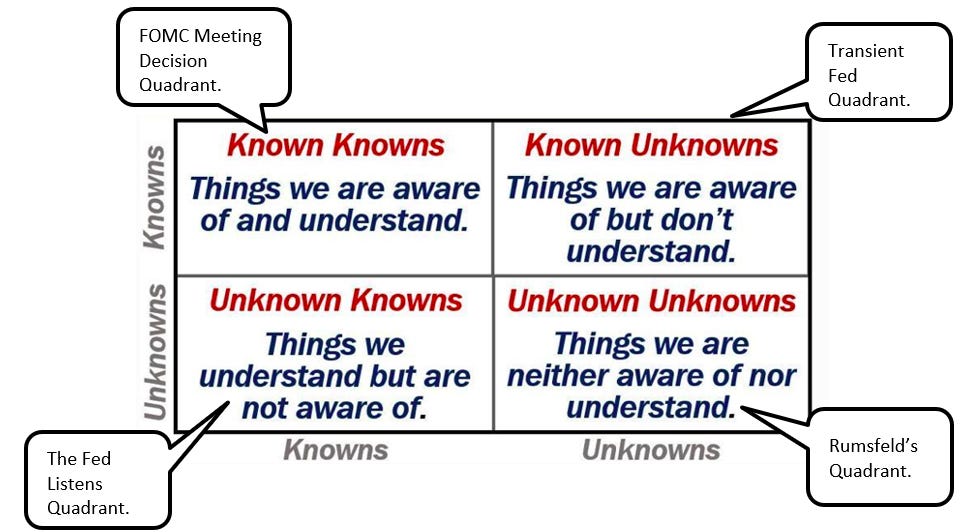

The Fed Is Not Alone In the Rumsfeld Quadrant

“But there are also unknown unknowns- there are things we do not know we don’t know.” (Donald Rumsfeld)

Summary:

· Central bankers are admitting their failures, by varying degrees, to pave the way for more failures.

· The Fed is pretending to be in Rumsfeld’s Quadrant of Financial Instability by accident.

· The Fed has deliberately understated financial instability risk because to correctly address it would mean immediately easing monetary policy.

· The Fed dreams that it can officially prorogue financial instability risk for another six months.

· Mary Daily’s Insolvent Munchkins have pivoted from Incremental QT to QE.

· John Williams tries to anchor the pivot in the Rumsfeld Quadrant by making it appear to be in the Known Known Quadrant.

· If the Fed behaves typically the next QE will be “Front-Loaded”.

· (Lorrie) Logan’s Run leads to nowhere other than to more monetary policy easing.

· The KCF’s ancient incremental guidance is justified by the changing inflation picture.

· The KCF is Constitutionally Compliant with the tighter partisan US political environment and thereby independent from it.

· Le Bromance makes Le Butler cater exclusively to Western Alliance VIPs.

· The global example of the rational response, of the Neo-Classical Japanese consumer, to inflation, completely confounds the rationale behind the global central banking communities’ aggressive inflation fight.

· The ECB’s, alleged, soon to be shrinking, balance sheet is in conflict with the expanding balance sheets of the Eurozone national central banks, which comprise it, which will lead to a financial stability crisis.

· History is rhyming again in Germany’s Rumsfeld Quadrant of the Eurozone’s next down-round capital raising event.

· German Economic Blitzkrieg may be found in the EU’s Rumsfeld Quadrant.

· Crypto is in the Rumsfeld Quadrant and policymakers and central bankers are happy.

Long-COVID Confessions of a Central Banker ….

The truth will always out.

· Global central banks have been insolvent for, a lot, longer than people think.

(Source: the Author)

Depending on the degree of transparency, and democracy, in their countries, central banks are now admitting to their failures during the COVID experience. These mea culpas appear to be, causally, linked to the level of losses on central bank balance sheets. One senses that questions are being asked, and fingers are being pointed, in the corridors of power. Elected policymakers want to start fiscally stimulating their voters, to vote for them, and central banks are dreading the prospect.

Last week, the Swiss National Bank admitted that it has been skint and potentially insolvent for most of 2022. This potential insolvency comes from the monetary policy tightening against the inflation from the previous COVID easing.

The Bank of England’s Chief Economist says, in luxurious hindsight, that its massive monetary policy easing was not needed. Well, he would, wouldn’t he, because he wasn’t at the Bank when it was massively easing. History is kindest to those who rewrite it.

The Reserve Bank of New Zealand now says that whilst its massive easing was necessary, the ensuing monetary policy tightening should have started sooner.

The BOJ, bless it, is unashamedly unrepentant and just lest sleepy easing dogs lie.

· Global central banks will have to start easing a lot sooner than they and people think.

· The attempted Soft Landing by the insolvent RBA is the financial stability policy canary in the developed economy coal mine.

(Source: the Author)

This author cannot help thinking that the central bankers are in a hurry, to dish out apologies, so that they can prepare to ease again.

The Reserve Bank of Australia certainly appears to be in a hurry, to wrap things up, with its latest guidance.

