“Liberate” the Global Managed Trade/FX Regime

“Soon — they will all stand at the feet of the master and will wag their tails a little.” (Vladimir Vladimirovich Putin)

Summary:

· President Trump is consolidating his “Liberation Day” bridgehead by swiftly advancing to contact with trade partners to negotiate a global managed trade/FX regime.

· President Zelenskiy confirms that foreign wars are now a profit center for the USA rather than a taxpayer burden.

· According to Isabel Schnabel, rhetorically speaking, President Trump has “liberated” a global managed trade/FX regime.

· Tony Blair wants Sir Keir Joseph of Starmergrad to negotiate a better-managed trade/FX deal with President Trump, than he could get pari passu with the EU.

· Tony Blair has given Sir Keir Joseph of Starmergrad Hobson’s Choice to “liberate” the Special Relationship through a managed trade/FX deal with President Trump.

· Mr. Market demands a higher US asset risk premium for a “managed-lower” U.S. dollar.

· Boston Fed president Collins signals that, despite cognitively blind guidance, the Fed is, actually, ready to react to the disinflationary financial instability created by the “managed-lower” US Dollar rising US asset risk premium.

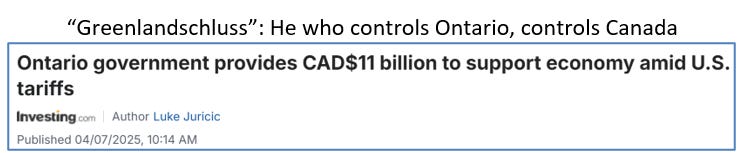

· The recent Ontario bailout of the rest of Canada “liberates” the province to unilaterally negotiate its unilateral trade deal with Trump, which is de facto a national deal.

· A US-Ontario trade deal would be de facto “Ontarioschluss”, hence, “Canadaschluss” by default, in practice.

Extracts

· “Liberation Day” +1 marked the fact that Chairman Powell missed the disinflationary key signal that, in a crisis, Mr. Market still has liquidity preference to hold US Dollar Cash rather than any other asset class or commodity.

· Mr. Market’s liquidity preference is a begrudging global acceptance of the US$ Exorbitant Privilege that signifies continued reserve currency status, and a multilateral vote for “Mar-a-Lago Accord”.

(Source: the Author, April 5th 2025)

· “Mar-a-Lago Consensus” will transfer the global supply chain security cost from the US taxpayer to the global taxpayer/customer.

· “Mar-a-Lago Consensus” will boost the US economy and mitigate the cost of global supply chain security for nations that trade with the USA.

(Source: the Author, December 7th 2024)

· The ECB’s developing “Mar-a-Lago Consensus”, for central banks, “Mar-a-Lago Accord” r* is higher than during the QE interregnum.

· According to the ECB, central banks will remain insolvent and, be out of the QE business until a new round of Global Reserves has been created.

· In a managed trade and managed FX regime, the central banks’ role will encompass currency board operation.

· The Dallas Fed believes that managed trade and managed FX rates, in an era of expanded Global Reserves, will be best facilitated through the creation of short-duration Central Bank reserve liabilities and consummate duration sovereign debt balance sheet assets.

· Based on the recent inventory “check”, by POTUS, at the Kentucky Federal Bank of Barbarous Relic, the next sovereign creation of Global Reserves will be in proportion to the level of national Gold Reserves.

(Source: the Author, March 1st 2025)

· To save itself, and the Special Relationship, the Global Blair Inc. Witch Project has folded its “hands” in with the “Mar-a-Lago Consensus” imperative.

· “Starmergeddon” is the most likely critical pathway of the Global Blair Inc. Witch Project's next step.

(Source: the Author, January 18th 2025)

· The unipolar “Mar-a-Lago Consensus” reinforces the global energy security imperative, and aligns, with US Swing Producer status, to deliver a disinflationary global economic stimulus, exclusively, to America’s trade partners.

· “Mar-a-Lago Consensus” and US Swing Producer status combine to reinforce the unipolar “US Exorbitant Privilege”.

(Source: the Author, December 7th 2024)

· OPEC+ must cut energy prices, at least as much as the “Mar-a-Lago Consensus” threatened tariffs, on sanctioned non-US purchasers, to maintain market share.

(Source: the Author, December 21st, 2024)

· The halo effect, of the recent US Minsky Moment, highlights that the Fed is now two FOMC meetings out of re-alignment with the “Onshore Mar-a-Lago Accord” policy curve.

· The Fed’s misalignment raises the requirement for a less gradual re-alignment than Chair Powell’s “Transitory” rhetoric signals.

· President Trump has “Executively Nudged” the Fed off its employment mandate dataset onto his DOGE “Onshore” dataset.

(Source: the Author, March 22nd 2025)

· Ontario has applied to become the 51st State of the USA, ahead of “Made-in-China” Mexico.

· Where Ontario capitulates today, the rest of Canada, which it financially supports, will follow tomorrow.

(Source: the Author, April 5th, 2025)