The Global Economy Approaches Friend-Shoring Junction

“To Macklem, or not to Macklem? That is the real question.” (Unattributed)

Summary:

· The FOMC’s barnstorming domestic economic landing has reached global “Friend-Shoring Junction”.

· Macklem Doctrine ticks all the “friend-shoring” boxes.

· US “friend-shoring” will be achieved with “Build Back Better” and “Make More In America” fiscal drivers.

· Unrealized balance sheet losses may have just triggered the Macklem Doctrine embracing “Fed Put”, in the form of the “Waller Put”.

· The “Waller Put” signals that the FOMC will not kill the “Build Back Better” and “Make More In America” booms.

· The recent Wall Street earnings season-wink signals that the US financial sector has, already, become the medium of economic transfer of the FOMC’s “methodical” and “expeditious” tightening which has only just begun.

· The Dallas Fed kicks off the “FOMC Two Step”.

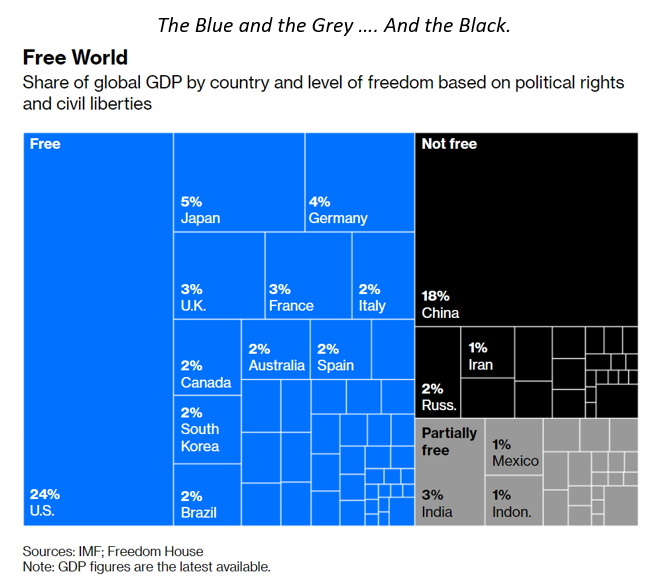

Multilateral New World Order Rules: A Friend of My Friend is My Friend …. etc.

The New World Order, as envisioned by G7, has some important calendar events coming up at the Spring Meetings of the World Bank and the IMF.

· The war in Ukraine is the catalyst for irreversible structural changes in the global economy.

(Source: the Author)

President Biden, seemingly, intends to go into the meetings from a position of onshoring. On the eve of the meetings, he promoted his own domestic manufacturing bill.

The President’s onshoring call to arms was answered, initially, by the EXIM Bank of the United States. The bank’s board unanimously voted to approve the Make More In America Initiative. Going forward, more will be made in America through the provision of favorable domestic financing conditions by the bank. Most of the President’s Build Back Better stimulus may, therefore, get spent and built at home.

This onshoring stance is, presumably, based, to some extent, on Biden’s weak position in the opinion polls ahead of imminent midterm elections. Onshoring, however, is impossible to achieve exclusively in America, since some foreign imports of goods and commodities will be required. In practice, therefore, onshoring will require some dilution and diversion, to recognize the fact that America requires global partners to be successful in the future.

· “Supply-Side Keynesian” Yellen wishes to Build Back Better America’s disinflationary supply chain with a larger fiscal deficit.

(Source: the Author)

Treasury Secretary Janet Yellen, recently, remarked on the USA’s intentions and capabilities going into the Spring meetings. Yellen is unashamedly multilateral in her approach, not necessarily by choice but by the practical necessity of the need for global partnerships to be successful. On the critical issue, of supply chains, America will be “friend-shoring”, according to Secretary Yellen.

In Yellen’s worldview, true friends do not create American inflation by constraining the supplies of goods, and commodities, that America imports. Clearly, Russia, therefore, is no friend. All of America’s trade partners should, carefully, look at themselves in this frame of reference, going forward, to see if they qualify as friends or foes.

“Friend-shoring” does not, currently, exclude China. China may however exclude itself, by its continued support of Russia; and its deliberate policy of cornering the commodity markets for elements used in the technological development of the global economy.

Yellen’s climacteric speech, suggests that the global economy is at a fork in the road. “Friends” will go down one branch and Unfriends/Foes, the other. The future will be defined not only by what each branch does but, also, by how each branch interacts with the other.

