The Global Economy Diverges At Friend-Shoring Junction

“Turn West for Macklem Doctrine, or, Turn East for Belt and Road Initiative. Or, go full steam ahead for Global Recession.” (Unattributed)

Summary:

· The World Bank endorses and proselytizes Macklem Doctrine, whilst the IMF multi-polarizes it.

· With the notable exception of Pro Tempore Chairman Powell, US inflation is now accepted by many on the FOMC as a significant economic headwind.

· The “Bostic Put” joins the “Waller Put” on the list of “Fed Puts” being extensively forward-procrastinated.

· Bullard’s Greenspan panegyric and Nabiullina’s lament are confirmations of the policymakers’ 1990s model hiding in plain sight.

· Black Gold, Banana Republics, and Old Habits define new potential Bay of Pigs and Malvinas Moments flashpoints.

Oh, say can you see Friend-Shoring Junction by the (“foggy”) dawn’s early light?

Renowned strategist, author, legend, and former US national security consultant, Edward N Luttwak has recently opined on the apparent intelligence failure, of the international community, to correctly estimate the tenacity and purpose of the Ukrainian resistance to Russia.

A further perusal, of Mr. Luttwak’s bibliography, suggests that he has anticipated current global events for some time. On the eve of the World Bank and IMF Spring Meetings, Mr. Luttwak turned his attention, to the global economic battlefield, and asked: “if the monetary authorities are up to their tasks”. The answer remains to be seen but will be seen, in due course.

The G7 “monetary authorities” have a plan, and events in Ukraine could be said to neatly act as a catalyst for it. All that is required is some rhetoric to conflate current global threats, and their causes, on the surface of this catalyst.

Said “monetary authorities” are well up to this specific rhetorical task. In many respects, this is why they exist. It is certainly why they were created. This rhetorical skill was recently demonstrated by Secretary Yellen blaming Russia, exclusively, for the latest increase in global food insecurity and derived inflation. Following this pronouncement, G7 finance ministers have set about totally isolating Russia from the global economy. Ironically, this action would seem to have made the inflation situation worse. But every inflated cloud has a disinflationary lining, if it rains supply-side investment financial liquidity. More on this deluge later. With the culprits identified, shamed, blamed, and ostracised it then fell to other monetary authority representatives to identify these supply-side liquidity solutions.

The Spring Meetings could, hence, be viewed as the platform upon which this rhetorical catalysis will occur.

The Global Economy Approaches Friend-Shoring Junction

“To Macklem, or not to Macklem? That is the real question.” (Unattributed)

(Source: the Author)

The last report précised the Spring Meetings under the headline “Friend-Shoring Junction”. The process of “friend-shoring” was envisaged as a repositioning of global supply chains away from their current configuration, and concentration in countries antipathetic towards the G7 rules and governance architecture. This process has been called Macklem Doctrine, by this author, in recognition of one of its main progenitors the Bank of Canada Governor Tiff Macklem. In essence, the doctrine envisions supply-side investment to unblock global supply chains, in order, to promote inflation defeating economic growth.

· G7 has canceled G20 and all multipolar initiatives associated with it.

(Source: the Author)

“Friend-shoring” was understood as a practical necessity, preferable to onshoring, since the USA requires trade partners for both its imports and exports. Based on this principle, Treasury Secretary Yellen has continued to soften her position toward some of the trade partners in the G20. She recused herself from direct contact with Russian representatives, at the Spring Meetings, and led the walkout by the Anglo-Saxon G7 cadre within G20. By comparison, the other walkout, led by the World Bank, was much more global and, thereby, meaningful than the G20 protest.

Both walkouts, however, left a significant critical mass, including some G7 members, to negotiate with Russia. The rump G17-ex Anglo Saxon bloc, still, remains a medium of dialogue that the Anglo-Saxons can interface with. One may, thus, infer that G7 has softened its attitude towards G20 also. Having initially wished to break up G20, over Russia, and China, G7 now wishes to “friend-shore” some of its members.

One should not, however, expect too much from the G17, immediately. The EU’s Economic Commissioner, and global nuncio, Paolo Gentiloni has opined that the events in Ukraine “will also spell the end of globalization as we have known it and reshape global alliances”.

The global economy is going into the phase of metanoia in which things are being broken. The rebuilding phase has not yet occurred. There may, in due course, be more, or less, digits behind the “G” that designates the “G-Thing” of the next iteration of the New World Order. Despite this uncertainty, however, presumably, the reassuring acronym of G7 will transcend the epochal shift.