Even though her Chief Economist is circumspect, about the last one, Bank of England Deputy Governor Sylvana Tenreyo is already speculating about the need for rate cuts, in 2023, in response to the recession that she and her colleagues are about to unleash.

Thus, one can see an exculpatory pattern of communication about prior failure and the desire for more failure. This communication was taboo until the Fed started piling on the “Front-Loading” agony.

At the epicenter, of apologies, denials, and promises, the Fed is in a curious zone of its own.

There are lies, damned lies, and the Fed’s semi-annual Financial Stability Report ….

Given the performance of Fed Chairman Powell, to date, one could argue, with sincerity, that Donald Rumsfeld would have made a better Fed Chair. At least Rumsfeld was humble enough to admit that there are unknown things that he does not know about.

Chairman Powell purports to be omniscient, despite the fact that he was once a failed inflation transient. Powell conflates his assumed omniscience with the presumed omnipotence of his position.

· The Fed is not committed, it is as inert as ever.

· The Fed does not know what lagged economic outcome from an initial belated, historical, monetary policy overreaction it has recently overreacted to.

(Source: the Author)

At his last FOMC presser, Chairman Powell chewed the heads off those journalists who adumbrated the unknown-unknown start of the Fed pivot. Apparently, Powell knows enough to continue tightening monetary policy. Sadly, he did not know enough about the inflation, that he is now certain about, back when he was certain that it was transient.

Powell appears to conflate awareness with understanding.

The FOMC, purportedly, makes decisions based on Known Knowns. The Fed’s Transient Inflation Mistake must have, then, by default, been made about a Known Unknown. The author would put the abortive Fed Listens initiative into the Unknown Knowns quadrant. The author would say that the Fed enters Rumsfeld’s Quadrant of Unknown Unknowns, periodically, because it has created this place through an observable process of the previous overreactions, to the Known Knowns, combined with policy executing inertia.

Currently, the Fed is pretending to be in the Rumsfeld Quadrant of Financial Instability by accident. The Fed, however, knows how it got there. It got there via the Transient Known Unknown Quadrant into the Known Known Quadrant. Inertia and overreaction in the Known Known Quadrant are forcing the Fed to pretend that it is accidentally entering the Unknown Unknown Quadrant. The good thing about the Unknown Unknown Quadrant is that one can be blameless for mistakes.

Thus, the Fed can deny all responsibility, for its actions to date, and any actions that it may take going forward. This lack of accountability is the beauty of central bank independence. There is no free lunch, however, and this beauty comes at the cost of the permanent disfiguring loss of credibility. It’s an ugly business, being a central banker, these days, and the Fed is one of the ugliest central banks, if not the ugliest.

Powell, and his team, would seem to need an inordinate amount of time to become aware of something that they can then overreact to.

The last report discussed how, and why, the Fed, is, incrementally, sleepwalking into a policy mistake, that it will not acknowledge, for some time, and will then overreact to.

Richmond Fed president Thomas Barkin has a new adverb for the incremental mistake. According to him, the Fed will “persist”, thereby, elevating the probability of a mistake.

The recent release of the Fed’s semi-annual Financial Stability Report was a classic example of this inert internal reaction function. The report and its presentation, by Vice Chair Brainard, was loaded disingenuously. Needless to say, despite all of the demonstrable, daily, volatile evidence, that states otherwise, the Fed does not believe that financial stability is a problem. To admit to it would be to admit to having a hand in it, just like admitting to having a hand in the creation of inflation. The Fed is just rewriting history to save what is left of its dubious credible commitment.

From this author’s perspective, the Fed, with exception of one individual regional president, is all out of credibility.

The report itself was borderline fictional. Rather than focus on recently elevated risks, the report took a backward-looking historical perspective, that diluted the threats. It was impossible to say that there is no financial instability threat because there is too much evidence that there is. Instead, the risk was downplayed as containable and contained.

Companies can no longer use leverage to fund investor returns. On the contrary, companies now need investors to provide them with pledged cheaper equity capital in lieu of expensive debt capital. Pledged equity investors are now on the hook as debt capital investors stand ahead of them, in the capital structure, awaiting the insolvency trigger. TPG, a barometer of health in this sector recently reported a 60% drop in earnings, as exits for its portfolio companies vanished.

In the face of looming corporate insolvencies, the Fed simply decided to downplay the headline financial instability threat. Over half of the participants surveyed explicitly cited poor capital market liquidity as a "salient risk". This consensus wasn’t even mentioned in the report. This is a clear red flag that basically undermines the value of the financial stability report in its entirety.

These “deferred out of thin air assets” are then layered with US taxpayers’ funds, in the form of US Treasury securities, on the Fed’s balance sheet. The layered proceeds are then integrated, into the real economy, through the Federal Reserve Bank system, by the injection of bank reserves, which are then multiplied through fractional reserve banking. The potential crime of wire fraud is also palpable in this process.