The multilateral rules of the game, for friendly players, are being written and disseminated in real-time.

Readers should understand that the future outcome is binary. If one does not sign up for “friend-shoring”, one will be assumed to be an unfriend/foe (perhaps even a hostile!) until one does. The door to becoming a friend remains open, and the economic pain of not going through it will be ratcheted up, with sanctions and trade barriers, over time.

Readers, who are theme/factor investors, should have their portfolios exposed to the “friend-shorers”. Cautious investors may wish to hedge, with some exposure to the unshored/foes, however, this author suggests that they may have to emigrate (permanently!) to enjoy the returns on their hedges.

· Macklem Doctrine (GHOS Protocol) will roll out in global venues soon and run for three years if successful.

(Source: the Author)

To understand all the rules, of the board game, this author has named it Macklem Doctrine. This doctrine, named for its author, Bank of Canada Governor Tiff Macklem, involves supply-side investment, in order, to unblock global supply chains; and make them more resilient to economic shocks. So “friend-shored” beneficiaries, of this supply-side investment, should be where the Alpha gets generated.

Macklem Doctrine, ticks all of Janet Yellen’s “friend-shoring” boxes. This doctrine appears to have been ticked by the World Bank and the IMF also.

Macklem Doctrine “is probably good news for everyone” …

The World Bank has become one of the latest global financial institutions to embrace Macklem Doctrine. The leader of the organization recently opined, on the issues of global supply chain and infrastructure investment, which are, required to address current constraints and frictions. The World Bank has provided its own take on the classification of “friend-shoring”.

World Bank President David Malpass believes that the onshoring of supply chains, and commensurate infrastructure investment, away from China, “is probably good news for everyone”. Probably is not as strong a word as definitely, however.

Malpass appears to have elected to use the word probably because he is still concerned to engage with China in solving global issues. Let’s see how Malpass’ vocabulary of estimated probability develops in line with global developments.

The IMF is more nuanced than the World Bank, in relation to the Macklem Doctrine thesis. This nuance, involves the requirement for greater diversity, in global supply chains, rather than their concentration within fewer trade partners. The IMF’s nuance, thus, belies a coalition of the willing trade partners inherent in Yellen’s “friend-shoring” thesis. Doubtless, said trade partners will have the same/similar views on political and economic governance.

To expand the coalition of “friend-shorers”, into direct contact/conflict with China’s Belt and Road alternative friend-shoring initiative, the IMF is also proposing a special funding program aimed at less-developed nations.

The issue of food security is garnering the prominence that will place it under the “friend-shoring”, and hence Macklem Doctrine, umbrellas. No doubt, President Putin will, also, be blamed for the latest increase in global food insecurity, and the attendant inflation. The World Bank (WB), IMF, World Food Programme (WFP), World Trade Organization (WTO), and International Fund for Agricultural Development (IFAD) are collectively “friend-shoring” an action plan, to address the food security issue at the global NGO level.

With the global rules of the game coming along nicely, the fiscal and monetary policy settings of the G7 protagonists require preparation. Some are in better shape than others for “friend-shoring”.

The US Fiscal Deficit: To Infinity and Beyond ….

Mind the (Missile) Gap: Crossing the Rubicon, by way of the Atlantic and Pacific Oceans ….

The Anglo-Saxon-ANZAC cadre, within G7, give it a name, AUKUS, is starting at the global level and sailing upstream from there.

(Source: the Author)

The last report discussed the mounting pressure on the US Federal deficit from the perceived “Missile Gap” with China and Russia.

The Defence Intelligence Agency (DIA) has recently added some footnotes, and zeros, to the growing fiscal bill; in a recently published report extending the “missile gap” into outer space. An arms race, in space, will, thus, mirror the terrestrial race and presumably bankrupt some, in not all, of the runners. Clearly, the Soviet Union couldn’t keep the pace in the last race.

Now, it remains to be seen if China, and what is left of the Soviet Union, have the legs and the money to go the distance.

Clearly, also, the Federal Reserve will be required to lessen the handicap for the beleaguered US taxpayer, by making its balance sheet a runner.

The State Department has, subsequently, created the terrestrial mirror, of the heavenly conflict, and potential warzones, with its annual update of the dirty list of human rights abusers. Russia is top of the list, with China a close second.

More interestingly, from this author’s perspective, Nicaragua is in the top five on the State Department’s black list. The Sinophile drift of Nicaragua was noted at the beginning of the year.

The American thirty-year narrative involves the funding and creation of a bipartisan consensus from the perceived Chinese threat via Latin America.

