Intransient Inflation, Intransient Fiscal Stimulus, Intransient Monetary Policy Stimulus

“Once is happenstance. Twice is coincidence. Three times is enemy action.” (Auric Goldfinger)

Summary:

· The inflation data contradicts Chairman Powell’s recent testimony.

· Mr. Mea Culpa Market contradicts Chairman Powell’s recent testimony.

· The recent ETF marked-to-market solvent BOJ flips its Modern Monetary Monopsony Theory (MMMT) policy framework mix, from Quantitative/Qualitative Easing to Quantitative Easing only; in order to mark its bond portfolio in the black.

· The BOJ has become an “Indirect Inactivist Investor” in Japan Inc.

· Like the Fed, the ECB will apply Brimmer’s Law in its new Modern Monetary Monopsony Theory (MMMT) policy framework.

· The application of Brimmer’s Law, by the ECB, lowers the financial stability risk in the Eurozone.

· Lower Eurozone financial stability risk reduces the requirement for aggressive interest rate cuts by the ECB.

Extracts

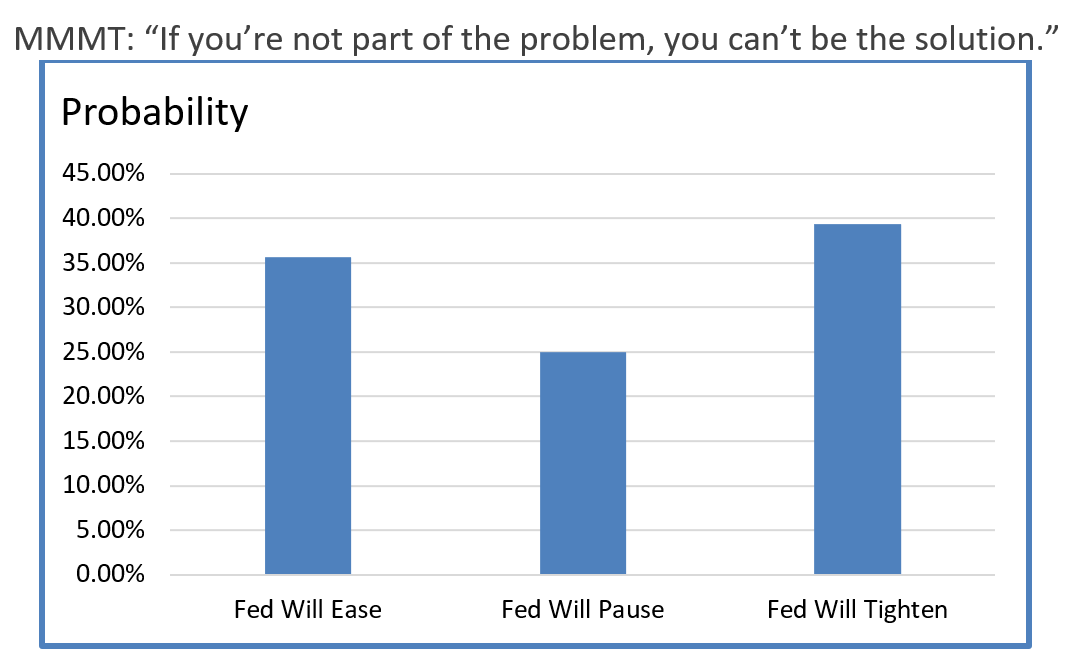

· The Key Signals analysis contradicts Chairman Powell’s rate optimism testimony.

· The Fed may be “not far” from easing, but it is closer to tightening before it eases.

· At this point, the Fed is unlikely to ease, before a new Presidential Cycle has begun unless it is rooting for the incumbent.

· At this point, the Fed is more likely to tighten, into a new Presidential Cycle, before being quickly forced into easing by the hard landing that it has created.

(Source: the Author)

· The recently (marked-to-market) solvent BOJ demonstrates the precedent for the panacea of Modern Monetary Monopsony Theory (MMMT).

(Source: the Author)

· Governor Kuroda confirms the Key Signals translation of Higher/Tighter for Longer as MMMT Forever.

(Source: the Author)

· The ECB’s intended expanded balance sheet mix, of Quantitative Easing (Sovereign Bonds), and Qualitative Easing (Bank Loans), is Modern Monetary Monopsony Theory (MMMT) by fiat.

· The ECB’s intended Modern Monetary Monopsony Theory (MMMT) implementation is pending inflation returning to target.

· Eurozone inflation’s return to target may require the financial instability that MMMT is designed to respond to.

· The ECB has an implicit financial stability policy mandate conditional upon compliance with its inflation target mandate.

(Source: the Author)

· There is no stigma attached to the adoption of Brimmer’s Law, through the Fed’s Standing Repo Facility, by the US commercial banks.

· The adoption of Brimmer’s Law, through the Fed’s Standing Repo Facility, vitiates against a repeat of the US regional banking crisis and mitigates for a soft landing.

· The endogenous, market-based, price discovery of Brimmer’s Law, via the Fed’s Standing Repo Facility, is more sustainable than the exogenous, indiscriminate, blunt trauma of crisis-response-driven Quantitative Easing (QE).

· The Fed’s “Standing Repopiate” is the gateway drug to Modern Monetary Monopsony Theory (MMMT).

(Source: the Author)