Full Employment: Frame …. Define, Discuss

“That’s quite a strong jobs report.” (Thomas Barkin)

Summary:

· The 1990s playbook is rhyming, audibly, but not repeating exactly.

· Ill-advised OPEC+ restraint supports US Swing Producer status and US Dollar global reserve medium of “unsanctioned” commercial exchange status.

· The US Dollar is the global reserve medium of “unsanctioned” commercial exchange, but it is not the global reserve of economic value.

· The Reserve Bank of Australia’s Modern Monetary Monopsony Theory (MMMT) policy framework will be “ample”.

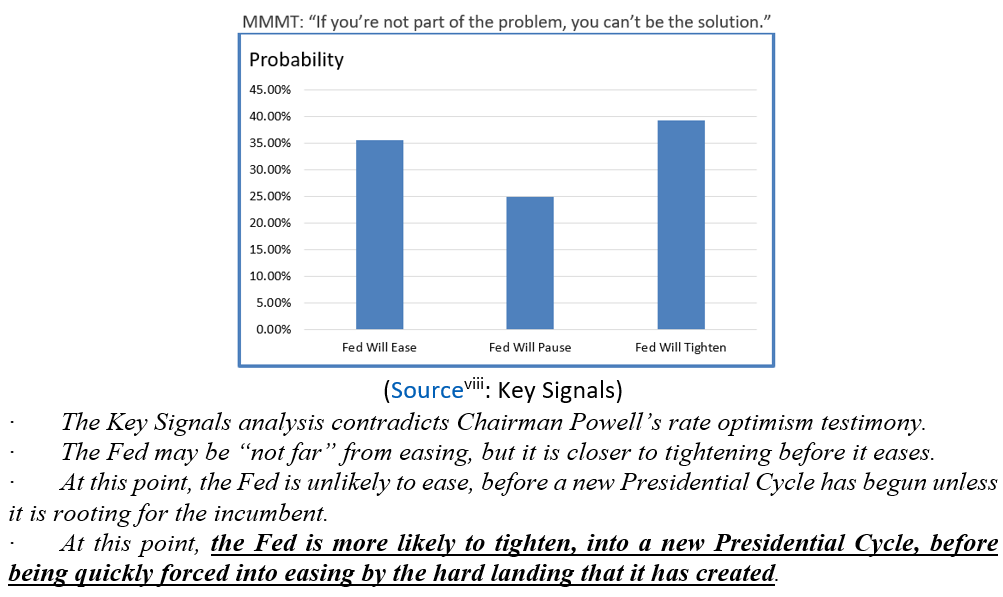

· The FOMC is forward guiding itself onto the Key Signals forward curve.

· The immediate challenge, for the FOMC, is to frame the latest employment sitrep in the context of the new definition of full employment imperative.

Extracts

· Chairman Powell informs Mr. Market that he has not price-discovered “Macklem Doctrine” by the desired process of a strong US Dollar, lower oil prices, and lower bond yields, as anticipated from the recent FOMC signaling.

· The broken FOMC signaling implies a loss of credible commitment and, thereby, greater risk to the desired Soft-Landing outcome.

· Extended OPEC/Russian production cuts have had the unintended effect of strengthening the US Exorbitant Privilege, and US economic relative outperformance/attractiveness which are discounted into the “Stronger for Longer” US Dollar.

· American “Swing Producer Status” is, effectively, “Texas Swing Producer Status”.

(Source: the Author)