(Source: the Author)

This drift, potentially, towards a Bay of Pigs Moment has now become a more elevated probability. Countries in the region are drifting towards this point under their own steam in any case. In their attempts to make inflation look lower, than it is, sales taxes are being cut and price subsidies are being applied. Consequently, fiscal deficits are ballooning and the economic strength of the governments is waning. Simply speaking, their fiscal position, is nudging them off the US Dollar reserve standard. Normally, the IMF would step in and chain them to the US Dollar standard. Now, however, China and Crypto appear to be an alternative solution.

The Latin-American drift, towards China, has also been characterized by the region’s drift, off the US Dollar global reserve standard, towards the Bitcoin Standard.

What Do Fed Monetary Policy, Common Prosperity, A Bipartisan Republic, Some Banana Republics, And A Bitcoin Republic All Have In Common?

Dec. 12, 2021 2:12 PM ETBTC-USD, BTCE-USD, TLT

(Source: the Author)

Evidently, since Bitcoin is being framed in the same picture as poor political and economic governance, casus belli for intervention, of some kind, is building.

The limits of US monetary policy have been neatly circumscribed by the US global imperative.

(Source: the Author)

As discussed, in a previous article, the Fed’s scope for monetary policy normalization has been circumscribed by the US global imperative. Unfortunately, the Fed’s eagerness to embrace the Federal Government’s COVID response has created inflationary consequences which are undermining the embrace of the new global imperative. This unfortunate situation has been noted by a former ECB Chief Economist.

Issing the Point ….

· The war in Ukraine is the catalyst for irreversible structural changes in the global economy.

(Source: the Author)

This author’s thesis, that the global economy has been structurally shifted, onto a higher inflationary plane, by recent global events, appears to resonate with the worldview of the ECB’s former Chief Economist Otmar Issing.

Professor Issing believes that 30 years of globalization is now swiftly unraveling, churning its original disinflationary paradigm in its destructive wake. His views, clearly, resonate with the editorial line in the globalist media organs since the end of 2021.

According to Professor Issing: “the ECB relied on its forecasting model and this model cannot give the right signals because it is based on the past and cyclical experience — and the pandemic did not cause a cyclical downturn,” and “you need a much broader approach to explaining inflation in a time of structural changes. If you have a misdiagnosis, of course, you have a misguided policy.” Issing’s analysis has one size that fits all global central banks.

Professor Issing was unavailable for comment on what is currently being rolled out in the G7 economies as the supply-side solution. His viewpoint is strictly related to domestic monetary policy settings in the Eurozone and the United States. The global solution has been called Macklem Doctrine, by this author. The doctrine involves supply-side investment, and restructuring, to onshore the 30 years of globalization, which are now unraveling; back home to countries with an alleged better track record on economic management and governance best practices. China and Russia have cast themselves as the enemies, of this global solution, by the pursuit of their own alternative global economic order.

· Whilst united, on Ukraine, at the global level, G7 nations and their central bankers are diverse at the national level.

(Source: the Author)

Following Issing’s observation, the various G7 central banks can now be seen trying to align their domestic monetary policy settings with the global dialectic. This alignment is an idiosyncratic process, dependent upon the economic and political situations on the ground. Consequently, various forms of economic landing from the removal of COVID-19 monetary and fiscal stimulus are up in the air simultaneously.

Each landing is fraught with its own idiosyncratic difficulties.

A barnstorming landing ….

· The US will have a barnstorming attempt at a soft economic landing.

(Source: the Author)

The last report suggested that the FOMC’s attempted soft-landing would appear more like barnstorming.

The US economy has an inflation tailwind that is shifting to become a headwind. There is also a global growth headwind gaining momentum. In addition, the US economy has a recently emerging fiscal tailwind, that will boost inflation, through the combined forces of the military, build back better and make in America drivers. Predicting the resultant combination of all these forces will be more artful than scientific.

Incoming FOMC guidance speaks to a desire to address the pure consumer demand-driven inflation component, whilst preserving the capital investment-driven inflation of the new fiscal economic drivers. Recession is, therefore, a low probability even if it may feel like it for those exposed to the consumer sector. Disinflation is also a low probability. What kind of inflation is acceptable is, as yet, unknown.

FOMC members are, presently, framing perceptions of the resultant combination of economic forces that will portend an acceptable level of inflation.

Do no harm ….

