The Fed’s Credible Commitment Point Will Be The Last One To Tip

"But them’s the breaks." (Alexander B. de Pfeffel Johnson)

Summary:

· A confluence of tipping points is pointing towards the next Hypergrowth phase inflection point.

· The next Hypergrowth phase inflection point is pending the Fed deciding that it has restored Hyper-credible commitment by fighting Hyperinflation with a Hyper-recession.

· The Hypergrowth phase inflection point is also pending the Manchin Tipping Point that is conditional on the FOMC’s next move.

· The Fed may decide to initiate the next Hypergrowth phase by “cancelling” the conflicting CIE data that it cannot fudge with a back testing best fit.

· The COVID-Zero Chinese Bank Run thesis is currently in Schopenhauer’s violent truth resistance phase.

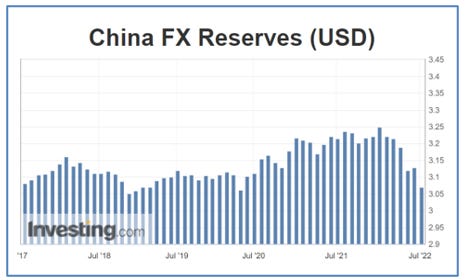

· The COVID-Zero Chinese FX Reserve Run thesis is well beyond Schopenhauer’s self-evident truth phase.

· Taiwan has been “asymmetrically” mobilized to preclude a repeat of the Ukraine surprise.

· There is political method in the latest perceived Kafkaesque COVID-Zero policy tweak.

· Political power now grows, innocuously, out of the barrel of a syringe.

· The collapsing Chinese property bubble is developing into a US Credit Crunch repeat.

· Commodity producers will be thrilled to know that China intends to spend $1.1 Trillion on infrastructure for a population that is locked down by “COVID-Zero” and has nowhere to go even if it were able to.

· The symbiotic process of “Dishevelling Up” should do-for both of the major UK political parties.

· The Bank of England thinks that it is highly likely that the UK economy will swiftly turn Japanese in 2023.

Credible Commitment Tipping Point: Are we there yet?

A “Just in Case” inflection point is now happening “Just in Time”.

(Source: the Author)

Tipping points are coinciding and positively reinforcing to become an inflection point.

· The MSP and the Biden G7 “Slam Dunk” “Friend Shoring” G7 Infrastructure Plan are Vinod Khosla’s “Techno-Economic War”.

(Source: the Author)

The tipping point referred to, by Speaker Pelosi’s neighbor Vinod Khosla, as a “Techno-Economic War” was recently noted coinciding with “Speaker Pelosi’s Bottom”.

· The Minerals Security Partnership (MSP) is “Friend Shoring” in action and is Macklem Doctrinaire in principle.

(Source: the Author)

These two coincidences coincided with the US sponsorship of the Minerals Security Partnership (MSP), which will sustain the supply of Rare Earth elements required for the next tipping point observation.

Most recently, the coincident tipping point of mass electric vehicle adoption in the US has just been recorded. A coincident AAA survey has found that roughly one-quarter of Americans now say that their next car will be electric, despite innate misgivings about the reliability of electric vehicles and the infrastructure available to support them. Readers should imagine the adoption rate if a massive fiscal stimulus was aimed at the misgivings about EVs. The MSP has, therefore, arrived just in time for US electric vehicle adoption.

Before getting carried away, however, the reader should also consider the formidable obstacle of Senator Joe Manchin. A Manchin Tipping Point, whatever this involves in terms of bribes and threats, needs to be achieved for the other aligned tipping points to cascade into each other at an inflection point.

Senator Manchin is currently stalled, waiting to see what the FOMC does about the latest inflation data. Should the Fed lean a little more heavily, on the economy, at the next FOMC meeting, Manchin may then be nudged into line with all the aligned tipping points.

To support the MSP and, presumably, to nudge Senator Manchin, President Biden is also pulling on the legislative lever of the old Cold War shibboleth of the Defence Production Act of 1950 to sustain technology supply chains, from mines all the way to consumers. According to US Energy Secretary Jennifer Granholm, this is a necessary piece of executive intervention because China has “weaponized” the elements involved in the technology sector. This Sino-Weaponization comes in addition to the Russo-Weaponization of its energy resources. Taken together, these two initiatives may be viewed as weapons of mass destruction to the economies of the Allies. In this “Techno-Economic War,” no quarter is being given on either side.