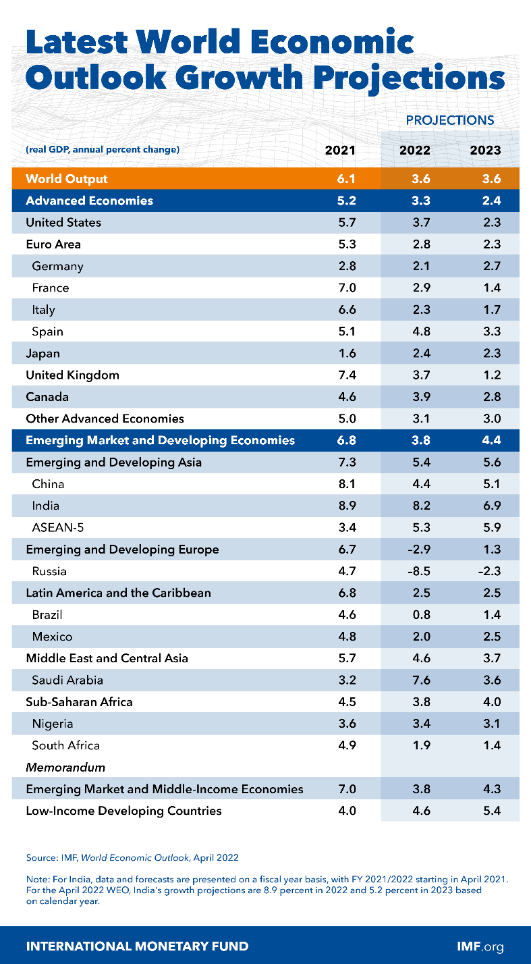

The IMF has left nothing to the imagination, about the stakes involved, with its characterization of the view, of the global economy, being obscured by the “Fog of War”, from Ukraine.

This “Fog” does not, however, conceal the fact that the IMF sees a large divergence in economic growth ahead. Developed economies will slow down. China and the ASEAN-5 will grow, albeit weakly. The rest of the developing world will slow down.

So, in conclusion, at “Friend-Shoring Junction”, an economy can turn West for a slowdown or East for growth, as things currently stand, according to the IMF. The IMF does not, however, suggest that economies should follow this binary-outcomes approach. On the contrary, Chief Economic Counsellor Pierre-Olivier Gourinchas recommends a multi-polar solution. In his view, this transition to a managed multi-polar system would avert global “disaster”.

The IMF’s market surveillance head also notes financial stability risk rising, which he attributes (exclusively) to the War in Ukraine, rather than any association with the capital markets’ collective reaction to rising inflation and central bank monetary policy tightening. Ukraine is the IMF’s Alpha and Omega for the causes of all the world’s problems. By inference, therefore, it is also part of the solution.

· Unrealized balance sheet losses may have just triggered the Macklem Doctrine embracing “Fed Put”, in the form of the “Waller Put”.

· The “Waller Put” signals that the FOMC will not kill the “Build Back Better” and “Make More In America” booms.

· The recent Wall Street earnings season-wink signals that the US financial sector has, already, become the medium of economic transfer of the FOMC’s “methodical” and “expeditious” tightening which has only just begun.

· The Dallas Fed kicks off the “FOMC Two Step”.

(Source: the Author)

In view of the IMF’s new call on financial stability risk, one should connect the dots to the appearance of the “Waller Put”, in lieu of the “Fed Put”, in the last report.

Clearly, the Spring Meetings were supposed to enable the discussions that were intended to divert, in order to redress, the economic divergence, pictorially represented by the IMF above, at “Friend-Shoring Junction”. Indeed, one could argue that the whole point of the Spring Meetings was to “friend-shore” economic growth back West, via trusted trade partners, presumably away from China. The ASEAN-5 were, hence, the key economic territories to be fought over about growth. Clearly, if they were offered “Friend-Shore” status this might tempt them away from what China has to offer.

Through the “Fog”, there was a clear outline of the G7 strategic passage through “Friend-Shoring Junction”. Unfortunately, this passage involved economic warfare on a global scale. Clearly, IMF Chief Economic Counsellor Gourinchas would prefer cooperative rules of engagement, rather than no quarter terms.

Getting through this foreseen economic war, without a major conflagration, will take the acme of skill and diplomacy. It may also require lots of mini-conflagrations, like Ukraine, as a combination, of catalysts and fire-breaks, to prevent the big one from occurring. The omens are inauspicious.

As the Spring Meetings were occurring, and with its own economy imploding, China doubled down on its strategic commitment to Russia. Globally speaking, therefore, it appears, quite literally, to be turn West for the USA, and turn East for China.

Assuming that there is going to be one, global posterity may look back at “Friend-Shoring Junction” as “Clean Break Junction”. Treasury Secretary Yellen is, however, not ready to break just yet. Whilst a strategic re-evaluation, followed by restructuring, of the global order, as governed by the World Bank and IMF, is in process, Yellen still wishes to include China and its supply chains in the debate.