As she Faced the Nation, Cleveland Fed president Loretta Mester adopted a do no harm style of outcomes-based forward guidance. Mester started with the least painful economic outcome and then worked back to a monetary policy stance that is consistent with it. Monetary policy tightening will, henceforth, only be targeted at the excess demand in the US economy. Presumably, worried that this focussed message had initially been missed, in the mass hysteria of rising bond yields, Mester then repeated herself with emphasis on the benign economic outcome. She may have to keep repeating herself since the hysteria is garnering more attention than her guidance.

Based on her guidance, Mester expects a monetary policy tightening phase that leaves inflation above target in 2023. The war in Ukraine is also net inflationary, in her view. The monetary policy tightening achieves nothing, in terms of fighting inflation, however, it doesn’t create a recession either. It’s political, it’s populist and it’s the best that she can extemporize under the circumstances. It buys time until 2023 if nothing else.

Chicago Fed president Charles Evans is taking the do no harm meme a little too literally. He wants to arrive at his neutral rate, circa 2.25% to 2.5% Fed Funds, by year-end. Despite this leisurely pursuit, of the neutral rate, he is, however, willing to discuss a 50-basis point rate hike as long as someone else on the FOMC suggests it.

Missing the barn, but accidentally killing the herd ….

Fed Governor Christopher Waller has been brutally honest about his economic landing approach. Whilst he seeks to do no harm, in principle, he warns that there will be unavoidable “collateral damage”, because interest rates are an indiscriminate monetary policy tool lacking in finesse.

Deliberately killing the herd, whilst pretending to aim at the barn ….

· James Bullard no longer has credibility.

(Source: the Author)

St. Louis Fed president James Bullard is a man with a hammer. Consequently, he only sees inflation nails. So keen has he become, to hit these nails, with interest rate hikes, that he completely misrepresents what the inflation problem is about.

According to Bullard, he is going to hit those elements of demand that are driving inflation. So, Bullard is attacking the demand-side of the economy. Unfortunately, his attack will also hit the supply-side of the economy, thereby, constraining supply chains and what they supply. In practice, therefore, he will also be hitting those supply-side enablers of disinflation that should be avoided.

Bullard’s indiscriminate carpet-bombing of the US economy will, thus, beget economic contraction. Little does he care about the structural components of inflation, within the supply chain, that he is shutting down.

Inflation erodes credibility ….

· Thomas Barkin gets a credibility downgrade.

(Source: the Author)

This author has noted the demise of essayist, and Richmond Fed president, Thomas Barkin’s credibility. Barkin has been on the fence for some time, observing the causes and effects of inflation, inconclusively. He has adopted the conflicted default position, of wishing to get to the neutral rate, as swiftly as possible, but, remaining loath to get there via 50-basis points interest rate hikes.

The recent spike in the US CPI has brought Barkin’s conflicted predicament into greater relief. His latest guidance finds him, still, inconclusively, sitting on the fence advising data dependence in relation to the size and pace of rate hikes. Unfortunately, for him, the latest inflation data should have pulled him off the fence onto the 50-basis points side, but he will not admit it. Rather, it seems, like Evans, he prefers someone else to suggest it so that he can go along with it, whilst opining the need for caution. If inflation has recently peaked, he can then say I told you so.

Learn your meme “methodically” and “expeditiously” ….

Fed Governor, and nominee Vice-Chair, Lael Brainard has added some new words to her monetary policy role play. Ostensibly, monetary policy will be tightened “methodically” and “expeditiously” going forward. Exuding such confident signals may evince a safe pair of hands that expedites her nomination at a more than methodical pace.

New York Fed president John Williams is, also, “expeditiously”, singing from the same page as Brainard. His libretto, “expeditiously”, involves an allegro movement of 50-basis points rate hikes played with brio.

Philadelphia Fed president Patrick T. Harker is also on the methodical page, but, not necessarily, the 50-basis point expeditious page though. His libretto proclaims the need for "a series of deliberate, methodical hikes" because inflation is "far too high".

Do not self-harm: The “Waller Put” ….

Liminal signals of what has been called the Fed Put were evident in the latest guidance from Fed Governor Christopher Waller. The “Waller Put” does not envision swiftly tightening, to fight inflation, beyond a level that destroys the capital markets and the US economy.

Thus far, in the tightening cycle, this is the first mention, by one of its voting members, that the FOMC is actually concerned about market reactions. One senses that the FOMC is more concerned about the level of bond yields than equity valuations.

The “Waller Put”, thus, has a note of financial stability policy, about it, that will resonate later with a similar tune from the Dallas Fed.