(Source: the Author)

The Fed seems to believe that since it is insolvent, and, allegedly, can get away with it, and the money-laundering insolvency mitigation process, this makes the whole US financial system similarly immune.

So, based on the fictitious financial stability report, and Brainard’s dissembling cover story, the Fed, in theory, can pretend that there is no financial stability problem for at least another six months. This author would say that this proroguing, of the financial stability threat, has been deliberately done to fit the guidance, and timeline for the Fed’s current monetary policy tightening schedule.

Thus, financial instability has been deliberately ignored, thereby, highlighting that it is, in fact, the greatest threat to the US and global economy. To apply Rumsfeld Doctrine, financial instability is an Unknown Unknown.

An admission that financial instability is a significant current threat would be an embarrassing admission that the Fed should, actually, now be looking to ease monetary policy. Such an admission would be the final nail in the coffin for Powell et al, excluding the brilliant Esther George.

The only good news is that the Fed has moved from “Front Loading” to incremental tightening.

It may be too late, however, for the most at-risk members of the American family.

13 is Unlucky for Some ….

Some readers have struggled with the significance of the 13th Amendment in the last report. This struggle reflects an ignorance, of the importance of the 13th Amendment, in relation to the current level of partisanship and the rezoning of certain voting districts to nullify the amendment’s impact on the democratic voting process. The Mid-Terms have been very much about the 13th Amendment, even though the politically correct American news media has avoided calling this spade a spade.

The amendment is of great significance in five Black Belt States. In these states, the preservation of Jim Crow legislation, and customs, broadly excludes those Americans who have also been excluded from participation in the economy. These broadly excluded are still treated like property and economic resources rather than economic agents. This treatment and exclusion are even more egregious when it is practiced by members of the Federal Reserve.

· The Fed Listens initiative does not make the Fed compliant with the 13th Amendment.

(Source: the Author)

Two Fed presidents, who should know better, for patently obvious reasons, have ignored the commentary and opinion, from the Black Belt, in relation to monetary policy settings. The Fed Listens initiative, hence, then, becomes nothing better than window dressing in relation to this at-risk ethnoconomic minority. In this author’s view, these two Fed officials are in breach, of the 13th Amendment, by their failure to accommodate the views of the Black Belt into the monetary policymaking process. If they are in default, then so it’s the Fed by association.

On the other hand, President Biden listens, attentively, to ethnic minorities. This is why he was elected. Hence, as the Fed raises the cost of student debt POTUS cancels it. POTUS will have heard, what the Fed has, recently, ignored, and will mobilize pressure on the Fed, to listen-up, as he approaches the re-election treadmill.

(Source: the Author)

This author suspects that the Fed is going to feel the heat, from POTUS, in relation to its, alleged, 13th Amendment compliance breach. The author also suspects that, by then, the Fed will have stopped tightening and started to talk seriously about easing.

Goodbye Yellow Brick Road ….

San Francisco Fed president Mary Daly had been observed to be playing the Wicked Witch of the West, to Kansas City Fed president Esther George’s Glinda, when it came to the dark arts of monetary policymaking spells. “Front-Loaded” Daly seemed rather bitterly opposed to George’s Incremental spells.

Daly’s Munchkins were, however, seemingly, more responsive, to George’s incremental spells, thereby, making it difficult for Daly to continue with her “Free Loading” one. Daly’s Munchkins have recently moved further down the Yellow Brick Road, of monetary policymaking, towards the Emerald Green City of more QE. A recent weekly staff report finds that financial conditions are already consistent with a Fed Funds Rate of circa 5.25%.

· Global central banks have been insolvent for, a lot, longer than people think.

· Global central banks will have to start easing a lot sooner than they and people think.

(Source: the Author)

Daly’s Munchkins also find that financial conditions have been tighter since late 2021. As noted, by this author, in the last report, the Swiss National Bank’s balance sheet losses were set at nine months old. This would put the duration of monetary policy tightening much longer than is currently assumed. This also puts the point of the next monetary policy easing much nearer than is currently assumed. Daly’s Munchkins have, therefore, confirmed that the losses in risk assets, and central bank balance sheet assets, have been tightening financial conditions for much longer than is currently acknowledged.

Daly’s Munchkins also support this author’s view that inflation, itself, tightens financial conditions. Hence inflation has already been doing the Fed’s tightening for it. With inflation running above 7% this tightening is significant. This may significantly obviate the need for aggressive monetary policy tightening by the Fed. It certainly, obviates the need for “Front-Loading”.

· The Fed is not committed it is as inert as ever.

· The Fed does not know what lagged economic outcome from an initial belated, historical, monetary policy overreaction it has recently overreacted to.

· Based on its lack of policymaking situational awareness the Fed is well-advised to move from “Front-Loading” to Incrementalism.

(Source: the Author)

Mary Daily’s Insolvent Munchkins have pivoted from Incremental QT to QE. The big question is whether this new QE will be “Front-Loaded” or Incremental. If the Fed is smart, like Esther George, it will be Incremental. But, as this author notes, the Fed always, belatedly, overreacts.