Macklem Doctrine: Go West through the “Fog of War” ….

Whilst the IMF played at global bad cop, with its pessimistic framing of the global economy, its sister organization, the World Bank, was pragmatically optimistic.

In his opening address, World Bank Group President David Malpass set out the agenda of the meetings, by conflating the global balance of risks of lingering COVID-19, rising inflation, and Russia's invasion of Ukraine. The World Bank’s view is broader, in terms of causes, and opportunities for solutions, than the IMF’s narrower focus on the catalyst of Ukraine. This confluence of factors has prompted the World Bank to cut its global economic growth forecast. The subliminal message is, the same as the IMF’s, however, that growth is the solution to the global problems.

The World Bank’s pro-growth solution, to the conflated global problems, is to break down trade barriers and support the supply-side of the global economy with capital investment and strong governance.

· Macklem Doctrine ticks all the “friend-shoring” boxes.

(Source: the Author)

Specifically, in relation to Macklem Doctrine, Malpass opined that, currently, “capital is being misallocated”. He directed capital markets, and central banks, to address this misallocation in order to boost real economic growth which does not boost inflation. In his own words: “I (Malpass) want to turn now to the inflation problem, which is causing immense strain. Policies need to be adjusted to enhance supply, not just increasing demand. Markets are forward looking so it's vital for governments and private sectors to state that supply will increase and that their policies will foster currency stability to bring down inflation and increase growth rates. This is especially important as global supply chains shift away from dependency.”(Author’s emphasis)

In Malpass’ opinion “central banks can use more of their tools, not just interest rates. Capital is being misallocated now. One of the focal points should be using all the central bank tools so that capital is allocated in a way that helps increase supply”. His view of simplistically hiking interest rates and then expecting the global economy to neo-classically rebound, when inflation falls, was rather a dim one. One may, therefore, assume that Malpass is not overly-impressed with the current Hawkish zeal, of some G7 central bankers, even if it is only just words.

An inverted yield curve should signal a belief in falling inflation, rather than rate-hike induced recession applying Malpass’ worldview. This is the challenge now facing the overzealous central banks. Unfortunately, if yield curves now start to steepen Mr. Market might, logically, conclude that central banks have lost their control of long-term inflation expectations. An inverted yield curve, thus, seems to be more acceptable under the circumstances to central bankers.

Malpass wants the global economic supply-side to be geographically, and financially, moved to places, where there is a faith in free trade, in order to sustain a neo-classical rebound. He is of the view that global economic productive capacity is, currently, concentrated in the wrong hands.

Malpass’ sublimely inculcated form of economic warfare requires its own supply-side investing, and fiscal deficits of considerable magnitude. It also requires its casus belli which is understood by its taxpayers.

The US Fiscal Deficit: A Quantum Leap to Infinity and Beyond Inflation….

Conflating the global threats of Climate Change and Energy Security, the US Department of Energy (DOE) has initiated further fiscal spending in the form of a Civil Nuclear Credit Program.

Conflating the global threats of Climate Change and Energy Security, the US Department of Energy (DOE) has initiated further fiscal spending in the form of a Civil Nuclear Credit Program.

This is all well and good, but the Big Bucks, as we all know, however, are in the Department of Defense’s hands.

The last report discussed the state of the US fiscal stimulus in relation to the “missile gap” with China (and Russia) which had extended to outer space. President Putin, then, supported the thesis by testing an ICBM to demonstrate his intentions and capabilities over Ukraine. Potaytoes-Potahtoes, both sides seem to feed each other's hysteria and military spending.

Further zeros must now be added. to the fiscal stimulus, in order to narrow the alleged quantum computing gap with China. The emerging conclusion, to be drawn, from the sequential news stream, is that the field of combat for the emerging conflict is primarily technological. Onshoring/Friend-Shoring should, thus, be viewed through a technological prism rather than the simplistic repatriation of low-value manufacturing supply chains.

Newsflash: Inflation is now a headwind ….

Positioning US inflation as casus belli, for a major supply-side economic transformation, should be easy to achieve in practice. The US consumer is already feeling it, so the proselytizers and nudgers are pushing on an open door.

· On aggregate, the overextended US Consumer is most likely to be subsisting on inflation, rather than gorging on it, but the Fed is assuming the latter.

(Source: the Author)

It has been suggested that the US consumer “is most likely to be subsisting, rather than gorging on inflation”. Empirical confirmation is now coming in to support the anecdotal evidence that the consumer is subsisting.

The divergence, of the Sticky and the Flexible inflation readings, speaks, to what is transitory and what is not in the inflation basket.

(Source: the Author)

It has also been observed that “the divergence, of the Sticky and the Flexible inflation readings, speaks, to what is transitory and what is not in the inflation basket”. It can also, now, be said that this divergence speaks to a growing economic headwind.