All the above coincidences coincide with the observation that the US “Friend Shoring” process of offshore productive and logistic capacity has kicked in.

Anticipation, of all these structural catalysts, is already working its way into Mr. Market’s investment thesis and style. Back in the day, such a confluence of coincidences used to traditionally lead to a Hypergrowth Phase in the sectors, and sub-sectors, involved once all the conditions precedent had aligned. Currently, they are aligning.

Mr. Market has been hunkered down in the trenches, with the Cash Cows, of late, but his gaze above the parapet is being attracted to Question Marks and potential Stars of the Hypergrowth “Techno-Economic War” phase ahead.

To take off, however, into Hypergrowth, central banks must do the needful with liquidity and credit refueling operations.

Speaker Pelosi “loves” Microsoft and Apple call options. Madam Speaker’s recent eyebrow-raising leveraged bottom fishing has raised more than a few eyebrows.

(Source: the Author)

Despite the investing discipline, however, there are always those well-informed insiders who jump the gun. They follow in the footsteps of the well-informed Speaker Pelosi.

· A Key Signals proprietary indicator signals that the FOMC is, once again, totally off with its timing, this time, on monetary policy tightening.

(Source and caption by Key Signals)

All involved, currently, follow in the footsteps of the Key Signals indicator which indicated that the Fed should be considering easing next, back in the first week of May this year.

· The Fed is fighting the last war whilst creating its next war.

(Source: the Author)

Currently, central banks are trying to Hypergrow their tiny credible commitment by being seen to prevent Hyperinflation. The Hypergrowth Phase is thus on pause, but within reach, awaiting central banks to dismount, from their high horses, and alight themselves on policy fuel for shiny new electric vehicles. The good news is that as the central banks stay in the saddle, for too long, they are creating the recessionary conditions on which “Hyper-Monetary Policy Easing” follows. The ensuing Hypergrowth Phase will, thus, be turbocharged.

It, thus, seems reasonable to conclude that the US economy has either reached the tipping point of Peak Oil or of Peak “Friend Shoring” hype. Arrival, at these potential tipping points, has been hastened by the Russian weaponization of its hydrocarbon resources, and the Chinese weaponization of its Rare Earth elements.

It is important to understand that oil prices can remain elevated even at Peak Oil for some time. It is the volume of oil consumed in the US that counts, not its price at the tipping point. The rate of consumption in volume terms of oil needs to fall for the Peak Oil point to be passed. This passing can be accelerated with higher prices. This passing may then lead to a sudden and dramatic fall in price. Volume leads price in this case. Indeed, it is necessary for oil prices to be elevated for some time in order to drive consumers away from it. Peak Oil in the US, is thus a slow death of the price rather than a spike.

One more (big rate hike) and done ….

In relation to the FOMC holding up the Hypergrowth Phase, the Biden Administration was keen to mitigate the fallout of the widely anticipated bad inflation number. Prior to the announcement, the White House framed the next shocker as an anachronism. Allegedly, inflation has peaked.

Atlanta Fed president Raphael Bostic was keen to make it clear that the Fed isn’t falling into a White House trap, again, as it did back in March 2021 with disastrous consequences for inflation. Despite saying that everything will be on the table, at the next FOMC meeting, in terms of rate hikes, however, Bostic was clear to say that he prefers the 75-Basis point rate hike tool.

Prompted, by the bad inflation numbers, Cleveland Fed president Loretta Mester also voiced her credible commitment to aggressively hiking interest rates. She would not specify just how credible, in terms of basis points, she is willing to go. Mester, allegedly, hasn’t seen any “solid proof” that inflation has rolled over. This author suggests that Mester should read the latest Beige Book more carefully.

· Esther George’s sound monetary policy compass will be sorely missed when she retires.

(Source: the Author)

Bostic and Mester’s alarmism was contrasted (and overshadowed) by Kansas City Fed president Esther George’s continuing valedictorian masterclass. George is retiring, and it’s a great pity.

When her colleagues were losing it, and the inflation mandate, over COVID, George was cautious. Now that they are losing it, and the full employment mandate, about inflation, she is also cautious. Her cautious consistency is what credible commitment, and hence being a central banker, is all about.