Daly, herself, is some way behind her Munchkins. She does not believe that financial conditions are “Munchkin Tight”. Evidently, she thinks that conditions are a little tighter than, before, when she was a bitchin’ “Front-Loader”, however, since now she has gone Semi-Incremental. In this contorted position, she can still aim for a target Fed Funds rate close to 5% but will just take longer to get there.

This author has referred to Cleveland Fed president Loretta Mester as a “barbarous relic” by nature of her dogmatic tightening inertia. Mester continues to defy this author and the incoming data. She has, however, redefined herself, presumably, as a prelude to more radical surgery.

diligent (adj): having or showing care and conscientiousness in one’s work or duties

(Source: Cleveland Fed English Dictionary [CFED])

Mester now defines herself as diligent. This author has heard this one before. It belongs on the same shelf as Transient. Whenever the Fed is being inert, in the wrong policy direction, Fed speakers raid their dictionary, and thesaurus, for unscientific euphemisms which are less self-critical. Thus, Mester’s inertia is, allegedly, diligent. Consequently, she undoubtedly intends to redefine herself as diligently in favor of stimulus when her current diligence has tipped the economy into recession. The Fed could, should, and can do much better than this extreme kind of diligent ex post facto blunt trauma.

When it comes to Free-Loading, Front-Loading Minneapolis Fed president Neel “Ex Culpa” Kashkari is the Cowardly Lion from the author’s dream. Cocooned, in his comfort zone, Kashkari has decided to become a passive/unaggressive Front-Loader, to avoid embarrassment in another financial crisis. Thus, rather than the say that he believes in Front-Loading, he now says that he doesn’t believe in pausing monetary policy tightening. What this demonstrates is that Kashkari is not certain about growth and financial stability anymore. Rather than deal with this uncertainty, he prefers to say that he is certain about high, intransient inflation.

(Source: the Author)

Minneapolis Fed president Neel “Ex Culpa” Kashkari seems to be growing into his, author-imagined, role of the Cowardly Lion as though it was his nature. This role does not oblige him to make predictions or offer any meaningful extended forward guidance, so he no longer has to apologize when he gets it wrong. Kashkari’s latest timid communication identifies him as still scared to pivot even though committed to trying to land the US economy softly.

There are some who are less afraid to pivot.

Hello, Confused Pivoting Sailor ….

New York Fed president John Williams is slightly less timid, about pivoting than the Cowardly Lion, although one would not say that he is easing like a drunken sailor just yet.

Williams is pivoting around what he believes is the firm anchor of flaccid long-term inflation expectations. According to Williams, these flaccid longer-term inflations are not too far away from the Fed’s droopy target.

Williams is, hence, anchoring his pivot in the Rumsfeld Quadrant by pretending that he is in the Known Known Quadrant. He knows that long-term inflation expectations are well-anchored so, allegedly, he can pivot. What is, in fact, happening, in practice, is that Williams is drowning in the Rumsfeld Quadrant with each 75 Basis-point rock of rate hikes.

Williams is also surprised to see some recession/depression expectations creeping into the professional economic forecasts that the Fed relies upon. Why he is surprised by this is perplexing after the Fed has piled on the tightening headwind when the inflation headwind is already approaching double digits.

Williams has tried to pivot using data, forecasts, and expectations. He should be very careful because the Fed and professional forecasters are rubbish at making forecasts. The whole Transient Inflation debacle is a testament to their rubbishness.

If Williams is sincere, about being rigorously analytical, he should construct a Confusion Matrix using the forecasts of GDP and inflation, by the Fed’s professional forecasters, as the data to be analyzed. True Positives and True Negatives could then be assigned to what the forecasters predicted and got right. False Positives and False Negative could be assigned to what the forecasters got wrong.

Williams may find that the measures of Accuracy, Precision, and Recall, in relation to the validity, and utility, of the forecasts, that the Fed uses, are rubbish. He should therefore be careful about presenting himself, and the Fed, as rationally efficient data analysts. Perhaps he already has, run his own Confusion Matrix, so that he is just fudging his results by saying that long-term inflation expectations fit his subjective decision to attempt the pivot.

Richmond Fed president Thomas Barkin is not on board with the pivot. In his view, the Known Known is high inflation that may un-anchor benign longer-term inflation expectations.

This dissonance between Williams and Barkin illustrates just how poor the Fed’s forecasting abilities are.

Philadelphia Fed President Patrick T. Harker is moving through the pivoting gears. Currently, in first gear, he initially seeks to rewrite the economic history, that we have all lived through, in order to minimize the blame, on the Fed, for the inflationary situation that we are all living in. His historiography is a mixture of pandemic, war, pro-cyclical fiscal, and monetary stimulus which have conspired to create aggregate demand in excess of supply. It’s not quite as bloviate as War and Peace, or this author’s reports, but it is getting there in spirit. In the final chapter, the Fed can move from “Front-Loading” to Incrementally landing the US economy in the Soft-Landing happily ever after. It’s a cute story, that ignores the reality as witnessed by all of us.