· The Fed may embrace Macklem Doctrine when it sees the unrealized losses on its balance sheet from the recent spike in yields.

(Source: the Author)

This author has suggested, previously, that the FOMC will suddenly start paying attention to growth risk when the spike in bond yields has created substantial unrealized losses on its balance sheet. That time is now.

A Fed in need of recapitalization, from the US Taxpayer, when it was supposed to be mitigating the taxpayers’ pain with lower interest rates, is the kind of anathema that finally destroys the Fed’s credible commitment. As a bi-product, of this loss of credible commitment, the Fed will find it difficult to monetize the fiscal deficit that Janet Yellen envisions with her “friend-shoring” thesis. Clearly, talking up growth risks, hence the Fed Put, mitigates the credibility disaster and supports the principles of Macklem Doctrine.

The FOMC has just blinked, through the eyes of Christopher Waller.

If Waller has blinked, with one eye on the Fed’s balance sheet, his other blinking eye may be in response to Wall Street’s latest wink.

Dirty Dancing: Nobody puts (My) Bonus in the corner ….

The ugly earnings coming in from the US bulge-bracket banks, especially JP Morgan and Goldman, point to a sudden deceleration in capital markets activity. Generally speaking, such a deceleration portends an economic slowdown. Wall Street has, thus, asked the Fed to prepare its Put, and Waller has reciprocated. The reciprocation is not, however, the traditional Put in the form of a promise to ease. It is a pledge not to tighten too much, on this occasion. Credible commitment, on this occasion, requires the FOMC to fight inflation to the exclusion of Wall Street’s desired Put writing.

Wall Street must, henceforth, get its balance sheet, and capital buffers, in order to receive negative credit events. Wall Street has, in fact, already, done so.

By preparing for incoming bad news by tightening credit standards, and raising capital buffers, Wall Street has already become the vehicle of economic transfer of the FOMC’s “methodical” and “expeditious” tightening that has only just begun. Chances are, therefore, that the Build Back Better and Make More In America programs will be big drivers of Wall Street earnings, going forward. The FOMC has promised not to kill these two drivers with a recession.

As Wall Street gets its balance sheet in order, in risk-off mode, the transmission of FOMC tightening is showing up in a corner of the real economy that is of great concern to the Fed.

Trendline Dancing: Nobody puts Financial Stability in the corner ….

Previously, this author had noted the FOMC’s line-dancing style of tightening with words, via the forward curve, thereby stepping back in practice when it is time to deliver on the words. This music and dancing continue in Texas.

This music and dancing also follow a financial stability policy tune that seems to resonate with the “Waller Put” tune.

A recent, timely, study by the Dallas Fed has concluded that the tightening of liquidity conditions, in commodity markets, combined with the geopolitical tensions, are creating increased financial stability risk. Wall Street, it should be remembered, has, just, confirmed the financial stability piece.

The Dallas Fed researchers advise that the FOMC should be focused on this growing financial stability risk. The risk, and hence the commodity inflation derived from it, is a real economic headwind. This risk is squarely blamed on Russia as the initiator. There are, also, however, willing collaborators, in the commodity supply chain, who now face sanctions and intervention unless they comply.

The analytical suggestion is that commodity traders should, voluntarily, scale back their risk-taking, and strengthen their own balance sheets, in a kind of “friend-shoring” display of compliance. If the commodity traders do not comply, there is an imputed threat of direct intervention in the research article. The message is clear. It is time for commodity markets to calm down and stop playing havoc with price inflation, by hook or by crook.

· Disinflation price discovery by Cancel Culture is on the global commodity and capital markets agenda.

(Source: the Author)

What the Dallas Fed researchers fail to mention is just how much of the financial instability the FOMC itself is creating first by letting inflation overheat, and second by overreacting.

This author has noted, before, that the cancel culture strategy of regulators, in commodity markets, is in effect a deliberate attempt to control prices. The Dallas Fed is warning commodity traders to comply or their trades, and their businesses will be canceled. The cancellation could come through recession, or it could come through market intervention. Either way, the outcome is asymmetrically the same.

Notwithstanding the real root cause of financial instability, the Dallas Fed is framing the situation as an economic headwind. Wall Street has gilded the frame of reference with its poor earnings and credit tightening. This frame advises the FOMC to do no harm, and Mr. Market to expect that no further harm will be done if he complies with his commodity trading.

Economic soft landings are difficult to achieve. It always helps to move the runway though.