Do You Want Some Weimar Beanz, With Your Gresham’s Shrinkflation?

“When depreciated, mutilated, or debased coinage is in concurrent circulation with money of high value, in terms of precious metals, the good money automatically disappears.” (Thomas Gresham)

Summary:

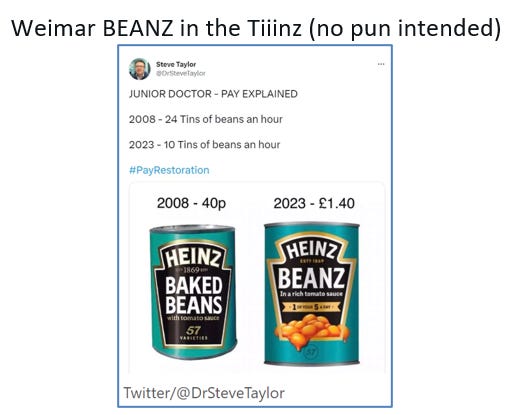

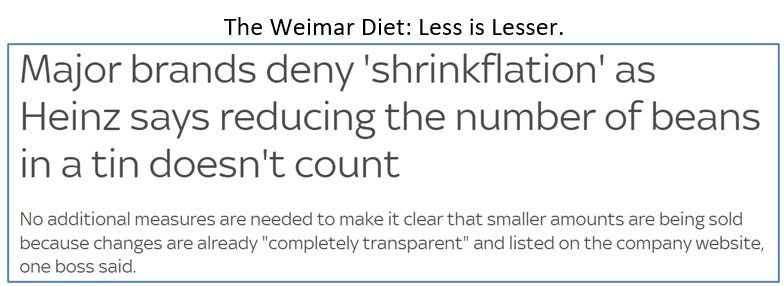

· The real evidence of Shrinkflation disabuses the developed central bank meme that inflation is falling.

· Shrinkflation confirms that “one gets much less, for a bit less”.

· Shrinkflation strongly vitiates the credible commitment of central banks currently adopting Modern Monetary Monopsony Theory (MMMT) policy frameworks.

· Shrinkflation means that central banks will get fewer assets, on their balance sheets, for less Modern Monetary Monopsony Theory (MMMT) Quantitative and Qualitative Easing stimulus.

· Since Shrinkflation diminishes marginal returns on monetary policy stimulus, the appearance of economic weakness will oblige central banks to exponentially expand the quantitative monetary policy stimulus in volume, and, over time.

· The exponentially expanding monetary policy stimulus is an exponentially expanding financial stability threat, which may become a hyperinflationary price threat if financial assets are abandoned in favor of consumption.

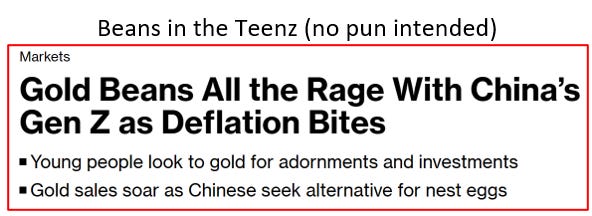

· Physical Gold, and Bitcoin are experiencing Shrinkflation.

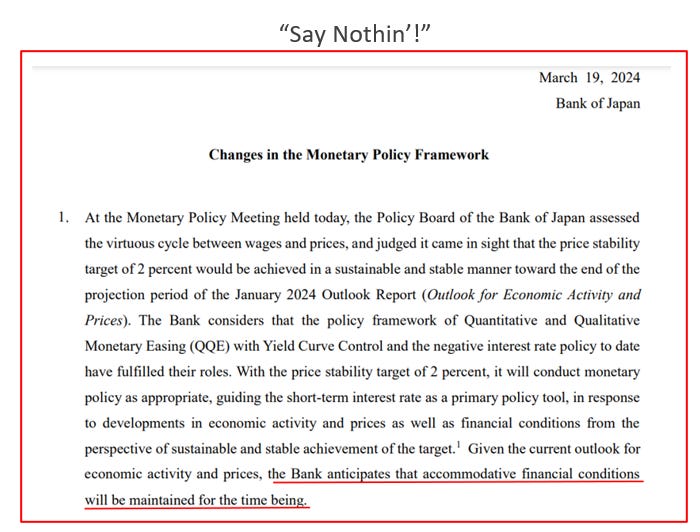

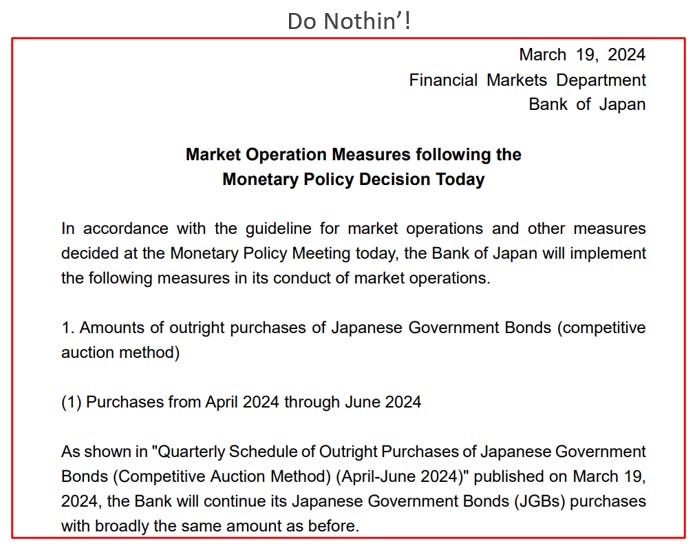

· The BOJ confirmed that its new Modern Monetary Monopsony Theory (MMMT) framework has exclusive monopsonist Quantitative Easing (QE)settings.