Oops! She blew it (the headwind) ….

Whilst Dallas Fed president Lorie Logan is new to the job, she is a seasoned Fed operative. She should, therefore, understand the risks of contradicting herself.

Logan recently opined that “high inflation is a drag on our economy”. She, thereby, admitted that inflation is a demand-side headwind, as this author says, that has been blowing away since inflation picked up in Spring 2021.

Logan then proceeded to put her other foot in her mouth by explaining that the Fed reacted, late, by blowing a further demand-side economic headwind. Apparently, there is a little more room in her mouth because she is not ready to pivot, just yet, based on one improved inflation data reading.

Two headwinds a Soft Landing do not make.

Two headwinds, Fed insolvency, a financial instability crisis do make.

· Central Bank insolvency is aligning with fiscal insolvency at a rapid pace in the global economy.

(Source: the Author)

Going forward, this author will enjoy watching Logan remove her two feet, and two headwinds, from her mouth, and the US economy, respectively, as she navigates the pivoting agenda.

· Stagflation has become Stabflation.

(Source: the Author)

(Lorrie)Logan’s Run does not seem to fit the 21st Century of economics which beckons. It belongs to the Volcker Era. In the new world, Stagflation has become Stabflation, and the Fed has made itself insolvent. To “Renew”, the Fed will need to monetize a new fiscal deficit, in order, to cover its balance sheet losses, and to re-energize the US economy. Logan is currently making the Fed more insolvent, and the Stabflation worse.

“Perfect pleasure”, in the new economy of the future may, however, be found, in Kansas, of all places.

She’s Justified and Constitutionally Compliant ….

As observed, previously, in this report, in the even more partisan post-Mid-Term polity it will be necessary for the Fed to be compliant with the 13th Amendment. By default, this means that the Fed will have to be Constitutionally Compliant in all respects.

The “perfect pleasure” that the Fed can derive, by way of its independence, therefore, depends, directly, on being Constitutionally Compliant.

Based on this author’ designed precept it is reassuring to know that, at least, the Tenth Federal Reserve District is Constitutionally Compliant. Maybe the Federal Reserve Board should relocate there, away from the partisan battleground of Washington.

Through all the latest market euphoria, and hurried incremental pivoting by her wrong-sided colleagues, Kansas City Fed (KCF) president Esther George remains the doyenne of incremental consistency that central bank credible commitment is built on.

George’s guidance is justified, and it’s becoming ancient. Her wisdom remains eternal.

In light of the latest incrementally improved inflation data, George framed the epiphany as consistent with her strategy of incremental rate hikes going forward. Inflation remains closer to 10% than to target, so there can be not let-up. However, based on the improvement, and lagged impact of previous rate hikes, incrementalism is the best option in her view.

· Free-Loading Chairman Powell’s position is untenable, ideally, he should be replaced, by Esther George, but this probably won’t happen.

· If the “Front-Loaders” finally listen to, and follow, Esther George’s incremental rate hike proposal, they may still be able to Soft Land the economy and avoid having to aggressively money launder the Fed’s balance sheet losses.

· Free-Loading Chairman Powell needs to grow a pair and use his casting vote magic to turn Front-Loading into Incrementalism.

(Source: the Author)

George is vindicated, but, she is not as vindictive as Powell and his, until recently, “Front-Loading Free-Loaders”.

In his latest Esther George panegyric, this author has found some more guidance features to eulogize.

This author is particularly impressed with George’s approach to the fact that high short-term inflation expectations are becoming entrenched. This entrenchment de-anchors confused sailor John Williams’s pivot. It is, therefore, imperative that it is addressed by someone at the Fed. Who better than Esther George?

George notes that this entrenchment, of high short-term inflation expectations, can only be overcome by productivity solutions, involving labor force training and education. Rather than kill the economy, and the training classes, with a recession, she intends to incrementally discover what the new market-derived cost of capital consistent, with an environment, that addresses the productivity solution is. She does not wish to threaten this price discovery process by overreacting and failing to include lagging rate hike impacts. Only a real central banker would understand any of this. George is consistent with the Fed’s dual mandate.

George is also consistent with the US Constitution. In the fissile partisan environment, in which the Fed operates, consistency, with the Constitution, is the only guarantee of Fed independence. The recent tight Mid-Term elections highlight how important it is to be Constitutionally Compliant. The Federal Government is now accepted as being “potentially divided”. Only a real central banker would understand this too.

As noted, previously, in this report, the Fed Listens initiative is not consistent with the Constitution. This is a problem for the Fed, that will be amplified, going forward, by the increased partisan environment of the tighter Mid-Term elections.

The tight partisan divide will also constrain the global polity in which America is “Friend-Shoring”.

Le Bromance du “Mondem” ….

· Behind Rishi’s great fortune lie Suella’s and Priti’s humanitarian crimes.