Transitory inflation is currently being made more transitory, by the geometrically compounding intransient inflation. This exponential divergence process is manifesting itself in the form of an economic headwind. This headwind comes about as the Sticky Inflation drivers substitute for and, thereby, cannibalize the Flexible Inflation drivers in the consumers’ basket. This headwind is known as demand destruction.

The latest Sticky CPI report, from the Atlanta Fed, strongly, suggests that inflation has now also become a consumer-driven headwind for the US economy. Previously, it was assumed to be a purely margin-destroying headwind to the production side of the economy.

The Core Sticky CPI data, reflecting what the consumer lacks discretion about purchasing, continues to rise. This rise erodes consumer purchasing power, thereby, causing the Core Flexible CPI, reflecting some discretionary purchasing power, to move lower.

Further clarity, and context, to this inflation measure divergence, have been provided by recent research from the Cleveland Fed. Unsurprisingly, the researchers found that economists’ inflation expectations are driven by incoming published inflation data. Similarly, unsurprisingly, consumer inflation expectations are driven by what they see in the shops. This may explain why Minneapolis Fed president Neel Kashkari, most notably, but also other FOMC members, thought that inflation was transitory for so long, whilst consumers hunkered down and expected it to persist.

Smoke and Mirrors on Liberty Street ….

Time For No More Mr. Nice Guy From Chairman Powell

Mar. 23, 2021 10:02 PM 19 Comments14 Likes

Summary

The Fed has become a prisoner of the US Treasury.

(Source: the Author)

The New York Fed is, somewhat disingenuously, trying to dissemble the Atlanta Fed’s diverging CPI findings. In so doing, the New York Fed’s staffers also dissemble accusations of any loss of vigilance on inflation by the FOMC. This seeming coincidence is not lost on this author.

Powell's “Transitory” Inflation Becomes Bullard's “Inflation Shock”

Dec. 06, 2021 10:59 PM ETTLT, USDU

(Source: the Author)

In a recently published dissembling article, the New York Fed’s researchers try to empirically prove that inflation did not become intransient, as this author suggested, back in March 2021, but actually in September 2021 when James Bullard made his, now infamous, “inflation spike” intervention.

Pitchforks and nooses on Capitol Hill ….. again?

· The Fed is diverging from the White House and may even, officially, blame the Federal Government, for the current inflation spike, under oath.

(Source: the Author)

The dissembling obfuscation, of the inflation continuum timeline, by the New York Fed, is critical for the Fed dissociating itself, from culpability, during a period of inflation target overshooting, and broad inclusivity, when the inflation first started to rise.

In effect, the New York Fed is rewriting economic history. As Churchill understood, history is kind to those who write it. As this author has noted, the Fed’s day on the stand may be coming; when the central bank is called to account, by Congress, for its poor inflation mandate performance. This author, also, notes that the Fed may be carefully laying the blame for this mandate failure at the US Treasury’s door. The New York Fed’s recent dissemblance would appear to confirm this suspicion.

Do not run too fast, and too far, when dodging pitchforks and nooses ….

The eroding US consumer purchasing power, deliberately dissembled, and otherwise, is, nonetheless, a monetary policy tightening, in real terms, which it behooves the FOMC not to compound egregiously with its own monetary policy tightening.

If it can be taken as a consumer barometer, Netflix’s recent loss of subscribers and its remedial business model tweak, to allow advertising, further confirms that the consumer retrenchment is already at an advanced stage.

Over on the production side of the US economy, Morgan Stanley has just noted an inflection point, in Q1/2022, at which inflation became an economic headwind that is destroying margins.

Thus, on both the production and consumption side of the US economy, inflation is a growing economic headwind. What then of the further headwind blowing from the Fed?

There is, already, chatter on the wires about Powell’s legacy and potential changes to the Fed’s recently adopted new monetary policy framework. Suddenly, everything, including Pro-Tempore Chairman Powell’s confirmation, is up in the air. Questions are, pointedly, being asked about the Fed’s performance and what it is actually focused on.

Evidently, Powell is stuck in Pro Tempore mode and is trying to break the deadlock. Consequently, he now ignores the economic headwind and intends to make it worse with a series of 50-basis point rate hikes.

Genus Central Bank Put and related animals ….

With the global and domestic economies slowing, it is inevitable that people should think of the “Central Bankers’ Put”. This option is being written, but not exactly verbatim as previously. This time around, the put option is more of an option not to tighten monetary policy aggressively.

We don’t expect you to talk, we expect you not to tighten Mr. Central Banker (reprise)….

ECB Governing Council member Ollie “Rehnfeld” Rehn is noted as being one of the progenitors of this do no harm put option writing. His legacy lives on in various degrees at the FOMC.