· The BOJ’s monopsonist QE settings “negate” the negative balance sheet impact of the removal of Yield Curve Control (YCC).

· The BOJ’s monopsonist QE settings maintain the basis of the weak Yen/Strong US$ that global central bank currency debasement is predicated upon.

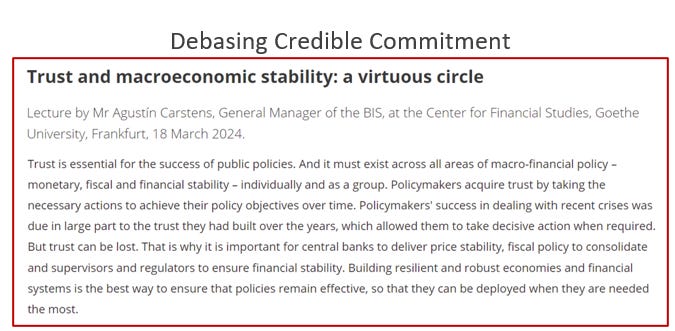

· The BIS diagnoses that intransient inflation makes Modern Monetary Monopsony Theory (MMMT) implementation premature at best, and stillborn at worst.

· Global implementation of Modern Monetary Monopsony Theory (MMMT), alongside intransient inflation, would erode central bank credible commitment with dangerous implications for financial stability.

· Chairman Powell didn’t get the BIS inflation risk memo on MMMT.

· Raphael Bostic may have got the BIS inflation risk memo on MMMT, but he is still keen to stop Quantitatively Tightening for financial stability risk reasons.

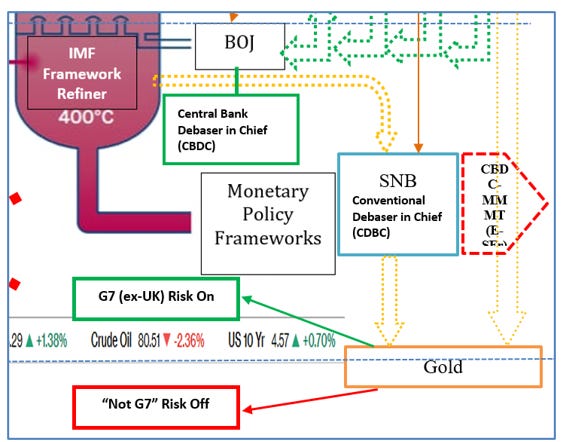

· The “Conventional Debaser In Chief”(CDBC) Swiss National Bank (SNB) acts eponymously rather than surprisingly.

· The SNB confirms its pre-signaled intentions and capabilities, to return to solvency, via a process of asset price inflation rather than real economic price inflation.

· The SNB has, also, blazed a trail for the ECB to follow in its own attempted return to solvency.

· The BOJ and the SNB have confirmed their respective positions of “Central Bank Debaser In Chief” (CBDC), and “Conventional Debaser In Chief” (CDBC); which preserve the US Dollar’s prime reserve currency status in the new global Modern Monetary Monopsony Theory (MMMT) central bank infrastructure.

· The IMF has disclaimed the inflationary combination of Political Dominance, and Fiscal Dominance whilst observing the loss of central bank independence in the premature, current, application of Modern Monetary Monopsony Theory (MMMT).

· Fed Governor Barr disclaims the Financial Sector Dominance of Modern Monetary Monopsony Theory (MMMT) from the capture of macroprudential policymaking by the Federal Reserve Banking Sector lobby.

· The Federal Reserve Banking Sector Dominance is an implied macroprudential policy easing which the Fed should (but won’t!) counter, with tighter monetary policy settings, to reduce the “exponential” financial stability policy risk from, the “exponential” easing response to, the fallacious “GDP Shrink” observed in Shrinkflation.

Extracts

· The BIS confirms that digital currency debasement is next on the agenda of developed central banks.

· In order to promote credible commitment, in digital currency debasement, the Fed is trying to destroy the credibility of digital and physical alternatives.

· The Fed’s digital monetary debasement is everywhere and always a balance sheet phenomenon.

· An expanded central bank balance sheet will be the norm and not the exception.

(Source: the Author)

· Gold (and Crypto) cannot wait for Modern Monetary Monopsony Theory (MMMT) to get the official inflation green light from the BIS and the IMF.

· The test of Crypto versus Gold, as the best MMMT alternative store of value, is the essential next step for the basis of new central monetary policy frameworks that involve CBDCs.