In her latest speech, George warned her overzealously Hawkish colleagues that they risked overplaying their extended forward guidance. Given the uncertainties, about just about everything, in the US and global economy, she believes that demonstrable, and incremental consistency to tighten monetary policy will (a) defeat inflation, (b) land the economy safely and (c) allow the Fed to shrink its balance sheet. This should be compared to hiking aggressively, and creating a recession, thereby, having to ease again, just as rapidly, and, thence, missing the chance to shrink the balance sheet at all. There is a lot to be said for caution.

In her latest speech, George warned her overzealously Hawkish colleagues that they risked overplaying their extended forward guidance. Given the uncertainties, about just about everything, in the US and global economy, she believes that demonstrable, and incremental consistency to tighten monetary policy will (a) defeat inflation, (b) land the economy safely and (c) allow the Fed to shrink its balance sheet. This should be compared to hiking aggressively, and creating a recession, thereby, having to ease again, just as rapidly, and, thence, missing the chance to shrink the balance sheet at all. There is a lot to be said for caution. Caution may obviate the need for drama and dramatic action.

George’s warning was supported, and amplified, by some empirical research from her staffers. The researchers found that the current tightening of monetary policy is more significant in force, and resultant impact, than the last attempt at balance sheet runoff in 2017. Readers all know what happened to that attempt. In this new instance, the outbreak of a global “Techno-Economic War” has replaced the outbreak of COVID-19 as the threat that will require mitigation with monetary policy easing at some juncture.

Without saying it, George indicated that the Fed’s current course of action will lead to a financial crisis and recession that will, then, oblige the central bank to rapidly cut interest rates and expand its balance sheet even further. She noted that this outcome is already being discounted, in the forward curve, despite the relatively recent start of serious monetary policy tightening. This author hopes that George continues to comment on monetary policy when she retires.

Richmond Fed president Thomas Barkin seems to be closer in spirit to George than he is to Bostic. Barkin would like to keep his options, and hence signaling flexibility, open on the size of the next rate hike. Were he to vote for 50-basis points, rather than 75, this could be interpreted as a signal that he believes that the worst is over for inflation.

Fed Governor Christopher Waller is also keen not to let the latest inflation data overly influence the next FOMC meeting. Waller is still aiming for a soft landing by the sound of it. He is, thus, still in the 75-Basis points rate hike camp, and believes that the underlying labor market strength will preclude a hard landing.

Like Waller, St Louis Fed president James Bullard is not advancing to the 100-Basis points baseline based on the latest inflation data. For choice, he prefers to go 75-Basis points at the next FOMC meeting.

The reluctance of Fed speakers, to go the full 100-Basis points, in their recent guidance, suggests a tipping point in the balance of risks ahead. There are some constituencies, within the Fed as an institution, that are tipping towards the growth risk. This tipping creates an impression of divergence.

It’s not Black and White, it’s not even Grey, it’s Beige ….

The eagerly anticipated CPI data fed further anticipation that the Fed will have to go large again, by at least 75-Basis points. Even 100-Basis points are now anticipated by some. In response to the data, Atlanta Fed president Raphael Bostic confirmed that “everything”, in terms of tightening options, is now on the table. It is also anticipated, by some, that the next oversize rate hike, will be the last of its ilk if not to say the last rate hike in this cycle.

· The Regional Fed’s view of the US economy is, currently, more accurate than the FOMC’s.

(Source: the Author)

Based purely on the criterion, of the veracity, of the Beige Book, so far, this year, the Regional Fed has more credibility than the Federal Reserve Board. Given the frequency of the Beige Book, it is not a bad barometer of accuracy. Sadly, Regional Fed presidents get seduced, by the political consensus approach to monetary policymaking, and lose their own credibility, when they rotate into the FOMC voting chair. Cleveland Fed president Loretta Mester is a seduction case in point.

Hence, if the contents of the latest Beige Book are to be taken at face value, and therefore of a higher value than recent FOMC extended forward guidance, the US economy is “moderating” and inflation is abating. One more big rate hike, and done, would, thus, seem to be the appropriate level of discretion for the better part of the FOMC’s valor.

If only things were that simple in real life.

There are lies, damned lies, and the CIE. (sic)

“The index of common inflation expectations at the board has moved up after being pretty flat for a long time, so we’re watching that, and we’re thinking, ‘This is something we need to take seriously’”

(Jerome Powell: June 15th, 2022)

At the last FOMC meeting, Chairman Powell alluded to the source of divergence between the Fed Board, in Washington, and the Regional Fed branches. The FOMC, it should be remembered, also seduces Regional Fed presidents once they rotate into the Washington voting chair.