The situation is more Beige than Black and White ….

The Fed’s recently published Beige Book showed an unerring correlation between the regional economies, in the disparate Federal Reserve Districts, and the global economy. It was as if the IMF and the World Bank had written the Beige Book verbatim.

Whilst tight supply chains and labor markets are creating rising inflation, within the US economic hinterland, global headwinds are also blowing growth headwinds in addition to the combination of inflationary tailwinds and headwinds.

Reading between the lines, of the Beige Book, a more cautious, and nuanced, approach to monetary policy tightening is required. This contrasts with the FOMC’s current, alleged, zeal for racing back to neutral, and beyond, with 50-basis points plus rate hikes and balance sheet reduction.

· The recent Wall Street earnings season-wink signals that the US financial sector has, already, become the medium of economic transfer of the FOMC’s “methodical” and “expeditious” tightening which has only just begun.

(Source: the Author)

The pessimistic regional message was then re-iterated, with brio, by the regional commercial banking sector. This Regional Blink should be placed alongside the preceding Wall Street Blink noted in the previous report. The financial sector is sending clear warning signals.

The warning message clearly states that the FOMC risks triggering a recession with an aggressive monetary policy tightening schedule.

The FOMC, for its part, has responded with procrastination rather than the kind of alacrity that will interdict a recession.

Methodical, expeditious, and purposeful procrastination ….

Fed Governor, and nominee Vice-Chair, Lael Brainard has added some new words to her monetary policy role play. Ostensibly, monetary policy will be tightened “methodically” and “expeditiously” going forward. Exuding such confident signals may evince a safe pair of hands that expedites her nomination at a more than methodical pace.

(Source: the Author)

At the last Lael Brainard Word count, this author had counted two adverbs in the growing list of FOMC guidance on how monetary policy will, allegedly, be tightened.

The two adverbs, methodical, and expeditious have now been conjoined, with the word “purposefully”, by San Francisco Fed president Mary Daly. Apparently, this extending vocabulary will bring the FOMC to the neutral rate, by December, possibly, with some purposeful 50-basis points rate hikes along the way. Presently, Daly is keeping her next adverb on hold, since the “open question”, of whether to hike rates beyond 2.5%, is conditional upon the incoming data.

Actions speak louder than words, especially when the wording has become bloviate. The risk of underwhelming, similarly, grows without action, and with it the loss of credibility.

*Note to this Author: Brevity is the “methodical” soul of clarity ….

Presumably, worried that this focussed message had initially been missed, in the mass hysteria of rising bond yields, Mester then repeated herself with emphasis on the benign economic outcome. She may have to keep repeating herself since the hysteria is garnering more attention than her guidance.

(Source: the Author)

Basis the rising market hysteria, in no short part due to the procrastination, as well as the Hawkish milieux, of the FOMC, Cleveland Fed president Loretta Mester is struggling to be heard.

In addition, to repeating herself, Mester is now plaintively trying to broker a consensus, from her colleagues, which is perceived positively by Mr. Market before he delivers a bigger monetary policy tightening than the Hawks envisaged.

The plaintive Mester is using a combination of brevity and clarity, in order to achieve her purpose. Consequently, procrastination has been limited to the adverb “methodical”. In addition, “methodical” has been clarified as a 50-basis point rate hike, in May, with increments no larger than this going forward.

Do no harm: The “Bostic Put” is now out there ….

Presumably the Sticky versus Flexible CPI divergence, as the harbinger of consumer retrenchment, published by his own team, has prompted Atlanta Fed Raphael Bostic to flash his own version of the “Fed Put”.

Like the “Rehnfeld Put”, the “Bostic Put” is a promise not to tighten too far, rather than a promise to ease swiftly.

Bostic has described his version as contingent upon his reluctance “to really declare that I(Bostic) want to go a long way beyond our neutral place because that may be more hikes than are warranted given the economic environment.”

Straight outta here, is the sensible way to go ….

The last report observed the conflicted agonizing of Chicago Fed president Charles Evans. Presumably, since Evans has to live, and work, in the spiritual home of Monetarism he is obliged to confront his demons on a daily basis. This inner conflict seems to be taking its toll on Evans’ health and guidance.

Fortunately, for Evans, he will be retiring sooner than is mandated. Evidently, he has had enough, and/or, he doesn’t want to be around for the proverbial shitstorm, that is going to break, as the Fed’s handling of the economy gets investigated by lawmakers.

The list of Fed presidents, and Governors, who are bailing early, or being forcibly bailed, is getting almost as long as the length of the adverbs in the procrastination which serves as their guidance. There’s definitely trouble at ’mill based on this observation.