(Source: the Author)

The last report explained how, and why, Britain is rushing through its Bill of Rights legislation. In this author’s view, the strategic objective is to legalize the humanitarian crimes, that have been committed, against asylum seekers, thereby, conveniently evading having to answer to international courts of justice. Once one crime is able to go un-punished others will follow ad infinitum.

The government has recently demonstrated its haste, allegedly, because the nation is besieged by migrants. At the source of this migrant tidal wave, the UK PM was trying to surf the wave.

To slow the flow, of migrants, and to salvage the last remnants, of any kind of trade deal, with the EU, the PM has succumbed to the lethal embrace of President Macron. Even after spectacularly miscalculating, and failing, in an alliance with President Putin, President Macron still has ambitions for EU superpower parity with the USA. As we shall see later, perhaps his attention should be directed toward the old enemy across the Rhine.

Macron’s grand strategy is now in ruins. Furthermore, Macron just abused the President of the United States, for the second time, to try and get himself off the hook. Fool me Joe Biden once, shame on you, fool him twice shame on him. There will be no third time. Politically, and metaphorically speaking, the Island of Elba now awaits Macron.

(Source: the Author)

At some stage, of their bromance, therefore, the UK PM and Macron will have to agree on how they relate to the USA, in political and economic terms. Le Bromance will also have to deal with the most acerbic Brexiteers who will be watching the relationship blossom with extreme suspicion.

Ultimately, therefore, Le Bromance will be governed by the overarching EU/USA and the Brexit dialectics. Britain and the PM are, hence, the bridesmaids, and can never be the bride or the groom. Britain has, therefore, crossed the line into the global-macro obscurity realm of a bit player with a two-bit economy. The crossing of the line was originally done through what came to be known as the Butler Model and the VIP Lane of policymaking. Apparently, these two features are back. They are more likely to cater to the interests of America, and the EU, however, going forward.

There is some wider context to Le Bromance. Macron previously snatched away an Indian “Techno-Economic War” powerplay victory from the hands of “Les Sunaks”.

Anglo-French bridges are allegedly being rebuilt in outer space. Perhaps this is where Boris Johnson and President Macron should be sent to by President Biden. All levity aside, this latest information confirms the author’s “Sputnik Moment” thesis, quite literally.

(Source: the Author)

Back when Sunak was operating the Butler Model on the VIP Lane when he was Chancellor, his modus operandi was to turn the UK Treasury into an investment banking boutique. Interesting technologies, in government hands, were sold into private hands and then funded, via the UK Treasury, by the UK Taxpayer. Basically, the UK taxpayer lost IP in return for Zero Lower Bounds return on investment. The recipients of the leveraged rate of return, on cheaply acquired IP, made out like bandits. Bandit is a good name for them. The Butler Model and the VIP Lane also made sure that these private hands belonged to friends and family, quite literally in some cases.

The UK “Butler” has catered to the exclusive political, and financial, needs of a global elite. This report is specifically concerned with the “R”, the “I”, and “C”, in the “BRIC” nomenclature, of the said global elite, that the UK is “Butlering” for.

(Source: the Author)

Needless to say, some of the sensitive technologies were shared with/transferred to potentially hostile nations. Certainly, to nations hostile to America and the EU. This was the UK model, for the post-Brexit world, in which old Commonwealth ties would, allegedly, be exploited to keep the UK economy buoyant. The problem with this was that, in the main, the formerly exploited, former colonials, were the ones doing the exploiting, of their former colonial master, with a little help from former colonials in the UK Government.

· UK economic policy seeks to play the balance of power, by pivoting away from domestic Levelling Up, and the EU-USA NMWO, back towards a cocktail of good old Thatcherite austerity with a splash of Johnsonian Sleazez-Faire aka Ripping Off.

(Source: the Author)

In this reverse colonial exploitation, OneWeb found itself “privatized” into minority Indian and Chinese hands. The majority UK Government hands continued to plow UK taxpayer funds into this IP transfer vehicle.

It has recently been announced that Eutelsat (ETL) will consolidate a majority holding, in the UK company OneWeb, by buying out the UK Government’s £600 million stake in the company. India’s Bharti Global and China’s Sovereign Wealth Fund will get diluted in the process. These two marginalized ethnic, soon to be, minority shareholders once proudly demonstrated the nexus of the BRICs that was infiltrating the UK, in order, to undermine the NATO alliance. Evidently, regime change at Number 10 causally resonates with the dilution of the influence of India and China in this strategic asset.

(Source: the Author)

The IP transfer also seems to have breached national security protocols at the highest levels in the Western Alliance. France was enraged and forced Britain to transfer majority control into French hands, allegedly, as part of the Brexit settlement. Chancellor Sunak was caught breaching Western national security protocols in addition to breaching ministerial conflicts of interest.

The return of Sunak as PM now brings all this national security, and conflicted interest, kerfuffle back to the fore. Effectively, he is compromised as a leader by his former ministerial behavior. Consequently, Britain will never achieve negotiating parity in anything, that he negotiates, until it drops the Butler Model and closes the VIP Lane to people from countries viewed as national security threats to the Western Alliance. It would be much easier if Britain just dropped the UK PM, and, his government, then, started from scratch.

