Fractionation Spring Is The New Fragmentation Spring

“Prices are the second casualty of War.” (Inspired by Aeschylus)

Summary:

· The Hyper-Milflation component of Shrinkflation is a national, and economic security threat that may “shrink” America’s global footprint.

· “Patriotic Monetary Policymaking” will oblige the Fed to monetize the Hyper-Milflation fiscal deficit to prevent rising real yields from “shrinking” the real economy.

· President Macron’s ambitious militarization agenda frames the ECB, and its balance sheet, in the same “Patriotic Monetary Policymaking” target as the Fed.

· “Macron’s Failure” to defeat “Joe Le Patsy”, with EU-Russophilia, is a political mistake with Hyper-Milflationary consequences.

· “La Green Dipper” wants ECB “Patriotic Monetary Policymaking” to Hyper-Greenflate the Green Transition.

· The “Neo-Alternative fur Deutschland” requires Hyper-Milflation to drive the Green Transition towards Red Zero Militarism.

· In order to be an economic stimulus, the “Neo-Alternative fur Deutschland” requires parking space on the Bundesbank’s balance sheet.

· “Patriotic Monetary Policymaking” will oblige the “ample” Reserve Bank of Australia (RBA) to monetize the “ample” Hyper-Milflation fiscal deficit to prevent rising real yields from “shrinking” the real economy.

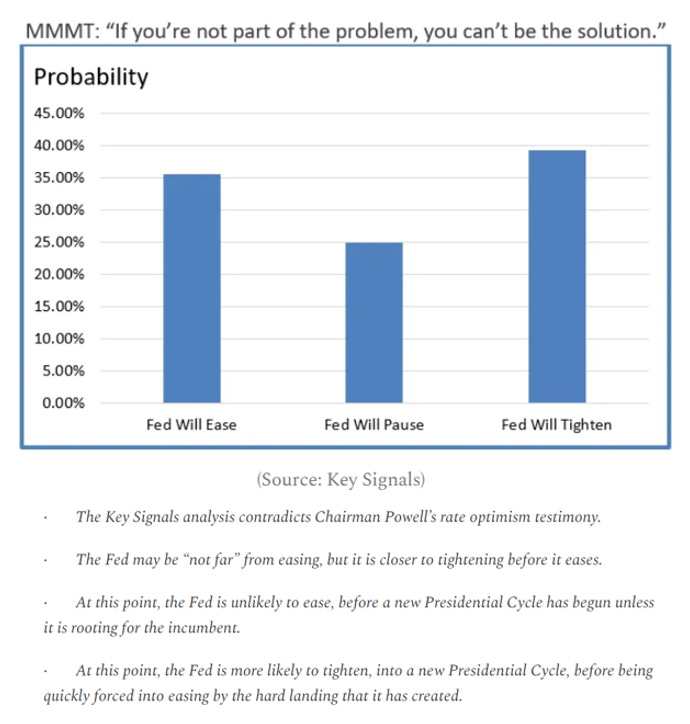

· Chair Powell is on the tail of the Key Signals forward curve.

· Jefferson’s Airplane is approaching the Key Signals forward curve.

· Raphael Bostic is on the tail of the Key Signals forward curve.

· The sincere version of John Williams would now be hiking interest rates, rather than jawboning them.

· The insolvent Netherlands Bank has confirmed that it will follow the insolvent Swiss National Bank (SNB) precedent that prioritizes its own solvency over its inflation mandate.

· The yield-hunting U.S. consumer, and inert inflation, will prompt the macro-prudential easing, by the Fed, to rescue its banking sector capturers.

· Sticky inflation-driven “Fragmentation Spring 2023” has reappeared at IMF Spring 2024.

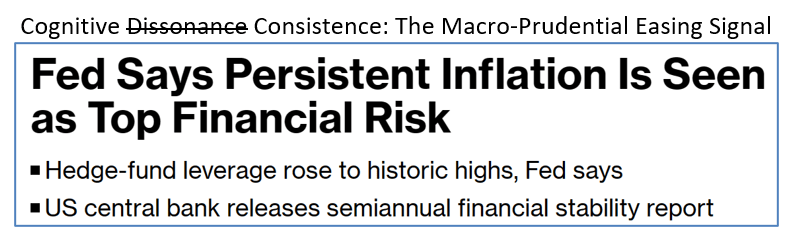

· The Fed’s latest Financial Stability Report is cognitively consistent with inflation-prompted financial instability.

· Inflation-prompted financial instability will prompt a Fed-initiated wave of macro-prudential easing in lieu of monetary policy easing.