In the last report, Evans was living, and talking, vicariously about arriving at a neutral rate of 2.25-2.5%, without hiking by 50-basis points unless he had his arm twisted. Evans now accepts the premise, and execution, of 50-basis point rate hikes, but would rather be living in the future, of December 2022, when the inflation picture is better understood. Since he is retiring early, his longing for this vicarious pursuit of monetary policy tightening should not come as any surprise. Sadly, however, he may be thinking more about himself than the US economy. This premature abandonment of duty does his reputation and legacy no service at all.

Unfortunately, furthermore, Evans has, also, accumulated the dubious kudos of adding another adverb to the extended list in the FOMC’s extended forward guidance on the verb to tighten. The newest adverb, “sensible”, was unleashed during a cozy, remote, fireside chat with Adam Posen. An adverb a day keeps the real tightening away.

We may remember Evans, sensibly, when he retires.

Trying, and failing, again, to do no harm to one’s credible commitment ….

· Neel “Ex Culpa” Kashkari has lost his credibility.

(Source: the Author)

Since his apology, for spectacularly calling inflation wrong, Minnesota Fed president Neel “Ex Culpa” Kashkari has been looking for scapegoats. Initially, he blamed the domestic economic agents of the US economy for his embarrassment. Now he has spotted some foreign agents to scapegoat, rather than getting his eyes and ears tested for aberrant perceptive faculties.

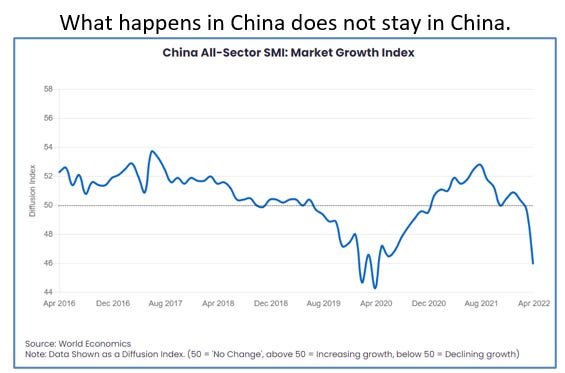

Kashkari’s newest observed scapegoats are global. Ukraine is an obvious scapegoat. This author is more interested in Kashkari’s scapegoating of China since it confirms a long-held view that what happens in China, does not stay in China when it comes to what happens in the United States going forward. Evidently, this is also the view of IMF Managing Director Kristalina Georgieva who recently opined that a slowdown in China’s economy represents a global threat.

Unfortunately, Kashkari sees both the Ukraine situation and the Chinese COVID-19 situation as inflationary reasons to tighten monetary policy. Since he failed to call inflation right, he is now determined to call it; even when it portends an economic headwind. Since he failed to call inflation, it is, perhaps, no surprise that he should now fail to call economic growth right, also.

Kashkari is not the only FOMC member, with dodgy credible commitment, who this author is re-evaluating for an upgrade. Like-mindedness, with oneself, is, however, a poor reason to ascribe virtue to others so the author remains cautious.

Empathy with the Rate Hike Devil ….

· James Bullard no longer has credibility.

(Source: the Author)

This author has no sympathy for St Louis Fed president James Bullard’s failure to address inflation, earlier in March 2021, and then to, belatedly and, theatrically overreact. This author must, however, admit to empathizing with Bullard’s current and future predicaments.

· The 1990s global economic scenario is hiding in plain sight.

(Source: the Author)

The author must also admit that his sense of empathy is imbued with self-gratification at the prospect of Bullard’s guidance being perceived, in the same frame, as the thesis in these reports. This author has suggested that the 1990s is an economic model hiding in plain sight for central bankers.

This 1990s model has now been noted and proselytized in at least one of the top financial media sites, even down to the year 1994 previously highlighted by the author. Bullard himself is also rhetorically going back to the ’90s in his forward guidance.

#1994Playbook@Macklem Doctrine, a #NewWorldOrderAssetBubble follows ….

This author would like to point out that the original 1994 Playbook set the stage for the Dot.com Bubble that followed. Buying the current dip, if one is following the 1994 Playbook would make sense. Once bought, it is, however, better to travel than to arrive at the end of the bubble that ensues.

(Source: the Author)

This author had, previously, opined that readers/traders/investors should remember the Dot.com Boom and the Millennium Bust that followed when this process was originally followed. A quick look at Bitcoin may inform this parallel reference viewpoint further.

Unlike this vainglorious author, Bullard is happy to give all the credit for his thesis to Alan Greenspan. Of future irrational exuberance and pessimism, from the repeat of the said 1990s model, Bullard opined that Chairman Greenspan “set up the U.S. economy for a stellar second half of the 1990s, one of the best periods in U.S. macroeconomic history.” Crypto Bulls, should once again take note.