Powell’s allusion is in relation to, a work in progress on, the illusion called the Index of Common Inflation Expectations (CIE).

The CIE work in progress is an attempt, by the Federal Reserve Board, to accurately measure inflation expectations. Presumably, if you can measure inflation expectations, accurately, you can manage them.

A brief history, of the CIE, shows that inflation expectations have not yet been accurately measured. Thus, by default, inflation expectations have not been managed yet. Therefore, by default, the Fed has not been performing its inflation mandate properly. The Fed may argue that it does not have an inflation expectations mandate. Managing this derivative inflation indicator, however, is clearly critical in performing the Fed’s inflation mandate.

The current iteration of the formulae, to construct the CIE, shows that inflation expectations have been, worryingly, on the rise since COVID hit in 2020. Viewed through the narrow context, of the CIE, the Fed should be continuing to hike interest rates, aggressively, if it is serious about suppressing rising inflation expectations.

Evidently, the Fed is now being second-guessed, on its employment mandate, whilst it is still failing on its inflation mandate.

This author notes two things.

Firstly, each iteration of the CIE appears to have the impact of making inflation expectations look lower than under previous calculations. In fact, the latest CIE measure (2.19%), although elevated, above 2%, isn’t really elevated by much over time. This author wonders how objective the methodology really is, especially when the inputs keep getting changed with hindsight. He also wonders if there is not some innate bias to want to make inflation expectations appear lower, and hence, closer to target, thereby, making the Fed look like a better inflation fighter than it really is.

Secondly, this author notes that the CIE comes with a big legal disclaimer that the Fed is not responsible for any harm done to the US economy by following it. There is also the added disclaimer to drop the CIE at any point in time that the Fed so chooses.

From this author’s perspective, the legal disclaimers are pure “Judge Powell”. The author has noted that the Chairman has assiduously, and legally, prepared for a face-off, with Congress, over the central bank’s historic failure to consistently hit either of its mandate KPIs.

From this author’s perspective, also, it is clear that the Fed could just let the CIE suddenly disappear; if it conflicted with the overriding Washington economic agenda of the day.

The author suspects that the CIE is being continuously re-iterated to show that the Fed has succeeded in flexible average inflation target (FAIT) overshooting. He also suspects that the latest supply-side inflation spike has undone these devious intentions by continuing to rise at each iteration point. It now looks as though only a painful recession will do in nudging inflation expectations in the right direction. But, in Stagflationary times, such as these, short-term inflation expectations can continue to rise even as long-term expectations fall. The CIE is, thus, losing its utility in supporting the Fed’s relatively recent new monetary policy framework. The CIE’s days may, therefore, be numbered unless it can be made to conform with the Fed’s credible commitment imperative.

To all intents and purposes, therefore, there is a limit to how high recorded inflation expectations can rise. They can only rise to the level at which the Fed bins the CIE. Chairman Powell, evidently, reserves the right to use the unconventional monetary policy tool of “Cancel Culture” in line with measures adopted by the elected branch of policymaking. If CIE doesn’t say the right thing, it will be canceled.

Better times on the global front than on the home front ….

The news for the White House is somewhat better on the global front than the domestic front. There are, apparently, tangible signs that it now has the initiative over Russia and China.

The South China Morning Post (SCMP), a useful journalistic barometer of the Cold War between the US and China, estimates that, at this stage of the conflict, the US has gained the initiative. The potential US Hypergrowth Phase, discussed previously, therefore, has a powerful fundamental global macro driver to sustain it also.

· The Ukraine war is a wargame for the Taiwan war.

(Source: the Author)

Low-ranking US State Department official Jessica Lewis has nudged the initiative, from the tactical position, on the ground, to the strategic international level in recent comments linking the situation in Ukraine to the one in Taiwan.

Chinese FM Wang Yi is now on the record as saying that ‘China and Russia have maintained normal exchanges and promoted cooperation in various fields and cast aside any "interference", showing the "strong resilience" and "strategic resolve" of their relations.’

G7 can now, with justification, claim that China is a combatant in the Ukraine war, and then go on to ratchet up political and economic sanctions proportionately.