Hence Macron has flexed his muscles and Sunak has demurred. This isn’t just a matter of Sunak channeling wealth to his friends and family. This channeling is a national security threat to the Western Alliance. Thus compromised, Sunak is now Biden’s and Macron’s puppet and not their Bro’.

· Kishidanomics i.e. Abenomics II is the globally acceptable face of UK Kwasinomics.

(Source: the Author)

Whilst Britain may no longer be able to get away with sailing close to the wind, Japan is encouraged to be economically reckless.

Cash rules, digital money cools ….

The last report discussed the depressionary implications of the collapse in the Japanese monetary base.

The latest policymaking nudge, to mitigate the depressing monetary base circumstances, is coming in the promotion of digital payments with incentives attached. Wide consumer adoption has not, however, led to increased consumption. The next nudge is expected to be the paying of salaries and other forms of compensation in digital form. It would be ironic if the digital money supply also collapsed, but there is no fundamental reason why it should not. Pushing on a digital string may not necessarily increase aggregate demand.

Japanese consumers don’t like inflation. Their response has been to Neo-Classically create weak aggregate demand conditions that defeat inflation. This is a rational response to inflation. It is also a response that is an economic headwind.

The globally accepted central bank logic, of tightening monetary policy, to fight inflation, ignores the rational behavioral response of the consumer. Consequently, central banks have been doubling up, the inflation economic headwind with additional monetary policy tightening. OPEC has similarly turned into a global central bank by tightening monetary policy further with higher oil prices in the net oil-consuming nations. The global headwinds are immense.

The rational Japanese consumer response, to this increased headwind, has been to reduce consumption further, thereby, exacerbating the economic headwind. Fooling around with digital payments is, thus, futile. In fact, fooling around with digital payments just weakens the banking system and any potential economic stimulus from this sector. Anecdotal evidence of the folly was to be found in the latest report from Japanese e-commerce giant Rakuten. Consumption with traditional, or alternative, cash is down, as prices rise. Rakuten’s bonds have taken a big hit to reflect the threat to company solvency.

Japan is the Neo-classical example of what central banks should not do when faced with Stagflation. They should not tighten monetary policy aggressively when the Stag part of the word is already running its course. This is why central banks should have tightened, during the early 2021 post-COVID re-opening, when economies were strong. Central banks, however, waited until inflation became a headwind before tightening aggressively. This inertial behavior is a policy error that has created a financial stability problem.

Stagflation can now be seen as pushing up yields on two counts. The Stag part leads to insolvency, hence, a rising credit risk premium. The flation requires an inflation yield premium. Then just to make it all worse throw in a central bank hike, in benchmark interest rates, to fight inflation, and the whole thing becomes a financial stability problem because the whole economy becomes insolvent.

· Japan’s insolvency and contracting monetary base militate strongly in favor of the Yen Carry Trade solution to domestic and global growth risks.

(Source: the Author)

As the global economy reflates around the core of a strong US Dollar, the Crypto-economy deflates.

US Dollar Rules, Crypto cools ….

· The Crypto Crash will soon be framed as the next disinflationary headwind requiring remedial economic stimulus action.

(Source: the Author)

This author has long suggested that the “Crypto Crash” would be framed as a disinflationary headwind and an element in the catalyst of the next global economic stimulus. The recent White House take on the situation, as a catalyst for Federal intervention would seem to satisfy the prediction.

A crash in cryptocurrencies is, by default, one of those footprints that central bankers and policymakers will tell you is only to be found in the Rumsfeld Quadrant. Hence, with both arms of policy flailing around, looking for culprits to blame, and excuses for economic stimulus, growing awareness of the problem is being propagated.

It has taken longer than this author thought for Mr. Market to connect the dots from the global shortage of US Dollars to the surplus of unwanted cryptocurrencies.

The dots would now seem to have been joined up.

The joining of the dots is a growing global consumer headwind.

There’s a crack in my dyke, Dear Christine, Dear Christine ….

· If the ECB and the EU intend to trigger deeper banking sector and economic integration, with QT, Grexit proves otherwise.

(Source: the Author)

In a previous report, this author reminded Eurozone policymakers that their best efforts to promote a deeper banking sector and fiscal economic union would be frustrated. This frustration would come from national governments’ self-interest, in monetizing fiscal deficits, on their national central bank balance sheets, taking precedence over joint monetization at the EU level.

EU officials recently watered down tighter bank capital adequacy rules. The excuse offered, on this occasion, was that this dilution was needed to promote credit creation at the national economic level.

Newsflash! Currently, there is no private credit creation at the national level, however. National economies are contracting. This can only mean, then, that the rules were watered down to allow nations to stuff their counter-cyclical fiscal deficits onto their national central banks’ balance sheets.

On the other hand, the same EU officials also propose a longer negotiated path toward fiscal deficit reduction.