“SWIFTLY” Building Back A 1990s Better Inflation And Growth Story Than The 1970s And 1980s Models

(In their haste, to get back to the 1970s, and 1980s commodity and inflation shocks, commentators, and analysts, seem to have forgotten the 1990s.)

· As went Saddam’s Iraq, so goes Putin’s Russia.

Those riveted to spiking oil and commodity futures prices, on their screens, should remember that the complete opposite occurs in the real world in times of crisis. President Putin is starting to resemble Saddam Hussein. It is no surprise that many of the current Russian Oligarchs learned their trade in the 1990s. A return to this status quo would not overly concern them. Russian assets and presidents change, in times of crisis, but the oligarchy structure remains. In fact, it can be reasonably argued that the oligarchy structure is enhanced by said changes.

(Source: the Author)

Patriotism, and no lesser fear of incarceration, demands that no sympathy, or empathy, should be shown toward the Bank of Russia, even though its “reverse industrialization” thesis is also rhyming/repeating with this author’s 1990s thesis. Bullard may feel similarly inclined towards his Russian nemesis with the same historical perspective.

Bullard has also, cleverly, used his panegyric for Greenspan to frame perceptions of his own soliloquy to be behind the yield curve, or not to be. If you ask John Taylor the answer is yes. But if you were to ask Bullard the answer is not by much. Bullard’s tiny negation is based on his treasured assumption that the FOMC has retained all of its inflation-fighting credibility during the rise of inflation since Spring 2021. One man’s assumption may be another man’s over-confidence cognitive bias.

Why Bullard would think that the FOMC has any credible commitment left, after this current inflation debacle, is mystifying. To be behind or not behind, the yield curve is not the question. To have credible commitment, or not, is the real question.

Despite his dodgy credibility, Bullard is still deserving of some modicum of kudos for his sheer chutzpah in the loyal service of hunting danger to the Fed as an institution.

Fool me once, shame on you, etc., etc.(sic)

· The “Waller Put” signals that the FOMC will not kill the “Build Back Better” and “Make More In America” booms.

(Source: the Author)

The last report observed the FOMC’s growing “do no harm” consensus drifting, further, towards the “Waller Put”; based on the Fed’s self-preservation instincts and a lot of unrealized bond losses on its balance sheet. The report also observed that this “do no harm” bias may result in worsening inflation; as President Biden Builds Back Better and Friend-Shores supply chains, with brio, before the resulting supply-driven disinflation occurs.

· The Macklem Doctrine of America’s global imperative may make bigger fools out of the FOMC than the incoming inflation data.

(Source: the Author)

It has also been noted that the US global imperative may make fools out of the FOMC. James Bullard is increasingly desperate not to be made a fool of, again. Presumably, this is also why Bullard is heaping praise on Alan Greenspan and what he did in 1994. Consequently, Bullard now talks loudly of 75-basis point rate hikes.

The limits of US monetary policy have been neatly circumscribed by the US global imperative.

(Source: the Author)

Presumably, Bullard remembers the massive fiscal expansion and Vietnam War period that led to the Volcker Era. Evidently, he would like to have a mini-Volcker Era, right now, as Greenspan is alleged to have done in 1994.

The reader should also remember the Latin American debt crises that ensued from Volcker-Era rising interest rates. After remembering this time, the reader should then revisit this author’s quest for a new Bay of Pigs era in the region.

Day-O, Day-O, Daylight Come: Black Gold, Banana Republics and Old Habits ….

The American thirty-year narrative involves the funding and creation of a bipartisan consensus from the perceived Chinese threat via Latin America.

(Source: the Author)

The last report updated on the potential for an imminent Bay of Pigs moment in South America. The threat level was raised in relation to Nicaragua’s elevation to a significant regional threat status by the State Department.

What Do Fed Monetary Policy, Common Prosperity, A Bipartisan Republic, Some Banana Republics, And A Bitcoin Republic All Have In Common?

Dec. 12, 2021 2:12 PM ETBTC-USD, BTCE-USD, TLT

(Source: the Author)

This author has also, previously, noted the conflation of the risks associated with Cryptocurrency into the South American geopolitical narrative. At the recent Spring Meetings, the IMF has also causally linked the crypto-threat directly to the global narrative. The IMF has opined on the threat of nations using their energy resources to mine cryptocurrency and also to derive fiscal revenues from the process. Clearly, Russia is the first target of global enforcement, however, this logically will also apply to other nations who choose not to become trusted “friend-shorers”.

Some of the infamous Banana Republics in Latin America are blessed with hydrocarbons. This feature makes them of strategic interest as G7 nations look for alternatives to Russia’s hydrocarbons which are exclusively heading East to China. The blessing is hence a curse.

China’s top offshore oil and gas producer CNOOC Ltd, a partner in ExxonMobil’s Guyana operations is preparing to exit its businesses in Britain, Canada and the United States, because of concerns in Beijing the assets could become subject to sanctions, industry sources told Reuters.