(Source: the Author)

Readers will remember that, back in the previous report, China had formally accepted its strategic partnership with Russia. Capitalizing on this admission, Assistant Secretary Lewis recently opined that the, allegedly, successful “asymmetric” war in Ukraine serves as a model for the successful prosecution of an “asymmetric” war in Taiwan. The Taiwanese population, in general, has, thus, been quasi-mobilized to prepare “asymmetric” tactics and weapons to defeat an imminent Chinese invasion. Maybe China will reconsider its plans for an invasion after this signal of “asymmetric” mobilization in Taiwan.

· The slipped G7 “Biden Slam Dunk” will become the “Blinken Slam Dunk” at G20.

(Source: the Author)

The SCMP barometer, if accurate, suggested that the ensuing G20 summit would be, a real humdinger, as anticipated. Russia and China would be trying to narrow the perceived initiative gap and get ahead. An uncharacteristically feisty Treasury Secretary Janet Yellen gave the event some advance top-billing, with her opening salvo, that Russia did not even deserve to be there.

Yellen’s aggressive opener, thereby, framed the G20 summit, as a non-event, in terms of achieving a meaningful global consensus on anything. There were some consensual policymaking minutiae, about addressing short-term food insecurity but, in general, the summit outlined global divisions rather than closed them.

If America has gained the initiative, then, the global division with China, sees the latter falling behind the former.

The COVID-Zero Bank Run ….

· China’s “COVID-Zero” strategy may now be to mitigate bank runs rather than COVID-19 per se.

(Source: the Author)

This author once theorized that China’s “COVID-Zero” policy, amongst other strategic objectives, was a macro-stability policy tool aimed at stemming runs on Chinese banks.

The recent chaos suggests that Chinese depositors have tumbled this ruse and are rapidly trying to make withdrawals before their banks become insolvent. Various excuses, along with baton charges, have been given to irate depositors in lieu of their cash. The depositors’ revolt has now reached the doors of the PBOC.

The best excuse so far, given to angry depositors, has to be one that banking systems are being upgraded, in rural banks, which somehow precludes depositors from making withdrawals. This kind of thesis ridicule has, unfortunately, transitioned to violent thesis resistance, on-route to self-evident thesis acceptance.

If it looks like a bank run and quacks like a bank run, it, most likely, is a bank run. If it is a bank run, it means that the banking system is becoming insolvent and that the PBOC has not, so far, been instructed to bail the system out.

This also means that China’s financial resources are finite and are being conserved, perhaps, by global threats and/or for opportunities. This author suggests that, based on the dwindling level of China’s FX reserves, the said finite resources are being conserved by global threats rather than for global opportunities. The rundown of China’s FX reserves, clearly, explains the attempts to forestall a run on the banks. China’s FX reserves are now lower than they were at the time of the first COVID-19 outbreak.

Russian energy exporters may now have to accept Yuan, which they can only then spend in China if they are looking for alternative buyers to European ones. This would not unduly worry the Chinese. It may worry the Russians, however, and call them to question the financial terms and conditions of their partnership with China.

· “COVID-Zero” is entering a multi-year rolling lockdown phase that will obstruct Chinese investment and trade flows.

(Source: the Author)

Further context has been provided by recent edicts, from Chinese state regulators, which effectively choke off outward-bound capital and investment flows. The application of the “COVID-Zero” policy is, hence, behind the curve since the capital flow horse has bolted. The stable door is being shut to prevent the whole stampede from leaving.

The prospect of the first Chinese domestic bond default will provide further context to how the country’s finite economic resources will be applied to the growing list of threats.

· “Imperator Xi’s” triumphal celebrations confirm that “COVID-Zero” is a strategic policy tool, which suggests that COVID-19 is a strategic weapon.

· Hong Kong may become a “Trojan Horse” in the global economy.

· “COVID-Zero” is the new “Long March”.

· Political power now grows out of the barrel of a syringe.

(Source: the Author)

Economic resources will be conserved in the newly annexed territory, of Hong Kong, as the city moves to adopt the “COVID-Zero” protocols being administered on the mainland. Anticipated protests, on the streets, and bank runs, have, thus, been effectively interdicted.

The architect of “COVID-Zero”, either, wishes to lead by example or he is afraid of the mob on the streets. Whatever the reason, since his recent triumph in Hong Kong, President Xi Jinping has disappeared from public view. The only evidence of his existence are edicts, attributed to him, on the Communist Party website. This author notes that, should an invasion of Taiwan be underway, the Chinese President would, logically, wish to be out of harm’s way in the build-up.