· For MMMT central bank monetary policy frameworks, involving CBDCs, to be successful, Gold must defeat Crypto, because the latter is not an official global reserve currency.

(Source: the Author)

· The BOJ upholds globally coordinated MMMT, which is predicated on a managed foreign exchange rate system that maintains the appearance of US Dollar strength.

(Source: the Author)

· The recently (marked-to-market) solvent BOJ demonstrates the precedent for the panacea of Modern Monetary Monopsony Theory (MMMT).

(Source: the Author)

· Governor Kuroda confirms the Key Signals translation of Higher/Tighter for Longer as MMMT Forever.

(Source: the Author)

· The recent ETF marked-to-market solvent BOJ flips its Modern Monetary Monopsony Theory (MMMT) policy framework mix, from Quantitative/Qualitative Easing to Quantitative Easing only; in order to mark its bond portfolio in the black.

· The BOJ has become an “Indirect Inactivist Investor” in Japan Inc.

(Source: the Author)

· He/She/They Gold has the correct global macro view.

· He/She/They Gold envisions a debased currency polycule that is artificially inseminated by Modern Monetary Monopsony Theory (MMMT).

· MMMT is consistent with a new definition of full employment.

· CBDC is fertile ground for monetary artificial insemination.

· The ECB is piloting “Jefferson’s Airplane” with a dose of MMMT artificial insemination.

· The Central Bank of the Ungoverned Kingdom (BOE) confirms that it is in desperate need of MMMT artificial insemination.

· MMMT artificial insemination is a debauched process of digital currency debasement.

· The Fed’s MMMT artificial insemination will be carried out through a process of evolution of the monetary supply chain.

· The Fed’s MMMT artificial insemination process is consistent with “Brimmer’s Law”.

· The Fed’s MMMT artificial insemination will digitally disintermediate the Federal Reserve System Banks and leave them at risk of not being bailed out anymore.

· Disintermediated Federal Reserve System Bank credit will command a higher risk premium and cry out for FOMC interest rate cuts.

· The Fed insists that Congress will have the final de jure say over a digital currency debasement process that is de facto already evolving ultra vires.

(Source: the Author)

Summary:

· The insolvent Swiss National Bank (SNB) intends to return to solvency by a process of financial asset price inflation rather than real economic price inflation.

· The action of the Swiss National Bank (SNB)is a global risk-on signal for developed economies’, ex-Ungoverned Kingdom (UK), asset prices.

· The action of the Swiss National Bank (SNB) confirms the recent behaviour of “He/She/They Gold”.

· The SNB will also embrace the digital currency debasement zeitgeist of the times.

· Rumour has it that the ECB also intends to return to solvency by the same method as the SNB.

(Source: the Author)

· At this point, the Fed is unlikely to ease, before a new Presidential Cycle has begun unless it is rooting for the incumbent.

(Source: the Author)

· The Fed’s new Modern Monetary Monopsony Theory (MMMT) policy framework intends to ease Macro-Prudentially, rather than quantitatively or qualitatively.

· The Fed’s new Modern Monetary Monopsony Theory (MMMT) policy framework transfers wealth, from the Fed balance sheet to bank shareholders, for creating private credit with less regulatory capital risk.

· The Fed is failing to cure any banking sector addiction to MMMT with new capital adequacy and commercial risk pricing rules and regulations.

· The Fed’s new Modern Monetary Monopsony Theory (MMMT) policy framework is a morally hazardous surrender to, and capture by, the banking sector rather than the executive branch of policymaking.

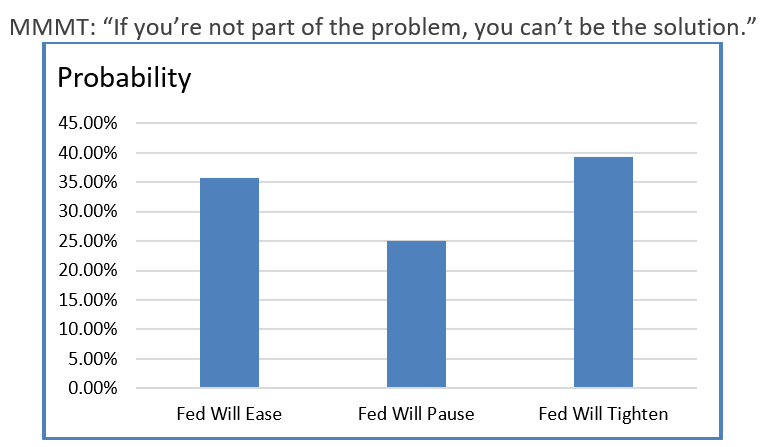

· The Key Signals analysis contradicts Chairman Powell’s rate optimism testimony.

· The Fed may be “not far” from easing, but it is closer to tightening before it eases.

· At this point, the Fed is unlikely to ease, before a new Presidential Cycle has begun unless it is rooting for the incumbent.

· At this point, the Fed is more likely to tighten, into a new Presidential Cycle, before being quickly forced into easing by the hard landing that it has created.

(Source: the Author)