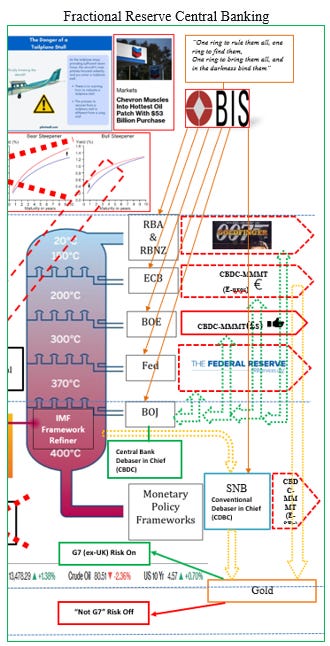

· “Fractionated” G7 central bank easing, in the order of the most Fragmentation-at-Risk to last, is being presented to mitigate Global Fragmentation.

· The ECB is taking great care, in managing the “Fractionation”, to prevent a weakening Euro from preventing it from easing.

· The ECB wishes to trade credible commitment for flexibility.

· The cost, to the Eurozone, of the ECB trading credible commitment for flexibility will be an inflation risk premium for the Euro and Euro-denominated assets.

· Fragmentation is being addressed with Fractional Reserve Central Banking.

· Fractional Reserve Central Banking will create new Global Reserves, by fiat.

· New Global Reserves will require each Fractional Reserve Central Bank involved to create new reserves in their respective commercial banking systems.

· New commercial banking system reserves will require new deficit-financing sovereign debt to balance their liability on each central bank balance sheet.

· New deficit-financing sovereign debt will be layered with insolvent lossmaking debt on central bank balance sheets.

· Since developed central banks are, in principle, committed to smaller balance sheets the scope for new banking system reserves is challenged.

· Developed central banks will evade the reserve creation challenge by subcontracting out reserve creation, credit creation, and fiscal deficit financing to the private “Masters of the Asset Class Universe”.

Extracts

· The PBOC technology-focused application of Modern Monetary Monopsony Theory (MMMT) overtly vitiates Janet Yellen’s balanced growth initiative.

· Japan Inc. will on-shore Taiwan Inc.’s technology global supply chain node by 2030.

· Global “Techno-Economic War” macroeconomic fundamentals mean that G7 central banks will need to follow the Fed’s “Patriotic Monetary Policymaking” example of Modern Monetary Monopsony Theory (MMMT) stimulus.

· G7 “Patriotic Monetary Policymaking” will necessitate the political and fiscal domination of the application of Brimmer’s Law by each central bank.

· The political and fiscal domination of the application of Brimmer’s Law, in each G7country, implies the political and fiscal capture of each central bank by its elected branch of policymaking.

· The German fiscal breach of “Black Zero” will only be an economic stimulus if the Bundesbank caps the rise in yields, with its balance sheet, to prevent the crowding out of private sector consumption-driven economic growth.

· Lethal casus belli is being framed as legal casus belli for Eurozone fiscal and political union.

(Source: the Author)

· The German fiscal breach of “Black Zero” will only be an economic stimulus if the Bundesbank caps the rise in yields, with its balance sheet, to prevent the crowding out of private sector consumption-driven economic growth.

(Source: the Author)

· The Reserve Bank of Australia’s Modern Monetary Monopsony Theory (MMMT) policy framework will be “ample”.

(Source: the Author)

· The insolvent Swiss National Bank (SNB) intends to return to solvency by a process of financial asset price inflation rather than real economic price inflation.

· The action of the Swiss National Bank (SNB)is a global risk-on signal for developed economies’, ex-Ungoverned Kingdom (UK), asset prices.

· The action of the Swiss National Bank (SNB) confirms the recent behaviour of “He/She/They Gold”.

· The SNB will also embrace the digital currency debasement zeitgeist of the times.

· Rumour has it that the ECB also intends to return to solvency by the same method as the SNB.

(Source: the Author)

· The Swiss National Bank (SNB) confirms that its unofficial mandate to return to solvency, through financial asset price inflation, takes priority over its price inflation mandate.

(Source: the Author)

· The Fed’s new Modern Monetary Monopsony Theory (MMMT) policy framework intends to ease Macro-Prudentially, rather than quantitatively or qualitatively.

· The Fed’s new Modern Monetary Monopsony Theory (MMMT) policy framework transfers wealth, from the Fed balance sheet to bank shareholders, for creating private credit with less regulatory capital risk.

· The Fed is failing to cure any banking sector addiction to MMMT with new capital adequacy and commercial risk pricing rules and regulations.

· The Fed’s new Modern Monetary Monopsony Theory (MMMT) policy framework is a morally hazardous surrender to, and capture by, the banking sector rather than the executive branch of policymaking.