As it seeks to leave the West, CBC (Canadian Broadcasting Corporation) said that CNOOC is looking to acquire new assets in Latin America and Africa, and also wants to prioritize the development of large, new prospects in Brazil, Guyana and Uganda.

(Source: stabroeknews)

Guyana is either blessed or cursed, by the fact that it has been the beneficiary of the largest offshore hydrocarbon discovery of the last decade.

Guyana is currently re-evaluating its strategic options, and partners, for the development of its abundant offshore hydrocarbon reserves. Currently, Exxon is the major, and China’s CNOOC is the minor “strategic partner”. Clearly, these two strategic partners are under evaluation and consideration.

China’s CNOOC is positioning itself to become the exclusive “strategic partner” at a time when the Guyana government is trying to squeeze out Exxon. CNOOC is, in fact, divesting its Western assets, which fall under direct G7 purview, in order to invest in Guyana.

Should CNOOC be successful, it will require a massive maritime military operation by China to secure the position. This author would, thus, say that the level of estimated probability of a Bay of Pigs moment in Guyana is rising significantly.

(Source: bbc)

The picture in Guyana is further muddied by the fact that it is a Commonwealth member state. Given the current travails of the UK, outside the EU, and its increasingly desperate Prime Minister, Guyana’s anticipated Bay of Pigs moment could quite easily be preceded by a Malvinas Moment.

From his bunker, the PM is certainly putting some colonial spin on things. His delivery might be a no-ball though.

Bridgerton Revisited: “Now in Injia’s sunny clime, Where I used to spend my time ….”

The vote-calculating, culturally-obtuse PM recently chose to rekindle the flames of Partition by athletically disporting himself at a manufacturer of machines, which are used to demolish Indian Muslims’ homes, during the Holy Month of Ramadan. Well, “they” all vote Labour, don’t they?

· The UK will become an austere economy with an ungovernable polity.

(Source: the Author)

Partition of the Union, and the Commonwealth, may await the PM’s return to Blighty. Buckingham Palace has been informed, and is closely monitoring the situation.

Further pressure, on the PM, is about to come as it dawns on the British electorate that the new IT jobs, effectively being taken from EU workers, post-Brexit, will be given to Indian workers rather than newly enfranchised (and still unemployed) Tory voters (formerly Labour voters), from Up North, beyond the Red Wall.

Apparently, “they” are not all coal miners and/or scroungers, Up Yonder, as is fondly believed at Number 10 and Number 11, after all. As it transpires, there actually are some of the world’s most advanced IT hubs located Up Yonder. Salaries, Up Yonder, are also very competitive, even by emerging markets standards.

So, cui bono?

The UK’s new IT jobs won’t be going to Ukrainian immigrants, for sure, because these new arrivals are being swiftly emigrated to, what appear to be “detention centers”, in the former killing fields of Rwanda. This re-migration stat may pacify the inquisitive Northerners, but it is doubtful. They may be more interested in the continued buy rating (especially from Goldman) on Infosys shares (INFY), despite its poor earnings report and slide in share price, and the Alpha attributed to the company in Mrs. Sunak’s portfolio. Is there a big global deal in the pipeline?

It’s still grim Up North, and getting grimmer, by the day, for the PM. Perhaps it’s time for Chancellor Sunak and Secretary Patel to “do one”, as they say in Manchester, before questions in the House, about the correlation of events, on this timeline, start to paint a causal picture of political motive, opportunity, and means. Placing lots of fracking rigs and nuclear power stations, Up North, may just foment the coming rebellion.

There are other strategic British interests who, evidently, now deem the Commonwealth and the Union to be under attack. Two senior members of the British Royal Family, recently, completed a Caribbean reconnaissance mission; and found evidence of a significant Chinese attempt to build a bridgehead, on the rubble of Britain’s slave-owning foundations, in the region. Back in Blighty, a reconnaissance mission, in search of Northern Chinese Fifth Columnists, in the fish and chip shops, beyond the Red Wall, is now being anticipated. The Duke of Sussex’s recent cryptic comment, about making sure that grandmama is “protected”, has suddenly taken on a new strategic meaning.

“Friend-Shoring”, whilst trying to climb The Greasy Pole, on the margins, in former colonies, and former constituencies, can be a complicated affair. The IMF has not placed the UK at the bottom of the developed economy growth league table without good reason. IMF bookmaking pundits have wagered that, whilst the UK economy may not be the worst developed economy, in the relegation zone, it is in the bottom one. Sadly, Brexit-tied potential new managers, Guardiola and Klopp, are unavailable to manage the team in the relegation battle ahead. The current manager is guesting on an away day in India. The drop is imminent.