“COVID-Zero” is proving to be a crude but effective policy tool with unwelcome outcomes.

The “COVID-Zero” Property Bust ….

Chinese policymakers, evidently, do not wish to use the property construction sector as a stimulus tool anymore. This hints that there is too much spare capacity of houses and commercial real estate. Consequently, “COVID-Zero” has been applied on both the supply and demand side of the construction sector.

Locked-down consumers cannot buy houses/apartments and locked-down builders cannot build them. This strategy is not without its economic costs, as developers are now in free fall. No doubt this free fall will consolidate around a handful of selected national champions, who can be used as a stimulus tool more effectively. Thus far, policymakers are letting construction companies default, thereby, effectively, making the cost of a national consolidation initiative cheaper in acquisition price terms. The cost in political capital terms may eventually be larger, however. China’s finite economic resources are stretched, indeed, and need careful preservation at the cost of private capital.

The finite economic reserves appear to be earmarked for infrastructure spending. Evidently, as in Nazi Germany, Chinese policymakers currently judge that the best projection of strength and “Common Prosperity” is an extensive motorway and railway system.

Chinese homebuyers are not taking the enforced status quo lying down, thereby, creating one of those unintended consequence risks for the government. The problem started with homebuyers in 22 cities who are refusing to pay their mortgages on properties that have been delayed. A recent count puts the number of cities where mortgage payment rebellion is occurring at 50. The banks estimate the current hit to be about $312 million. This is, however, purely on the mortgage losses, and does not take into account the delinquent loans to the developers. And then, there is the underlying collateral value of the homes that underly the mortgages. Chinese property prices have been falling for the last 10 months. Whilst the banks may have made provisions for non-mortgage payments, they will also have to provision for falling mortgage asset and developer loan values.

Bank assets, in the form of mortgages, and developer loans, have, thus, become distressed, thereby, impeding the ability of banks to pay their liabilities to depositors. The banks are, therefore, being hit twice. They are then being hit, a third and fourth time, by the falling asset value of their mortgage portfolios and developer loan portfolios. Banks are, hence, wary and incapable of making new loans. The credit creation process has been choked off, thereby, presenting another economic headwind to the economy in general. If all this sounds like the USA circa 2008/09, it should.

The Chinese National Bureau of Statistics estimates that the property sector has experienced a 7% contraction, making it the greatest drag on the economy in general. The property sector is, apparently, so bad that it is now being canceled through state censorship of all data and news pertaining to it.

If you build it, will they really come?

What is the point in building roads if there are no houses, or no banks, at the ends of these roads? The same goes for railways.

Chinese policymakers may, in fact, be more worried about the overt, political nature of the resistance from mortgage payers than any hit to the banking system; but they should not underestimate the strong correlation between the two threats.

This unedifying spectacle, of wealth confiscation, in the name of “Common Prosperity”, only serves to illustrate that China is un-investable for foreigners. Symbolic of this un-investability are Morningstar China’s operation’s recent cuts, and restructuring, to focus exclusively on a domestic client base.

The Kafkaesque “COVID-Zero” Tweak ….

With rebellion fomenting, on the streets, and at the bank, and with the sequestered President apparently preparing for the invasion of Taiwan, the political need to incarcerate the population was strengthened. This mass incarceration is being executed with a tweak to the “COVID-Zero” compliance rules and regulations. Now, full vaccination is no longer required to go out in public. But since the virus threat level has been also raised, those who are not vaccinated (i.e. the vast majority) cannot go out in public in any case.

· Hong Kong may become a “Trojan Horse” in the global economy.

(Source: the Author)

In Hong Kong, the recently conquered natives will now be enslaved by Imperator “COVID-Zero” and will be forced to wear his shackles which conveniently double up as fashionable smart COVID trackers. Should these slaves be allowed to travel, externally, their hosts will be surveilled with all the spyware loaded onto these gadgets. Vae victis.

· Political power now grows out of the barrel of a syringe.

(Source: the Author)

There is some political method in the seeming Kafkaesque madness. Political power now grows, innocuously, out of the barrel of a syringe.

Ride a White Swan, if you’re a commodity exporter ….