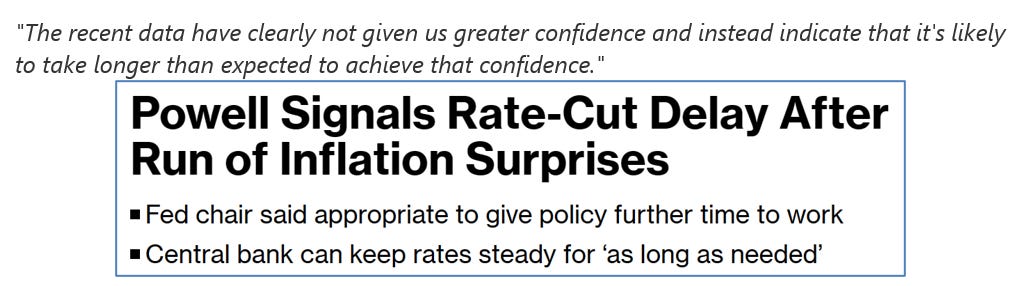

· The Key Signals analysis contradicts Chairman Powell’s rate optimism testimony.

(Source: the Author)

· There is no stigma attached to the adoption of Brimmer’s Law, through the Fed’s Standing Repo Facility, by the US commercial banks.

· The adoption of Brimmer’s Law, through the Fed’s Standing Repo Facility, vitiates against a repeat of the US regional banking crisis and mitigates for a soft landing.

· The endogenous, market-based, price discovery of Brimmer’s Law, via the Fed’s Standing Repo Facility, is more sustainable than the exogenous, indiscriminate, blunt trauma of crisis-response-driven Quantitative Easing (QE).

· The Fed’s “Standing Repopiate” is the gateway drug to Modern Monetary Monopsony Theory (MMMT).

· MMMT is a “Special Topic” in the Fed’s new monetary policy framework.

· The Fed’s new monetary policy framework must resolve conflicting signals from “tight” housing, and labor, markets; and the lack of appropriate policymaking rules of thumb.

· The Fed intends to cure any banking sector addiction to MMMT with new capital adequacy and commercial risk pricing rules and regulations.

· The Fed’s emerging monetary policy framework is an Esther George master class.

· The Fed has slowly learned, as Esther George taught, that supply curve convexity and oligopoly-driven price inelasticity are a “constraining”, Stagflationary economic headwind.

· The Fed’s disingenuous “Disinflation without a rise in Unemployment” new mantra takes false credit for the accidental “soft landing” predicted by Esther George’s “constraints”.

· The Fed’s latest Monetary Policy Report, and recent balance sheet commentary, herald a new definition of full employment; that is consistent with the existing dual mandate, assuming the latter remains the same.

(Source: the Author)

· The recently reported poor US bank earnings season signals that it is time for macro-prudential policy easing.

(Source: the Author)

· The “CIOgnoscenti” has, so far, missed the key signal that the Fed intends to lead a developed central bank wave of macroprudential policy easing, in lieu of inflation-challenged monetary policy easing.

(Source: the Author)

· The IMF concludes that the structural “Fragmentation” paradigm shift has shifted developed central bank monetary policy frameworks.

· The IMF implies that the absurd combination of “Quantitative Tightening” and “Qualitative Easing” is the optimal way to trade off inflation and financial stability risks at this point in the Polycrisis.

· “Fragmentation Spring” is shifting from the IMF Spring Meetings to Russia, via Ukraine.

(Source: the Author)

· The IMF believes that inflation is still too high to embrace MMMT.

(Source: the Author)

· The BIS proudly advocates for a strong US Dollar whilst coordinating G7 currency debasement in the pursuit of central bank solvency.

(Source: the Author)

· The BOJ upholds globally coordinated MMMT, which is predicated on a managed foreign exchange rate system that maintains the appearance of US Dollar strength.

(Source: the Author)

· Ex Post-Sintra, the Fed intends to interpret the IMF’s new monetary policy framework edict by sustaining Fiscal Dominance in pursuit of the Friend-Shoring imperative.

· Proposed higher Reserve Requirements must be balanced by a larger Fed balance sheet.

· Governor Barr confirms the Fed’s intention and capability to ‘drive the next leg of the “Great Rot-AI-tion” with tighter financial stability policy’.

· President Kashkari (finally) admits that Stagflation is a financial stability phenomenon.

· A larger Fed balance sheet will provide the taxpayer-backed assets to “layer” with the lossmaking “out-of-thin-air assets” currently causing the central bank’s insolvency.

· The Fed’s commitment, to a smaller balance sheet, means that Reserves and Assets will have to be managed, off balance sheet, by the “Masters of the Asset Class Universe”, going forward.

· US Monetary Policymaking, and Fiscal Policymaking, along with the elected executive policymaking function, will be ‘dominated’ by the non-elected “Masters of the Asset Class Universe”.

(Source: the Author)