participation amongst the various ethnic groups. So, broad inclusion is not really broad inclusion, as advertised by the Fed, after all. Furthermore, all narrowing income disparities then blow out, even wider, during ensuing recessions. Broad inclusion, thus, only works in economic expansions so it is a pro-cyclical artifact, at best. At worst, it widely excludes, those intended to be broadly included, whilst making the US economy more unstable in the process. Quelle epitaph!

Waller, then, finds that a monetary policy framework, aimed at inflation target overshooting, that is in place for too long, creates economic vulnerabilities that undermine all of its benefits, during the economic expansions, and then unwind all of them during ensuing downturns. Fed new Monetary Policy Framework RIP!

Waller’s finding, quietly, kills the new monetary policy framework, without attaching any blame for its failure, so that the FOMC can get to what it apparently does best in fighting inflation.

Evans’s “wrong-footed” feeling is explained away, by Waller’s thesis, but the Fed and the FOMC are blameless for creating the feeling. This author would say that this does not mean that the Fed’s credible commitment has been restored.

The FOMC now has the empirical collateral to wave at hostile lawmakers who want to know why it is the enemy, in the form of the PBOC, that is helping the US economy and US strategic global interest. The FOMC also has a small window of opportunity, which is getting smaller, to complete its empirically justified monetary policy tightening.

No place for Macklem Doctrine, yet ….

One way to realign the FOMC, with the G20 global growth agenda, would be to frame any new domestic economic stimulus as a supply-side one, aimed at unblocking supply chains, in order to promote growth. In the economic war with the 26%, the theme of onshoring the supply-side could also be strategically promoted.

Thirdly, in response to the trap being set for the FOMC, by the White House, this author expects “Supply-Side Janet Yellen” to start promoting her own pre-flagged solution, which is a fiscal stimulus aimed at unblocking supply chains.

(Source: the Author)

Secretary Yellen has already made her case for the supply-side stimulus. Expect more of the same from her within the G20 frame of reference, going forward.

· The White House Indo-Pacific Doctrine is Macklem Doctrinaire in principle.

(Source: the Author)

As noted in the last report, Macklem Doctrine, as explained by the Bank of Canada Governor, is the first central bank strategy that supports the supply-side stimulus thesis. Expect more of the same from other G20 central bankers, going forward.

The major catalyst for Macklem Doctrine is progress on inflation. There is, some, evidence that this catalyst is working.

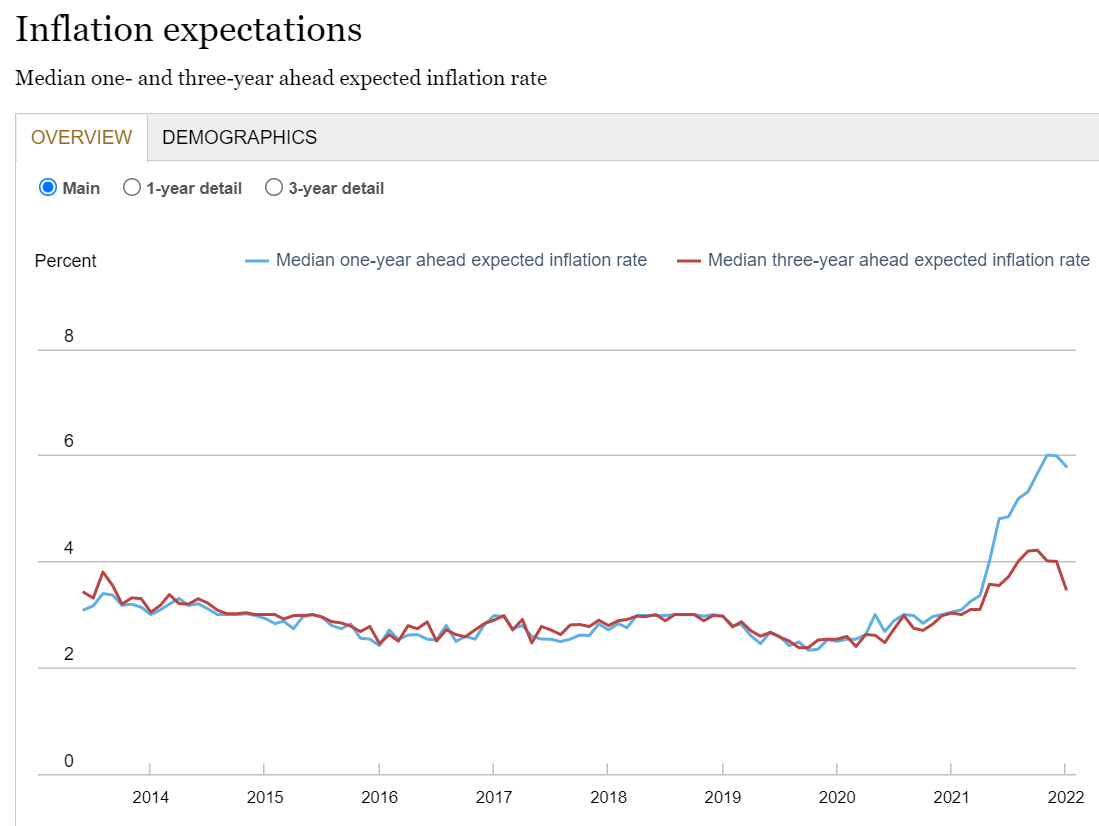

The inflation spike gets blunted by the New York Fed ….

In the last report, Atlanta Fed president Raphael Bostic had alluded to short-term inflation indicators peaking and beginning to fall. Further supporting evidence was recently provided by the New Fed’s Survey of Consumer Expectations (SCE). Just as the FOMC signals its serious intentions and capabilities to deal with the inflation spike, the spike itself seems to have been blunted.

The SCE report, in general, contains further signs of moderation in both economic growth and prices. The commentary, from the New York Fed staffers, which accompanied the report, was certainly keen to emphasize the moderation of all short-term things inflationary, and the stability of all long-term things inflationary. This, then, begs the question of whether the FOMC will still act with the same proposed vigor or not. This question has, already, been begged, and answered by Tiff Macklem. G20 is currently doing some more begging and answering.