With “COVID-Zero” in place, there is no pressure on the Chinese President to deliver double-digit economic growth. On the contrary, the pressure is now on to conserve resources, and not waste them on exports to competitors and enemies. If said competitors, and enemies, can be weakened with this economic weapon, then, so much the better.

In any case, said competitors, and enemies, are “Friend Shoring”, so, the days of double-digit Chinese growth are over. Probably a good time, therefore, to have tight societal controls and governance in place for an economy that is not delivering, export-driven, “Common Prosperity” as it used to. Premier Li Keqiang had the unenviable task of taking the responsibility, and thereby political liability, for the economy in his recent synopsis of how it looks. It looks weak. Still, that’s not President Xi’s problem it’s Premier Li’s. Any potential future challenge, by the latter, on the former has, thus, been weakened up front.

(Source: the Author)

Despite the webbed feet frantically stirring up the mud, at the bottom of the pool, the serene White Swanlike figure of President Xi Jinping still floats along merrily. The itchy Black Swan costume is being worn by the Chinese Premier. “Them’s the breaks,” as the great UK Statesman said.

The burden of dealing with the devil, in the details, and the economic and political blowback, has been ceremoniously/ceremonially unloaded on Premier Li Keqiang. And who would blame the President for delegating this pile of the proverbial?

The beleaguered Premier has recently announced that he is attentive to the economic misfortunes of the economy and will deal with them. The said misfortune at the hands of the “COVID-Zero” policy is estimated, by Chinese statisticians, to have cost the Chinese economy 14% of its potential GDP over the last couple of months. Apparently, Premier Li is going to boost 14% of GDP by building infrastructure for people whom the President is locking down. Confucius would have explained this somehow. This author is mystified.

The next Great Wall of Chinese infrastructure may, also, be visible from space; but its users may not be, because they are not there. They are and will be, locked down.

Premier Li and his Amazing Dancing Bear ….

The reader should note that the Chinese Premier will have to be creative, and, or, draconian because the country’s finite economic resources are constrained. The Premier’s hands are tied and he will also get the blame for whatever goes wrong.

Premier Li appears to be a game-old bird, who is not taking any of his economically-constrained fate lying down. Apparently, he fully intends to spend $1.1 Trillion, on infrastructure, for a population that is locked down by “COVID-Zero”, and has nowhere to go, even if it were able to. Commodity producers would seem to be the greatest beneficiary of this Kafkaesque economic policy initiative.

Readers, who enjoy a good bit of Kafka and chips, will be thrilled to bits by what is playing in the UK.

The UK has become the occidental spiritual home of Kafka.

Dishevelling Up: A Plague on your Houses ….

The Labour Party is gleefully rubbing its hands, for the cameras, and calling for a no-confidence vote on the UK Government. The Labour Party should be careful, about what it wishes for, because its own key personnel have been compromised, by the Conservative government, and must, therefore, go the same way with a no-confidence vote.

The Labour Party are the witting victims of a clever schoolboy Conservative Brexit prank. Brexit was energized by the immigration question. It was a question that the Labour Party did not answer because it could not answer. It could not answer because it was compromised.

The Conservative Party unloaded immigrants, and asylum seekers, on the regions, with brio, primarily in the North and in Wales. This unloading was explained, by the UK Treasury, as being cost-effective, for the taxpayer, because accommodation is cheaper in the regions, especially in the North. Hence, the cost to the taxpayer of housing immigrants, and asylum seekers, in the regions, and especially the North, was reduced by shipping them off in those directions. This logistic process created jobs for the boys, and girls, in the public and private sectors associated with this immigration policy.

Fat contracts were awarded to Serco and Mears, amongst others, for the logistic outsourcing of UK immigration policy to the private sector. Local authorities, and associated slum landlords, prospered. Labour local councils in the regions, selected for targeting, received much-needed cash injections as part of this outsourcing process.

None of the regional cash infusion went into building more housing stock, or sufficient local public and health infrastructure to cope with the growing populations in the areas involved. In fact, housing stock was taken off the market, from the local population, and put into the hands of private landlords riding the immigration outsourcing gravy train. Consequently, the regional native inhabitants developed animosity toward all things asylum/immigrant.

Clever politicians, like Boris Johnson and Dominic Cummings, understood the political game. As the regions buckled under, the waves of immigrants, Boris talked up Brexit and his Home Secretary delivered repatriation. Whilst talking up the solutions, care was taken to exacerbate the problem through the accelerated outsourcing to the regions and North. Thus, contrary to widely held public disbelief, Boris Johnson’s Red Wall surprise election victory was a logical outcome of shrewd policy execution and a shrewd media campaign.