Hence one can see that national central bank balance sheets have been put on notice, to receive larger national fiscal deficits, whilst these said deficits have been extended in size and duration.

The ECB’s, alleged, soon to be, shrinking centralized balance sheet is, hence, in conflict with the expanding balance sheets of the national central banks which comprise it.

· The tactics adopted in trying to remain solvent, whilst following its inflation mandate, mean that the ECB is triggering a banking crisis that will lead to a recession and then more QE.

(Source: the Author)

The ECB has opined that the watering-down, of capital adequacy, risks “cracking the dyke” of financial stability. What the central bank is implying is that when the, expanding, national central banks’ balance sheets meet the, contracting, ECB consolidated balance sheet, there will be a financial stability crisis.

ECB Banking Supervisors Andrea Enria and Joachim Wuermelling have warned that rising interest rates are not a blessing for all banking sector members. The blessing and/or pain will depend on the specific bank’s business model and who its customers are. On aggregate, the two supervisors expect bank capital to be eroded, by rising interest rates, as provisions increase for bad loans.

Maybe, the ECB hopes to force through deeper banking consolidation, with an I told you so moment in the said ensuing financial stability crisis. Hiking interest rates, and shrinking its balance sheet, should, in theory, allow the ECB to trigger this crisis.

There is, however, a more sinister Teutonic threat, to the Eurozone, hiding, in plain sight, like a Trojan Horse within the EU and the ECB.

This Trojan Horse, also, seems to be located in Germany’s Rumsfeld Quadrant.

“Bar-Bar-Bar, Bar-Bar-Barossa”: History is rhyming again ….

Germans seem to think that the term structure, of their interest rates, is being dragged higher by their fiscally inept Eurozone partners.

No doubt, high German inflation, amongst the highest in the Eurozone, will be blamed, by some Germans, to some degree, on these same Southern European fiscal wastrels too. If they were not allowed to borrow so much, these wasters would not be able to push the prices of German imports, so the German logic goes. Hence, if the ECB didn’t allow these wasters, to borrow so much, Eurozone inflation would be a lot better. And so on, and so forth, goes the Sturm und Drang.

Pretty soon, we will be converging on Untermenschen sentiments and corresponding economic epithets. Scapegoating and procrastination are, traditionally, what Germans do when the going gets tough and inflation gets rough.

The specter of Far Right Italians retiring even earlier has no doubt, energized the German soul-searching.

Pretty soon, Germany will be converging back on Untermenschen sentiments and corresponding economic epithets. Scapegoating and procrastination are, traditionally, what Germans do when the going gets tough and inflation gets rough.

German commitment to the European Project is noticeably waning. To be honest, it was never that strong. The Eurozone was sold to Germans as an opportunity to make their neighbors more German, something that Germany had repeatedly failed to do through violence. Since Germany appears to be becoming more European, more foreign, and less German, etc., etc. the commitment to the Eurozone, at the grassroots level is waning.

Russia, and its accessible resource base, were once a convenient buffer to the reappearance of these ugly German faces.

After the Ukraine war started, German resource-starved grimaces have started to get uglier. This ugliness has spread to the faces of German politicians and central bankers. This ugliness is now being directed toward the EU and the Eurozone Project.

The German contingent, within the EU, is dragging its feet on approving the dilution of fiscal austerity. Simultaneously, the Bundesbank is trying to force Eurozone sovereign bond yields higher. Ostensibly, the Germans are trying to enforce fiscal discipline through market pricing discipline.

Un-ostensibly, the Germans are trying to force insolvency onto Eurozone nations and the ECB. This will call for a consolidation of Eurozone assets and a recapitalization of the ECB. In this down-round of sovereign and central bank recapitalization, the Germans seem to think that they will be the consolidators. Germany presumes that its economic strength will guarantee a stronger political and economic position in the consolidated Eurozone financial and political capital structures post-recapitalization. This author is not so sure.

The fundamental weakness of the German economy has been exposed by the Ukraine war. Southern and Eastern Europe have the edge in energy terms since they have less energy-intensive economies that are located within easy reach of potential energy imports.

The energy equation has (conveniently) been omitted from Germany’s strategic calculations and bold political European gambit. This is a strategic mistake on par with the 1941 invasion of Russia. The invasion ended with the resource-hungry invaders freezing to death at the gates of Moscow and Stalingrad. Today, they are freezing in their homes in the German hinterland. The weakening of German power historically ensues such cold snaps. Unfortunately, there is, traditionally, a bit of scrap that goes global first.

Ominously, confirming its strategic weakness, German policymakers are actively considering a national materials-sourcing fund. It all sounds very IG Farben. It doesn’t sound very European, in the collective sense of the European Project. It actually sounds like an act of war, when combined with the Teutonic plans for EU and ECB consolidation. Taking down its neighbors’ economies and then consolidating them is Economic Blitzkrieg.

Evidently, Germany intends to go it alone, again, going forward. The EU and world leaders should be worried. Perhaps, more worried than they are about Russia and China.