The pledge to “Level Up” was empty, as the continuing “Dishevelling Up” with complicit support from venal Labour local councilors continued at a clip. “Dishevelling Up” was, and still is, a systematic process that undermines “Levelling Up”. Both parties are complicit.

The Conservative Party now wants to “Level Up”, and save money, by shipping folks off to Rwanda. Evidently, the Conservative Party understands that its grand scheme has been sussed out so that now it actually has to deliver on “Levelling Up” rather than use it for spuriously building political capital.

And so, when Labour pledges to “Level Up”, one may ask how.

Then it will be game on for the Britain Project, with its 1990s Tony Blair DNA. This game is already happening in the high street shops that are selling out of 1990s fashion.

(Source: the Author)

Both UK parties need to go. And there is some indication that they will, in due course.

· The UK will become an austere economy with an ungovernable polity.

(Source: the Author)

This author suspects that the policymakers’ solution to the underinvestment will not be higher interest rates, however.

· Larry Summers’ eulogy for Shinzo Abe is a panegyric for the return of MMT.

(Source: the Author)

As with the riddle of Larry Summers’ eulogy for Shinzo Abe, delivered inside the mystery of Modern Monetary Theory (MMT), Bank of England Governor Andrew Bailey is forecasting that the UK economy will turn Japanese in 2023. The project to build a new middle-of-the-road political consensus must, therefore, by default, be wrapped in the enigma of Abenomics.

If and when they all go, the Resignators will leave behind an economy that the Bank of England recently described as the least well-equipped developed economy to deal with economic growth and inflation threats.

(Source: the Author)

The Bank has previously stated that the UK economy is the developed economy least capable of standing the inflation and growth risks of current times.

The Resolution Foundation, and the London School of Economics (LSE), recently quantified just how relatively incapable the UK economy is.

Ironically, right off the bat, in the summary, the “Dishevelling Up” strategy, deployed by Boris Johnson is exposed but not elaborated upon. “Dishevelling Up” is taken as ceteris paribus, by the authors of the study. This implicit acceptance is an acceptance of the egregious abuse of governance at the rotten core of UK politics.

The study is, therefore, of little empirical value based on its avoidance of the obvious. The author suspects that the report is intended, as a prop, to bolster the case for Re-joining (formerly knowns as Remaining in) the EU; since the authors highlight how inequality is less on the continent than in the UK.

Presumably, therefore, according to the study’s logic, if/when the UK re-joins the EU the regional inequality will vanish. “Levelling Up”, thereby, conflates with “Re-Join”. Perhaps this conflation is not a bad guess, based on the fact that the Conservatives exploited the inequality to strengthen the Brexit vote. It remains a guesstimate, however.

Thus, politically flawed, with the overt sotto voce Remain undertones, and halo, the study does shed some light on how policymakers, and the Bank of England, will attempt to dig the UK economy out of the hole.

The study calculates that UK consumers are £ 9,000 less capable of living through current conditions. What this implies is that someone will have to come up with the cash. The Conservatives promise to cut taxes, in the view that the ensuing economic growth will generate the £9K/capita desired outcome. This is political dogma wrapped inside nostalgic Thatcherite wishful thinking.

What has happened, in Japan, is that the central bank has appeared to come up with the loot by expanding its balance sheet. The Bank of England, therefore, must expand its balance sheet at least by the £9K/capita gap between British consumers and their developed economic peers. This will be the case, whether the UK re-joins the EU or not.

Sterling is still in danger, although phony prosperity, from MMT, also lurks around the corner in 2023. In the absence of trade deals, with developed economies of scale, a weak Pound will create stronger inflation than stronger export-led GDP.

· Britain conflates the Commonwealth regime with the concurrent G7 global governance best practice regime.

(Source: the Author)

The global solution is for the UK to stop isolating and undermining the two trade blocs of NAFTA and the EU. This is the reason why it all went so bad for Boris Johnson at G7. His arrogance would have been tolerated, within the bloc, but outside the EU, trying to re-invent the British Empire, he was never going to survive. “Dishevelling Up” at home is forgivable, but dishevelling the global trading system is only something that a superpower can do.